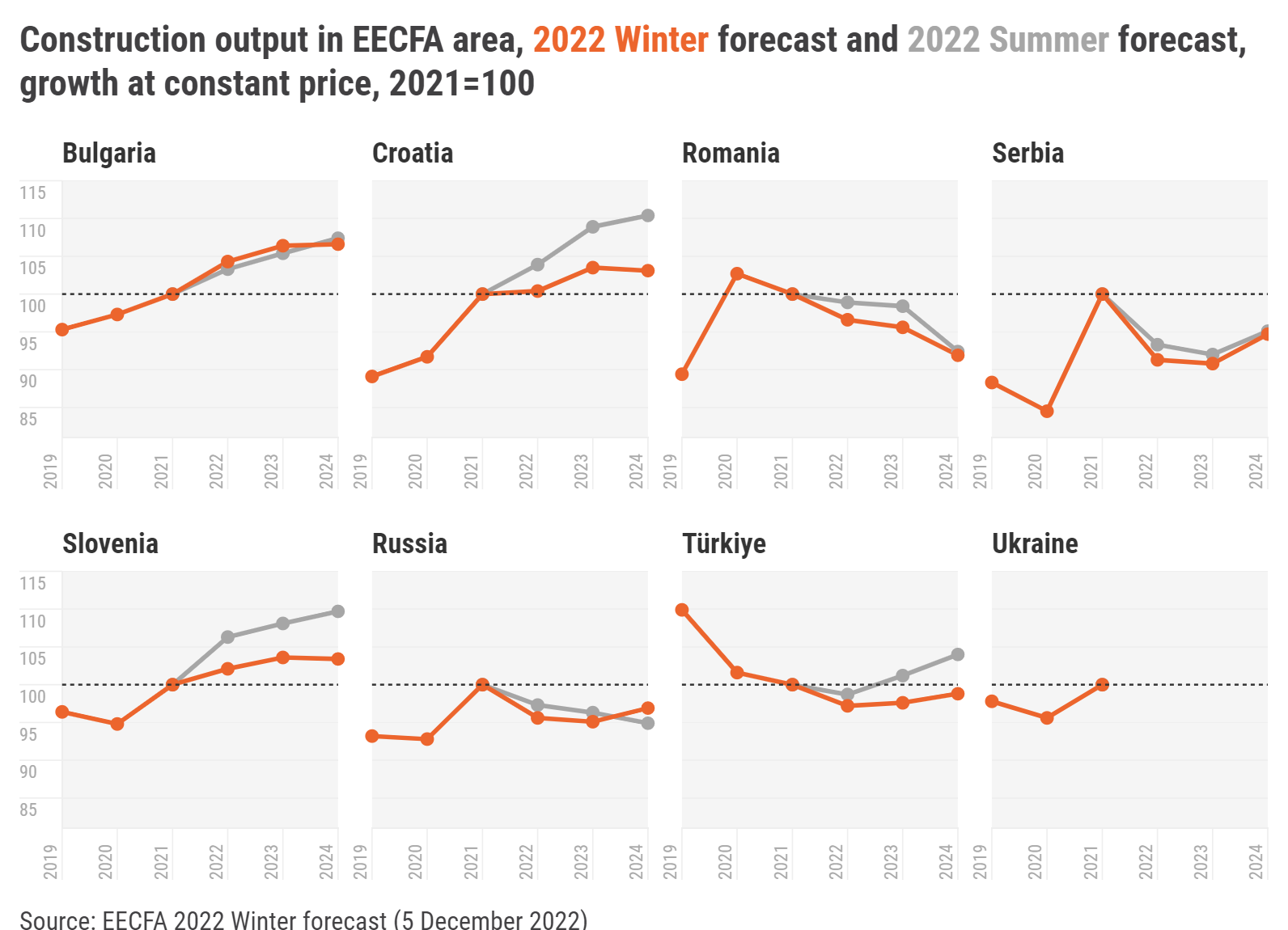

EECFA, which celebrates its 10th anniversary this year, released its 2023 winter construction forecast on 15 December 2023. The new reports can be purchased, and a sample report can be viewed at eecfa.com.

No clear direction in the Southeast European region of EECFA; 2024 is foreseen to experience a decline, but a comeback is our current scenario for 2025. Expansion is projected to prevail all the way until the end of the forecast horizon in the East European region.

Romania is expected to contribute most negatively to the shrinkage of the SEE region in 2024. The rest of our countries is forecast to perform better. Bulgaria, Croatia and Serbia could end up at higher level in 2025 than what was experienced in 2023. Upswing in Türkiye is envisaged to pull the EE region up and we still believe that shrinkage in Russia is about to come. Not a particularly strong, but recovery is projected in Ukraine.

Construction outlook up to 2025 in Southeast Europe

Bulgaria’s economy is expected to lose momentum in 2023 that will translate to a lower, yet positive growth in 2024. Against this backdrop, construction output is to follow this trend with heterogeneous performance on segment level. While in the forecast period till 2025 civil engineering and non-residential construction will likely contribute with positive growth figures, after several strong years, residential construction is predicted to witness a new normal with negligible annual growth rates from 2024 onwards if any.

Croatia’s construction output will continue to grow, rapidly in 2023 and less robustly in 2024 and 2025. Civil Engineering construction is poised to become the brightest star in the country’s construction firmament with Buildings showing considerable sector to sector variation, but overall not performing as strongly as in the past.

Romania’s construction is expected to shrink in 2023 in real terms. Economic growth is slowing down under sticky inflation and high financing costs. Further slowdown might come in 2024 as multiple elections, political pressure to lower budget deficit, high social spending and the transition to the new EU programming period would make it challenging to focus on public projects. The outlook doesn’t look better on the private investment side with tight labour market and sluggish consumption growth expected for 2024. By 2025, return to growth is postulated as most of these obstacles may dissipate.

During 2023, Serbia has been performing better than initially expected with the economy picking up in the second half of the year and construction outputs registering another record high. While the construction of buildings is consolidating in a moderate manner, civil engineering surged with a double-digit growth rate. The easing of inflationary pressures is also helping market stabilization, while high interest rates remain a major impediment for growth in short-term.

Slovenia’s construction industry in late 2023 faces economic challenges exacerbated by unprecedented floods in August, causing EUR 10 billion in damages. Despite workforce shortages leading to increased construction costs and inflation, the sector is expected to see a significant rise in output with civil engineering projects, including flood repairs and infrastructure initiatives, driving growth. However, concerns arise over the potential deceleration in growth in 2024 and 2025, mostly in residential and non-residential construction even as reconstruction efforts in civil engineering gain traction.

What to expect in the Eastern European construction markets of EECFA

In Russia, stable government support, a relatively favourable macroeconomic environment, and the general resilience of the industry to external challenges ensured positive dynamics in construction in 2023, making the forecast more optimistic for this year. The industry’s development strategy prioritizes housing construction as well as transport- and energy-related projects. The positive momentum is not predicted to last long, though, and in the 2024-2025 horizon we might observe contraction in construction market volume, mainly due to the expected decline in the residential market which might outweigh the positive dynamics in other subsectors.

Türkiye’s economy has been impacted by two developments with one being the reconstruction of collapsed buildings and infrastructure in recent earthquakes where most tax revenues went, causing large monthly budget deficits. The other one is increasing interest rates. Although the Central Bank increased the base rate from an 8.5 base point level to 40 in six successive months, it couldn’t curb inflation and there are exchange rate rises along with inflation. The construction sector grew at higher rates than the GDP as the national average on the back of building construction in earthquake-hit provinces. Growing interest rates reversed most of the problems caused by the low-interest rate policy, but it also led to an increase in construction cost and hit the affordability of purchasing homes.

Ukraine’s construction market has been struck by the ongoing war. According to official data alone, almost a million flats, tens of thousands of non-residential buildings, thousands of kilometres of roads, railways, bridges and other infrastructural facilities were either destroyed or damaged. The construction industry partially lost its raw material base and production as most metallurgical enterprises located in the south and east were destroyed or occupied. The main construction segments that can predictably develop even during the war are the restoration of damaged housing and social infrastructure, civil engineering, construction and modernization of industrial production.