The 2019 Winter EECFA Construction Forecast Report has been released. It can be purchased, and a sample report can be viewed at www.eecfa.com. EECFA (Eastern European Construction Forecasting Association) conducts research on the construction markets of 8 Eastern-European countries.

Southeast Europe

Building construction market of the Balkan countries of EECFA is in prosperity phase. In the 2016-2019 period the market size expanded by 30%. We think that the current cycle is getting closer to the peak and for the upcoming 2 years we foresee a deceleration. One extreme is Serbia’s building construction market. It well outperformed the rest of the countries in the past 4 years and hardly sees any further expansion. As we are getting closer to the end of the current EU programming period, the civil engineering submarket is projected to contribute more positively to total construction market growth.

Bulgaria. Construction output in Bulgaria continues its recovery as both building and civil constructions are contributing. Residential construction is boosted by increasing real wages and low interest rates on housing loans which make buying a home more and more affordable. Persistent demand for contemporary office premises, along with the ongoing expansion of industrial and warehousing projects, will likely continue to be a tailwind for non-residential construction in 2019-2021. Civil engineering construction is forecasted to continue its upward trend in line with EU fund absorption. Growth here in the upcoming years will be fuelled by large transport infrastructure projects and the public utility sector. Total construction output is set to grow by 8.7% in 2019, and to add another 6.5% in both 2020 and 2021.

Croatia. Construction in Croatia is in transition. Some sectors are reaching the limits of catch-up growth. Others are only now beginning to benefit from it. While the direction and inevitability of this transition is clear, the timing is less so, with each sector likely to follow its own, unique path. This said, certain factors, among them emigration, the slowness of key reforms (especially regarding the judiciary), rising construction costs, the government’s ability to secure EU and other official funds and increased international competition for the tourists on which, for better or worse, Croatia’s economy relies, will affect all construction sectors. The outlook is by no means grim. Croatia is not nearly done with its transition, certainly not as far as construction is concerned. Many opportunities remain.

Romania. Romania’s construction subsectors have seen different trends. Residential and non-residential have been on a growth path for several years, while civil engineering has been declining since 2015. Residential construction should remain the main contributor to growth in the forecast period on the back of increased income and high demand for new construction, though regulatory and tax changes have slowed down the subsector. Romania’s economic growth, one of the strongest in the EU, and increased public consumption are feeding the need for new non-residential construction; however, increased skilled labour shortages and costs keep the segment in check, hindering development. For civil engineering, increased construction costs, elections and government changes counter much of the potential growth. Overall, construction across Romania is predicted to expand by 6.4% in 2019 but switch to a lower gear in both 2020 and 2021.

Written by Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members

Croatia will at the turn of the year assume the rotating presidency of the Council of the European Union. So now is an appropriate time to assess how the Croatian government’s policies affect the country’s construction sector.

Source: Depositphotos

The

government’s preparations for the presidency don’t inspire confidence that its influence

is a positive one: the remodeling of the main building for the presidency won’t

be completed until December 22, leaving no room for (further) delays. And there

are concerns that the “finished” building won’t in fact provide satisfactory

facilities. Not to mention the project’s being at least 50% over budget.

On the

other hand, the current government has substantially increased Croatia’s

absorption rate for EU funds. At 78% it is now slightly higher than the EU

average of 77% and significantly greater than the country’s below-EU-average

2018 rate of 52%. This improved performance has enabled Croatia to invest

massive amounts in infrastructure. And while, bureaucratic delays have meant

that end users have received only 25% of the amounts they contracted for, much

less than the 33% EU average, there is a real likelihood of even more rapid EU

funds absorption in Croatia.

First,

use-it-or-lose-it rules governing these moneys mean that contracts relying on

them must be entered into before year-end 2020. Second, and crucially,

presidential and parliamentary elections are coming up next year, by January 20

in the case of the president and by December 23 in the case of the parliament.

Parliamentary elections, though, could be triggered far earlier if any of the minority

members of the current, fragile coalition withdraws its support.

On

24 June 2019, the 2019 Summer EECFA Construction Forecast Report up to 2021 was

published. Full reports can be purchased, and a sample report can be viewed at www.eecfa.com. EECFA (Eastern European

Construction Forecasting Association) conducts research on the construction

markets of 8 Eastern-European countries.

Southeast Europe

Good years are predicted to continue in the construction markets of Eastern and Western Balkan countries of EECFA. Altogether around 15% cumulated real growth is foreseen for the region as a whole in 2019-2021. The annual pace of growth, however, is gradually decelerating on the forecast horizon. In this upcoming period civil engineering is expected to outperform building construction in all countries, except for Romania.

click to enlarge

Bulgaria’s construction output remains on a growth path since both building construction and civil engineering continue to expand. Residential construction is still an attractive investment due to increasing profitability on the back of a positive change in disposable income and low interest rates. Growth in non-residential construction is backed by the acceleration in office segment and a stable performance in manufacturing and warehousing. Civil engineering is to be driven by road and public utility segments, while major projects in railway construction are struggling to start. Construction output is projected to grow by 5% in 2019 and 4% in 2020. The end of the EU programming period of 2014-2020 will likely give and additional boost of 7% in 2021.

Construction in Croatia is at a crossroads. Some sectors that have shown strong catch-up growth will soon slow. Others, so far less favored, will soon benefit from such growth. The country is also at a crossroads in another sense. An aging population, continued emigration, rising construction costs and increased international competition for tourists will threaten a number of construction sectors unless wise political choices are made. All in all, though, while the forecast for the Croatian construction industry as a whole is not as sunny as it once was and while patches of cloud have begun to appear in some places, other areas are expected to enjoy significantly more favorable conditions than in the past.

Romania’s construction is set to grow by 6% in 2019. Residential construction, after a remarkable growth between 2016 and 2018, might be hindered by legal and policy changes. Despite some concerns over the contrary, residential activity is still predicted to remain one of the main drivers of the Romanian construction market, at least until 2020. Demand remains high for most types of non-residential construction as well. But talent shortages and higher operating costs would, likewise, limit the growth of the segment. Of notable interest is the expected growth in civil engineering segments which considerably dropped after 2015 but are to return to a positive trend with renewed interest due to availability of national and EU funding and increased public interest in the election years.

In Serbia the booming cycle is now encompassing practically all construction segments, with strong performance in both buildings and civil engineering. While residential and non-residential buildings were leading the growth in the previous period, civil engineering is expected to again take charge in 2019. With increased spending in road construction and major large-scale projects now underway in energy and railroad, there is a strong expansion of outputs in this forecast horizon. Although extensive growth in previous years already doubled outputs in many segments, particularly in buildings, there is yet more to come. Total construction output in 2021 will likely at least double the volumes from 2015.

Construction industry in Slovenia continues to grow fast, recording a second consecutive year of double-digit growth. Based on strong economic growth, easy access to credit and strong demand for residential housing, its foundation would remain strong also in 2020 unless a major external shock reversed the current optimism on the market. Even in such case, there are several large civil engineering projects, especially the construction of a new railway towards Port Koper that began in early 2019, that will induce growth in construction output for several years.

East

Europe

The East-European countries EECFA covers show a completely different picture from that of the Balkan. The cumulated growth expectation of the region is -1% for 2019-2021. Turkey’s construction market is in such trouble as previously predicted, and this drags down the whole region’s performance. On country level, only Turkey sees negative cumulated growth until 2021, while Russia is prognosticated to be moderately positive. And Ukraine can reach the highest growth rates. In each country civil engineering is forecast to perform better (less worse in case of Turkey) than building construction until 2021.

click to enlarge

In 2018 Russia’s construction output registered a higher-than-expected growth of 2.4%, thanks to the partial revision of construction statistics and the completion of major infrastructure projects related to the FIFA World Cup. In 2019, though, with the disappearance of these two growth factors, construction output is set to be near zero. Forecast for 2020-2021 is more optimistic (2.8%-3.3% per year) as economic growth is expected to accelerate and state funding for the industry will likely have a major push. Civil engineering and housing construction will enjoy most state funding directed to new road and railway projects, energy infrastructure and residential real estate developers.

In August 2018 the economy of Turkey trembled owing to the massive depreciation of Lira that greatly hit many sectors, especially construction. Building permits also dropped sharply last year, after historical peaks a year earlier, but completion of buildings in terms of floor area rose by 5%. This trend continues in 2019, but housing sales declined by 20% in the first five months, together with large decreases in real housing prices.Further, building material output registered a more than 20% drop within a year until May 2019. Construction companies experience a hard time and those active in civil engineering have decreasing workloads due to the presidential decree (issued in October 2018) not to tender new projects except for priority ones. Plus, the budget to central and local governments for projects this year is less than last year. Against this backdrop, recovery in the construction sector can only begin in 2021.

The Ukrainian construction industry has all the conditions for a sustainable growth in the future by an estimated 6.8% rise this year, a 3.6% increase in 2020 and a 7.2% growth in 2021. A positive trend is the systemic state support for the industry, including more transparent and clear rules of the game in the construction market, simplification of permits, and powerful investment support, especially in civil engineering. Hindering construction industry, and the economy as a whole, though, is the lack of financing. The slight drop in residential construction is offset by the growth of non-residential and civil engineering subsectors.

____________

Source

of data: EECFA Construction

Forecast Report, 2019 Summer

EECFA (Eastern European Construction Forecasting Association), conducting research on the construction markets of 8 Eastern-European countries, released its 2018 Winter Construction Forecast Reports on 5 December 2018. Key findings are summarized below. Full reports can be purchased, and a sample report can be viewed at www.eecfa.com.

In many previous forecast rounds we have argued for a soft-landing scenario in Turkey. However, the dramatic fashion of the currency depreciation in summer 2018 unearthed many structural problems of the construction industry and made us revise our forecast to an even more pessimistic one. Unlike the stop-and-go like reactions to previous crises, we tend to believe in a stop-and-stay scenario this time. In Russia, we are less pessimistic thanks to a recently announced governmental program expected to affect the market positively.

Optimism still prevails in the Eastern and Western Balkan countries of EECFA. For the region as a whole the new forecast sees just a little downward revision. However, on country level, the stories are different. Less optimism in Croatia and more optimism in Serbia and Slovenia compared to the previous forecast round. In Romania, the largest construction market of this region, the outlook of the building construction submarket has been adjusted downward.

Bulgaria. Construction output in Bulgaria is speeding up with an expected growth of 7.4% in 2018. Residential construction continues to expand on the back of increases in economic activity and real disposable income, and historically low interest rates on housing loans. Additionally, the non-residential segment is also predicted to grow driven mainly by office and industrial constructions. Civil engineering construction has continued its recovery path in 2018, Continue reading EECFA 2018 Winter Construction Forecast

Due to its coastal geography, Croatia is exposed to the effects of climate change such as rises in sea level and serious wave and storm threats. In the near future, the country will need to take action which will involve increased civil engineering construction on the coast.

Written by Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members

Croatia’s building boom is continuing, but some of the engines currently driving it will likely run out of steam in a few years: Coastal hospitality-related construction will decline in importance as current renovation and greenfield projects complete and opportunities for new projects become more limited. Educational, health and other construction spending fueled by EU post-accession funds will decline as those funds dry up.

All of this is several years off, and inland hospitality construction and renewed office and residential building will take up some of the slack, so there’s no need to panic. But, it’s still worth asking: what will be the next big thing in the Croatian construction market?

The Eastern European Construction Forecasting Association (EECFA) – the forecasting association conducting research on the construction markets of 8 Eastern European countries – has released its 2018 Summer Construction Forecast Reports up to 2020. The main findings of the reports are summarized below. The full reports can be purchased, and a sample report can be viewed at eecfa.com

Construction up to 2020 in ‘South-East Europe-5’ (Bulgaria, Croatia, Romania, Serbia, Slovenia)

The region is posting a strong economic growth which is fuelling building construction. Some of the region’s housing markets are seeing record-breaking results, so the first voices for overheating appeared. We think these markets are far from it, though. At the same time, construction labour shortage, due to economic migration from these countries to Western Europe, is one factor giving cause for concern in the future. With accelerating absorption of EU funds, civil engineering is expected to contribute positively to growth all the way on the forecast horizon.

Bulgaria

Construction output in Bulgaria continues its recovery and is expected to reach an 8.8% growth in 2018. The star performer is the residential construction segment, benefitting from improved employment and real disposable income, as well as the ongoing process of the concentration of population in big cities. Additionally, the steady economic development will increase investments in non-residential projects. Civil engineering construction is forecasted to contribute strongly in the next few years after EU fund absorption started catching up. Therefore, estimations for 2019 and 2020 are for an additional growth of 7.1% and 6.0%, respectively.

Croatia

Croatia’s construction output is likely to grow at a respectable rate until 2020 (by an estimated 2.2% in 2017 and a forecast 11.6%, 6.2% and 4.0% in 2018, 2019 and 2020, respectively). Particularly well performing sectors include hotel construction, education and health and certain civil engineering subsectors, especially railways. A global trade war, fallout from the Agrokor crisis and rapidly rising construction costs are threats to Croatia’s construction industry. And all are now significantly more likely to occur than they were at the time of EECFA’s 2017 Winter Report. But fortunately, none yet constitutes an imminent danger. In 2021 or soon thereafter growth will probably begin to tail off in a number of important sectors as Croatia’s catch-up phase gradually comes to an end, but exactly when and how this will occur is not yet clear.

Romania

The housing and non-residential segments are set to continue their excellent performance in 2018, and, in spite of an underwhelming performance in the civil engineering segment, the total growth of the construction sector in 2018 is forecasted to reach 7.1% (up from +6.8% in Winter 2017). As projects co-funded by the EU are starting to be implemented, Continue reading EECFA 2018 Summer Construction Forecast

EECFA (Eastern European Construction Forecasting Association) – the forecasting association conducting research on the construction markets of 8 Eastern-European countries – published its 2017 Winter Construction Forecast Reports on 4 December. A concise summary on the main findings is outlined in this article. Please consider that foreseen development stories are rather different for the 3 submarkets (residential, non-residential, civil engineering) of construction in the countries we cover. In Russia, for example, civil engineering is expected to drive the total market back to expansion. Unless you need only an impression about the total market, we kindly suggest consulting with our reports.

Construction outlook up to 2019 in South East Europe: the countries EECFA dubs ‘South East Europe-5’ are Bulgaria, Croatia, Romania, Serbia and Slovenia. The overall picture is still very optimistic, but the expansion rate of the total construction market has been revised a bit downward, mostly due to the worsened expectation in EU fund absorption on the forecast horizon. This affects largely the civil engineering submarket, where 9% cumulated growth is foreseen for 2018-2019 for the region as a whole. In a very favorable macro environment where money is cheap, building construction is set to continue to recover; with a 17% cumulated market growth predicted for the upcoming 2 years. Shortage of skilled labour in construction is a major constraint of a more rapid growth, though.

Bulgaria: the country is facing a 7% growth in total construction output in 2017 as EU funds of the new cycle are fuelling civil engineering construction which dragged down the whole sector in 2016. Thus, total construction output comes from a very low level; in 2016 it nosedived by 35.2% (compared to the forecasted 31.1%). In 2018, the construction sector is set to register a 5.6% increase (as opposed to the 6.4% forecasted earlier), while 2019 should bring a 5.7% rise (up from the +4.5% predicted formerly).

Croatia: the good news for construction growth in Croatia is the country’s increasing capacity to obtain EU funds, at which the current government seems to be getting better and better. Continued strong growth in GDP, private consumption, retail turnover and industrial production should also benefit construction. Total construction output growth is estimated to be 6.3% for 2017, which has been revised down from the 11.2% growth expected in summer due primarily to caution shown by buyers, bankers and developers in the residential segment and to delays in some government-led, civil-engineering projects. Continue reading EECFA 2017 Winter Construction Forecast and Revision

We have released our summer construction forecast on 16 June 2017 on Bulgaria, Croatia, Romania, Russia, Serbia, Slovenia, Turkey and Ukraine. This post intends to summarize the most important projections for these construction markets for the years 2017-2019. These are our main findings; for a deeper understanding, please consult our reports. You can contact us on eecfa.com.

Outlook for the EECFA regions

The highly optimistic outlook for South East Europe is maintained by EECFA. Leaving behind the transitory 2016, when the absorption of funds available in the new EU programming period (2014-2020) was still at a low level, the upcoming years are characterized by a bigger expansion of the construction market than that of GDP. Building construction is predicted to well outperform the total market, with a yearly average rate of 9% over the horizon. The small growth in the region’s total civil engineering market is attributed to the negative expectations in Romania.

Sideway moves, no further market expansion on the horizon are what we consider the most probable scenario for the 3 East European markets together. Turkey and Russia, being far the two biggest markets we cover in EECFA, is expected to show some similarities. In both countries our forecasts are moderately optimistic in the civil engineering market. While in the building construction market the outlook is clearly negative for Russia and neutral for Turkey. In Ukraine, the recovery experienced in 2016 is predicted to be sustained until 2019. Both building construction and civil engineering could expand further with a relatively good pace. Continue reading EECFA 2017 Summer Construction Forecast and Revision

Earlier this year, Croatia’s construction industry at last seemed on track for recovery after many dismal years of negative growth. 2015 saw a number of construction sectors moving into positive figures for the first time since 2009, but the recovery really took hold last year with all construction sectors likely to show positive growth once complete data for the year are available. Now, though, the Agrokor crisis has thrown this rosy picture into doubt.

Written by Michael Glazer, SEE Regional Advisors and Tatjana Halapija, Nada Projekt – EECFA Croatia

Illustration of Agrokor HQ (Croatia) photo by Zeljko Hladika, source: http://www.24sata.hr

First, some background. The Agrokor Group is by far ex-Yugoslavia’s largest business conglomerate, with EUR6.4 billion in sales in 2015. Indeed, it is one of Central Europe’s largest companies (11th, according to Deloitte’s Central Europe’s Top 500 2016) and its second largest retailer (behind Poland’s Jeronimo Martins Polska, also according to Deloitte). Among other things, Agrokor owns the biggest retail grocery chains in Croatia, Slovenia, Serbia and Bosnia-Herzegovina (BiH), several large Croatian agricultural producers, important Croatian resort projects, significant travel agencies and major distribution companies for the wholesale and HoReCa sectors in Croatia and BiH.

Agrokor is now in serious trouble. It is having difficulty finding liquidity, a government administrator has been appointed for it by the Croatian government, the Slovenian and Serbian governments are considering similar measures and it is making only limited payments to its suppliers, on its taxes and to its lenders.

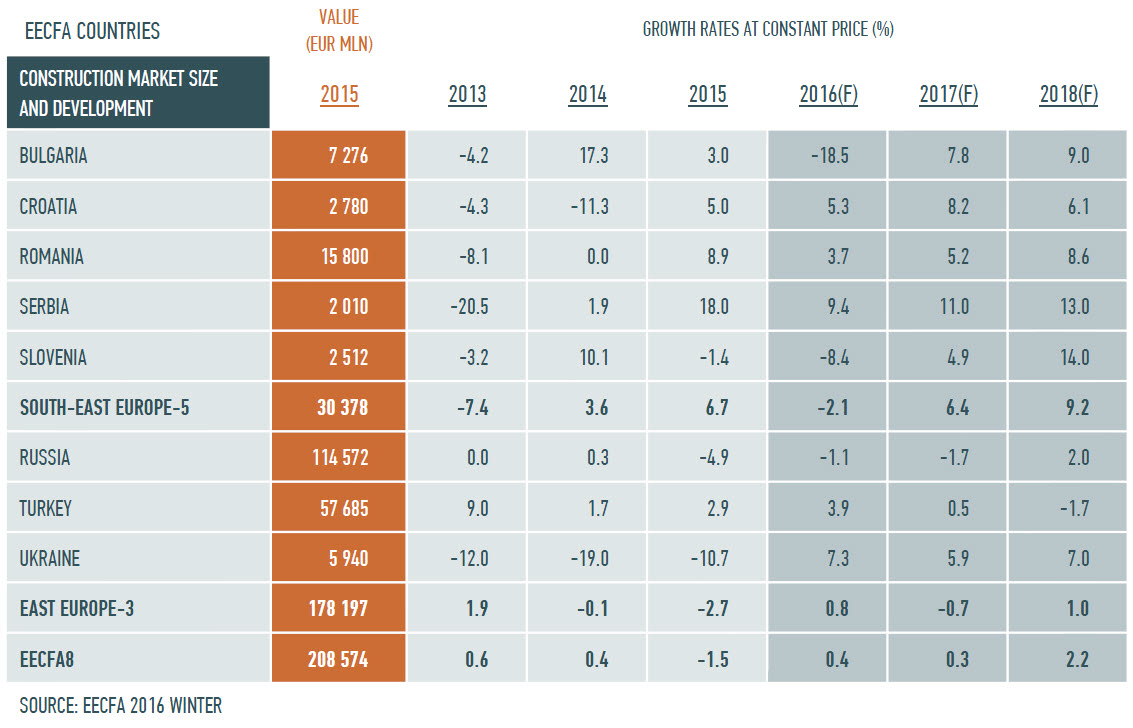

EECFA has released its winter construction forecast reports on 2 December 2016. In this post you will find the concise summary on our expectations for the 8 construction markets we are dealing with: Bulgaria, Croatia, Romania, Russia, Serbia, Slovenia, Turkey and Ukraine. You can also find us and our reports on eecfa.com.

Regional outlook

South-East Europe is very optimistic. After the transitory 2016, when shrinkage in the civil engineering market in the EU countries of the region dragged down the region’s total performance, high growth is expected to characterize the total construction market in the upcoming years. Each EECFA country of the region predicts an expansion beyond 5% for 2017 and a further increase for 2018. Building construction, coming back from low levels, is predicted to expand faster than civil engineering in 2017.

Eastern Europe is at a standstill as a whole. In Russia, we expect a prolonged decline. The total construction market is not predicted to expand before 2018, and we believe that the growth of civil engineering sub-market can only alleviate the loss awaited in building construction in 2017. In Turkey, our stories for the upcoming years is rather similar to that of Russia, slight optimism in civil engineering, slight pessimism in building construction leads to a total market which is not predicted to grow until 2018. In Ukraine, all-round recovery is forecasted. From the very low levels, we expect relatively high growth rates for 2017 and 2018.