There was no construction start indicator in Romania, so we have created an estimation for it.

This poster is a summary of our monthly findings. It shows how the total value of started construction works have changed over the same period last year. Besides, it presents which segments have the biggest start value in the current year. We call this indicator Project-Start. And they are computed every month for 18 construction segments by aggregating data of construction projects. The projects are from the iBuild database and ELTINGA and Buildecon found the way of creating indicators out of them.

If you need short-term foresight, you will like it.

Brief comment from Janos Gaspar, head of Buildecon:

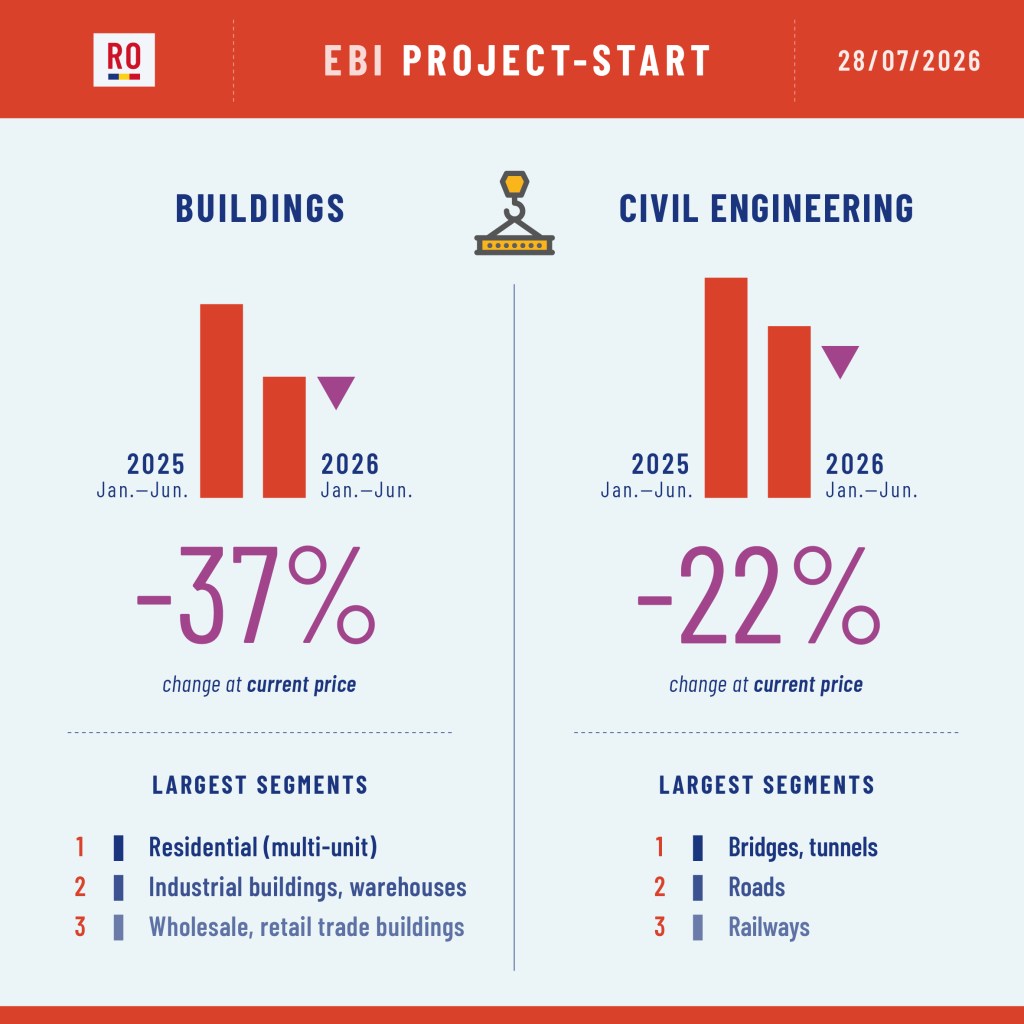

Project-Start is still much weaker in building construction than this time last year. Within building construction, the multi-unit residential submarket experienced the bigger drop, the total value of started works halved from a year ago. The drop in non-residential is less harsh, but still significant. And it is driven by the declining Project-Start in the publicly financed segments (education, health, other non-residential). Thanks mostly to the works commenced on A8 Motorway and the Bucharest-Giurgiu railway line, civil engineering is still strong, despite the double digit drop.

We have renamed our indicators for the sake of easier understanding; from now on we refer to the total value of started/completed construction works as Project-Start/Completion. In the EBI Construction Activity Visualization and Report we are also switching to the terms of Project-Start/Completion instead of the previously used Activity-Start/Completion.

Every month this poster will be available here on our blog. If your interest is deeper, we have the EBI data visualization (with indicators for all the 18 segments of the construction market), updated monthly and we have the EBI Construction Activity Report Romania (with data and explanations), published quarterly in English and in Romanian. All these are packed into a yearly subscription. For the specifics, please contact us.

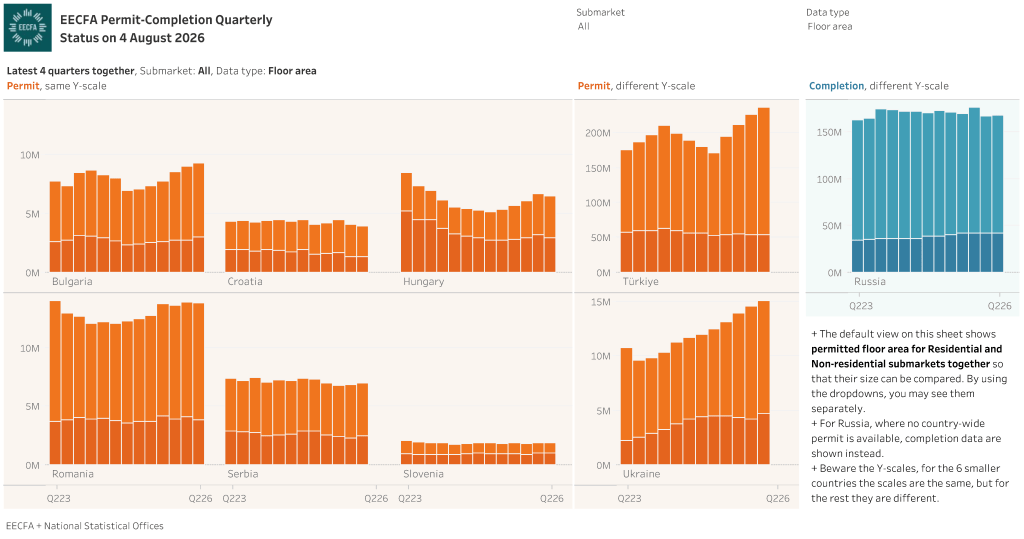

The viz was updated on 4 August 2026. → The latest data of Bulgaria are very promising, recovery in Hungary stopped. (The visual is updated continuously, the text will be refreshed when all data are published.)

Optimism in Croatia and Serbia prevails. Both countries experienced massive permit expansions between 2014 and 2022 and both have remained close to their peak ever since. Croatia has had around 4 million, while Serbia has had around 7 million permitted m2 for over four years. Slovenia remained below its 2022 high despite the positive correction in Q1 2026. Expansion continued in Bulgaria and the 9 million m2 was reached, a record in the last 15 years. Recovery in Romania and in Hungary is ongoing, led by residential projects.

You may use the dropdown in the viz for selecting either the residential or the non-residential submarket, or both.

In the full visualization, not only permit but completion data can be followed (where available).Just click on the Country-by-country sheet.

Figures in Türkiye are getting extremes, representing the highest optimism since 2017. Residential projects drive the growth, 1.25 million dwellings obtained construction permit in the last 4 quarters. (From Q2 2025 on, permits issued by authorities other than the municipalities are also published by TUIK. So the scope is bigger, the results show the full picture. Click through the below viz for understanding the size and the impact of this revision.) Q1 2026 has been the best quarter in Ukraine since the beginning of the war. This was the first quarter, however, when residential was not able to grow. After the strong year-end, 2026 started with shrinking completion in Russia.

This visual about the significance of the permit revision in Türkiye was compiled back in September 2025.

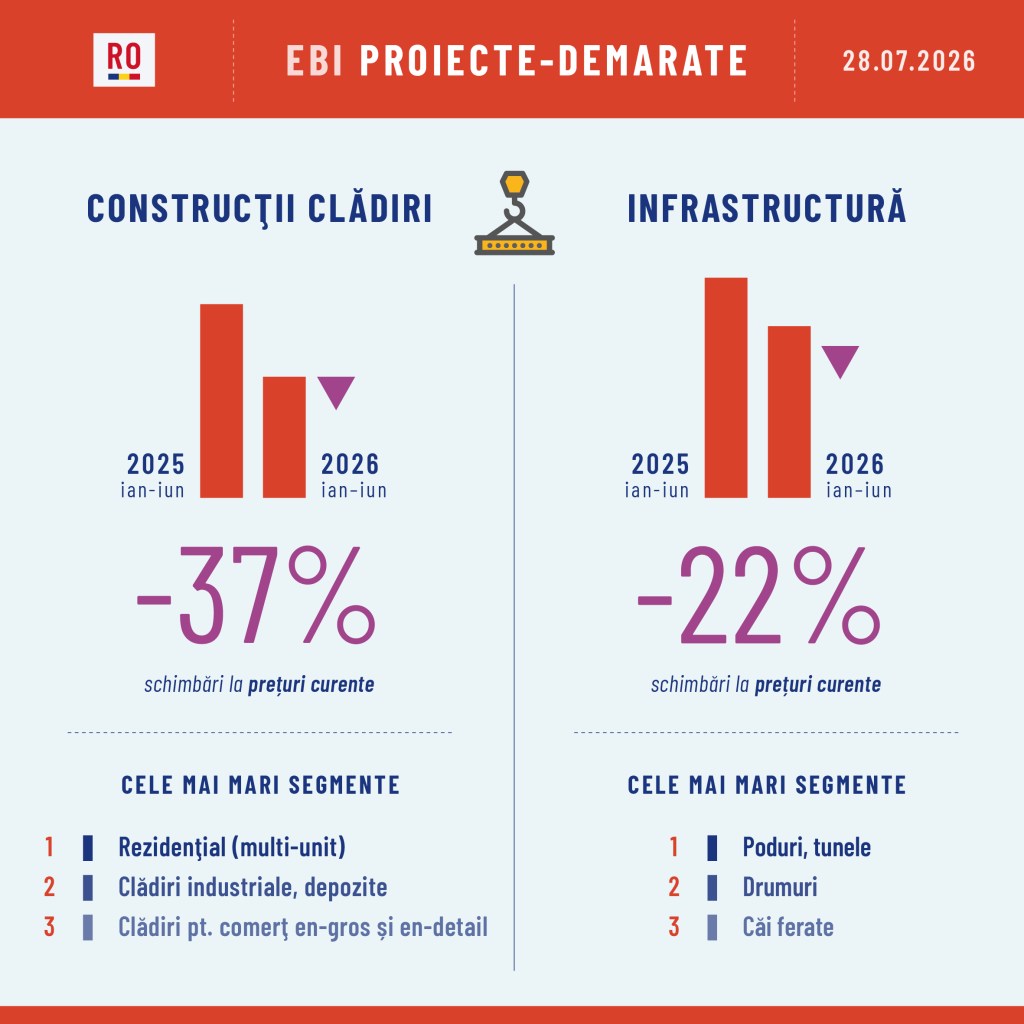

Az első félévben erős volt a Projekt-Kezdés a társasházi lakásépítés részpiacon. Igaz, a tavalyi évhez képest jelentős a visszaesés, de az volt a csúcsév. A nem-lakás magasépítési részpiacon továbbra is nagyon alacsony a megkezdett kivitelezések összértéke. Kis pozitívum, hogy az ipari épületek és raktárak szegmensben megállt a drasztikus csökkenés. Két erőmű kivitelezésének elindulása miatt a mélyépítés részpiac sokkal jobban fest, mint tavaly, de erősnek még így sem mondható a Projekt-Kezdés.

Átneveztük a mutatószámainkat a könnyebb érthetőség kedvéért; mostantól Projekt-Kezdés/Befejezés néven utalunk a megkezdett/befejezett kivitelezési munkák összértékére. A vizualizációban is a korábbi Aktivitás-Kezdés/Befejezés helyett a Projekt-Kezdés/Befejezés kifejezésekre térünk át.

A poszter a két nagy építési részpiac Projekt-Kezdés indikátorának időszak/időszak változását mutatja, valamint a szegmenseket amelyekben a legnagyobb értékben indultak kivitelezések. Ezt a posztert minden hónapban kitesszük ide a blogunkra. A teljes építési piacot részletesen bemutató EBI Építésaktivitási Adatvizualizációt (összesen 18 szegmens adataival) is havonta frissítjük, és negyedévente az EBI Építésaktivitási Jelentésben is elmondjuk, hogy mit látunk a piacon. Ha érdeklik a részletek akkor a contact oldalon írjon nekünk.

In the first half of the year Project-Start was strong in the multi-unit housing construction submarket. True, the decline is significant compared to last year, but that was the peak year. In the non-residential construction submarket the total value of started construction works is still very low. The silver lining is that the massive decrease in industrial buildings and warehouses segment has stopped. Due to the start of construction of two power plants, the civil engineering submarket looks much better than last year, but Project-Start cannot be said to be strong.

We have renamed our indicators for the sake of easier understanding; from now on we refer to the total value of started/completed construction works as Project-Start/Completion. In the visualization, we are also switching to the terms of Project-Start/Completion instead of the previous Activity-Start/Completion.

The poster (above) shows the period/period changes of the Project-Start indicator in the 2 main submarkets and the segments with the largest value of started works. This poster is published every month here in the blog. The EBI Construction Activity Data visualization with the details on the whole construction market (with altogether 18 segments) is also updated monthly and the EBI Construction Activity Report, summarizing what’s happening in the market, is published in each quarter. If your interest in construction markets is deeper, please contact us for the details.

Written by Tünde Tancsics – ELTINGA, EECFA Research

Similarly to every summer, ELTINGA (EECFA Research) has now examined how the European Commission sees the EECFA countries. Here is the summary of the major changes in economic prospects between the Autumn 2025 and Spring 2026 forecasts.

The economic outlook has deteriorated across almost all countries in the region compared to Autumn 2025, although growth projections remain positive. Serbia, Romania and Slovenia experienced the most significant downward revisions (-0.4 percentage points), while Bulgaria and Croatia underwent only slight adjustments (-0.05 to -0.1 percentage points). Russia was the only country whose projected growth marginally rose. Growth expectations for the EU and the Euro Area also fell moderately, reflecting a general weakening of economic momentum across the region.

In 2026-2027, average GDP growth is forecast to be positive in all countries, albeit to varying degrees. Türkiye is expected to lead the group with a growth of 3.5%, followed closely by Serbia (+3.35%). Meanwhile, Russia and Romania are forecast to have the smallest expansion (+1.2%). Croatia (+2.6%), Bulgaria (+2.35%) and Slovenia (+2.1%) are projected to perform in the middle of the range. The Euroconstruct member Hungary is predicted to grow by 1.95%, which is above the EU average. Despite the general downward revisions, most of the countries in the region are expected to do better than the EU (1.25%) and all of them will likely surpass the Euro Area (1.05%), maintaining the pattern of stronger growth dynamics in East and Southeast Europe.

Since the Autumn 2025 forecast, the projected growth rate of gross fixed capital formation in the region for 2026-2027 has been revised in both directions. The steepest cuts were seen in Bulgaria, in Serbia and in Romania where projected GFCF growth dropped by 0.8-1.75 percentage points. Meanwhile, Hungary, Slovenia, the EU, the Euro Area, and Russia recorded more moderate downward adjustments, while Türkiye and Croatia saw upward revisions. Serbia is still projected to lead in GFCF growth at 5.15%, followed by Türkiye (4.2%) and Romania (3.2%). Bulgaria (1.25%) and Russia (0.35%) remain at the lower end of the spectrum. The EU (2.1%) and the Euro Area (1.75%) continue to lag behind most countries in the region.

Growth expectations for gross fixed capital formation in construction have been modified across countries where data is available, in both positive and negative directions. The most notable upward revisions occurred in Slovenia where projected construction investment growth increased by 1.55 percentage points to 4.9% (the highest in the group). Romania ranked second in terms of expected growth with 4.85%. Compared to Autumn 2025, Croatia saw a more significant upward revision in its projected growth rate (1 percentage point); the third largest increase in gross fixed capital formation in construction is expected there (3.05%). By contrast, Hungary and Bulgaria experienced the biggest downward revisions, falling to 2.95% and 1.6%, respectively. In the broader European context, construction investment is projected to rise only modestly to 1.85% in the EU and 1.6% in the Euro Area, remaining below most national forecasts in the region.

The Commission’s view on expected construction investment is quite different from ours. Partly it is because we examine the sector from the bottom. For each segment we come up with an individual story and this is how the total construction market is formed. Our latest forecast is in the 2026 Summer EECFA Construction Forecast Reports. Sample report and order

EECFA’s 2026 Summer construction forecast up to 2028 was released on 22 June. Sample report can be viewed at eecfa.com. To obtain the new reports, please contact us

Southeast European construction markets up to 2028

Bulgaria stepped into this year as the 21st member state of the eurozone in the middle of an evolving political turbulence that inevitably impacted the construction sector, most notably, projects that rely on public funding. Nevertheless, according to Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian member institute, Bulgaria’s total construction output is anticipated to increase by approximately 2% on average in the forecast period of 2026-2028. He also notes that “Last year Bulgaria’s construction sector excelled with a strong performance, largely thanks to the residential and non-residential submarkets which fared better than previously predicted. In 2026-2028, however, the country’s total construction output could see a heterogeneous performance.”

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s members for Croatia, point to funding from the EU’s Military Mobility Package (MMP) as a promising source of finance for a wide variety of Croatian construction projects. Transportation ones, both straightforwardly military and dual use, are obvious contenders, so the availability of MMP money should lift output in those civil engineering segments. MMP will likely boost some non-residential segments, too, since it can finance, e.g., factories and logistics centers (perhaps even flight schools?) that have a military or dual-use purpose. This will help sustain total construction output despite rapidly declining levels of finance under the EU’s post-2022-earthquake rebuilding programs and RRF. In non-residential generally, while some developments will affect all segments, specific factors will ensure that output growth varies greatly from segment to segment. The picture for energy construction is also confused, with solid, well-known technologies competing with much-hyped, as-yet-unproven, “hi-tech” alternatives. Residential is buffeted by the conflicting influences of rising prices, declining GDP growth and interventions by the central bank and the government.

Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild, notes that Romania’s construction market is still in a tight spot. “Growth potential is limited with global and national factors conspiring against it. Recent economic forecasts are more pessimistic; 2026 might see a stagnant GDP, declining real wages and the highest inflation in the EU. This is coupled with the looming specter of national deficit causing high taxation and austerity measures: lower public spending, and wage and hiring freezes for public employees. Not to mention that construction costs, which started evening out in 2025 after the 2022 shock, are now again on the rise due to climbing energy prices and labor costs. The saving grace of construction is the EU programs funding infrastructure projects. Yet, with the NRRP running out in mid-2026, and other programs having an inconsistent performance, the boost they can provide is limited. Adding to all this is a political crisis that could lead to a government change at a critical moment (the end of NRRP absorption, projects phased into other funding sources). But the silver lining: most of these issues should be transitory. By 2028 Romania’s construction might return to growth on the back of improved economic indicators, inflation levels within the target range, a more efficient energy sector, and hopefully, a more stable political situation.”

“Serbia’s overall construction output is still consolidating in 2026 led by the correction in civil engineering, while buildings continue to grow in this forecast” – according to Dejan Krajinović, EECFA’s Serbian researcher at Beobuild. He adds that the performance in the residential submarket remains stable and is predicted to continue to grow with moderate growth rates. Non-residential, on the other hand, is booming, driven by massive investments related to the EXPO 2027, with another year of double-digit growth expected in 2026. Main segments benefiting from ongoing developments are office, commercial and hotel, but health-related construction is also breaking records in 2026. The consolidation in civil engineering is anticipated to end in 2027, with new growth on the horizon in 2028 and onwards. The large-scale infrastructure projects in the pipeline should launch a next big growth cycle in overall outputs. However, the war in the Middle East is already pushing construction costs up and the economic uncertainty and fragmentation are still risks that continue to linger in the coming period.”

“Slovenia’s construction sector’s output was holding steady at just under €6bn in 2024 and 2025 but is set to edge higher in the forecast period, supported mainly by public spending” – says Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia. “Growth is increasingly uneven: residential construction remains constrained by limited supply and rising costs despite strong demand, while private non-residential segments such as offices, retail and industry face cautious investors and only modest expansion. By contrast, publicly financed segments, notably education, health and civil engineering renovation, are providing stability, with infrastructure upgrades, railway investment and energy-transition projects sustaining activity. Transport and utility constructions are shifting from large expansions to maintenance and modernisation, and investment in electricity networks and pipelines is set to rise further due to the energy transition. Overall, the sector is moving into a more stable but slower phase where public policy and infrastructure spending play a decisive role in keeping output on track – as long as public financing remains available.”

Eastern European construction markets up to 2028

According to Andrey Vakulenko at Macon, EECFA’s Russian research institute, the downward trend in Russia’s construction market, which began in 2025, is likely to continue and intensify in 2026–2027. The main reason behind is the combination of a decelerating economy and a prolonged period of high interest rates, which negatively impacts demand, limits the availability of financing and restrains investment activity. Residential construction is experiencing the strongest pressure as the market struggles to find a new balance amid reduced mortgage availability, declining demand and decrease in new construction. Most non-residential segments may also show negative dynamics in the coming years impacted by the slowdown in consumption volumes and business activity, weak household income growth and changes in the direction and scope of government funding in certain segments. Civil engineering will likely stay the most resilient subsector due to the implementation of major transport and energy projects. The planned acceleration of infrastructure construction, the expected growth in the residential submarket and the easing of monetary policy are the conditions for the construction market to return to a growth trajectory in 2028.

“In Türkiye, state involvement in housing development has grown in recent years” – say Prof. Ali Türel and Prof. Leyla Alkan Gökler, EECFA’s Turkish researchers. “Policies to curb inflation have depressed households’ disposable income, creating a serious housing affordability issue for both ownership and renting as home prices and rents have spiked. As moderate-to lower-income households have found it increasingly difficult to accumulate sufficient equity for home purchases, the government has intervened. It launched a large number of residential projects for dwellings that can be bought on affordable terms by households not owning a house in Türkiye. Dwellings will be built by the Housing Development Administration (HDA), the key state actor in housing production in Türkiye. Since HDA has also been involved in rebuilding the about 550,000 dwellings damaged in the February 2023 quake, the share of housing built by the public sector has greatly risen in recent years, while the share of the private sector has been declining from its former share of about 90%. Our latest forecast indicates that total construction output in Türkiye may reach nearly 8 trillion TL (nearly EUR 180 billion) in 2028, at 2025 prices.”

“Ukraine’s construction market exhibited high resilience in 2025 despite the ongoing war and challenging security conditions. While it is recovering and it nominally returned to pre-war levels last year, it was still 40% below the 2021 output at comparable prices.” – notes Professor Sergii Zapototskyi at Uvecon, EECFA Ukraine. “Key growth drivers were commercial, industrial, warehouse, and logistics developments, an uptick in residential construction in relatively safe regions, and large-scale projects aimed to restore public and transport infrastructure. In the coming years, the construction market is expected to continue to grow, supported by post-war reconstruction needs, government housing support programs, and an increase in international funding for Ukraine’s recovery. The greatest growth potential will remain in residential, commercial, as well as industrial and warehousing construction. At the same time, the future performance of the market will largely depend on the security situation, the availability of investment resources, the ability to address labour shortages, and the effectiveness of government reconstruction policies.”

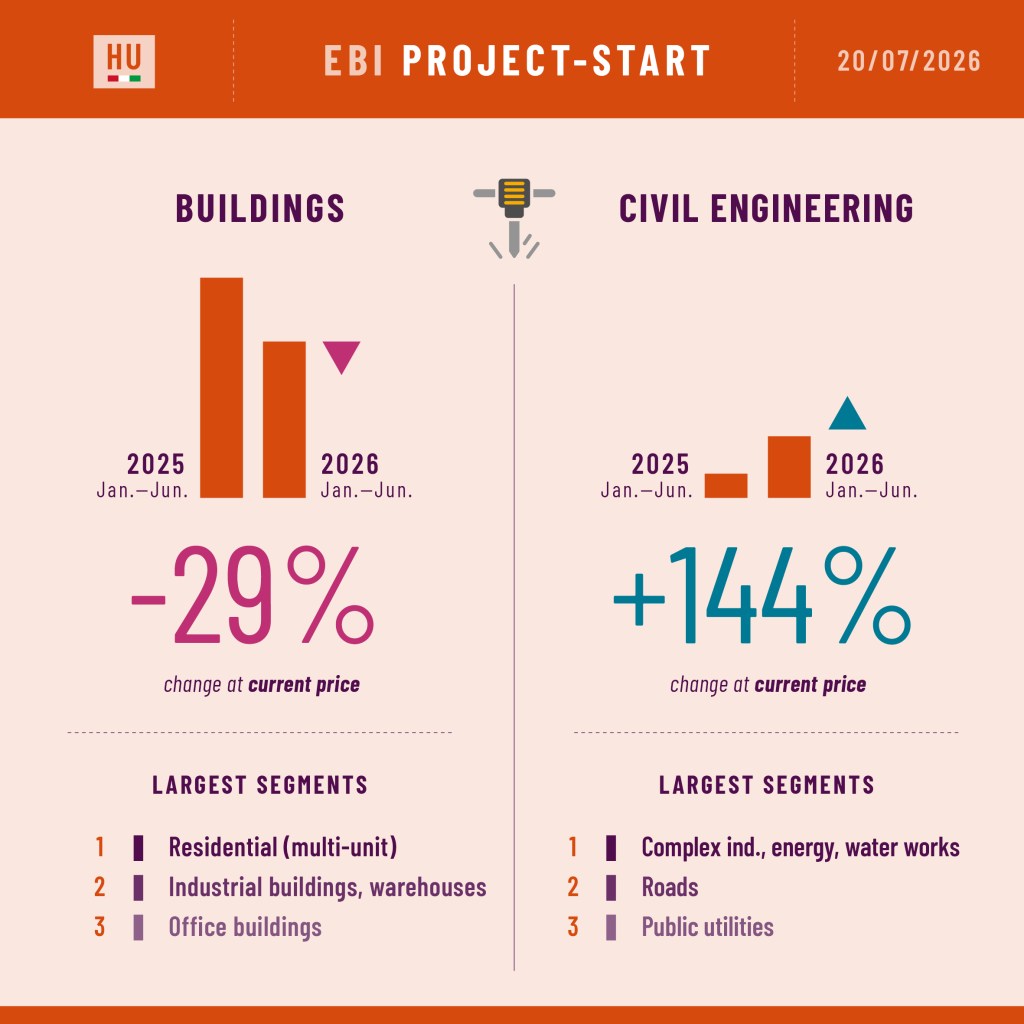

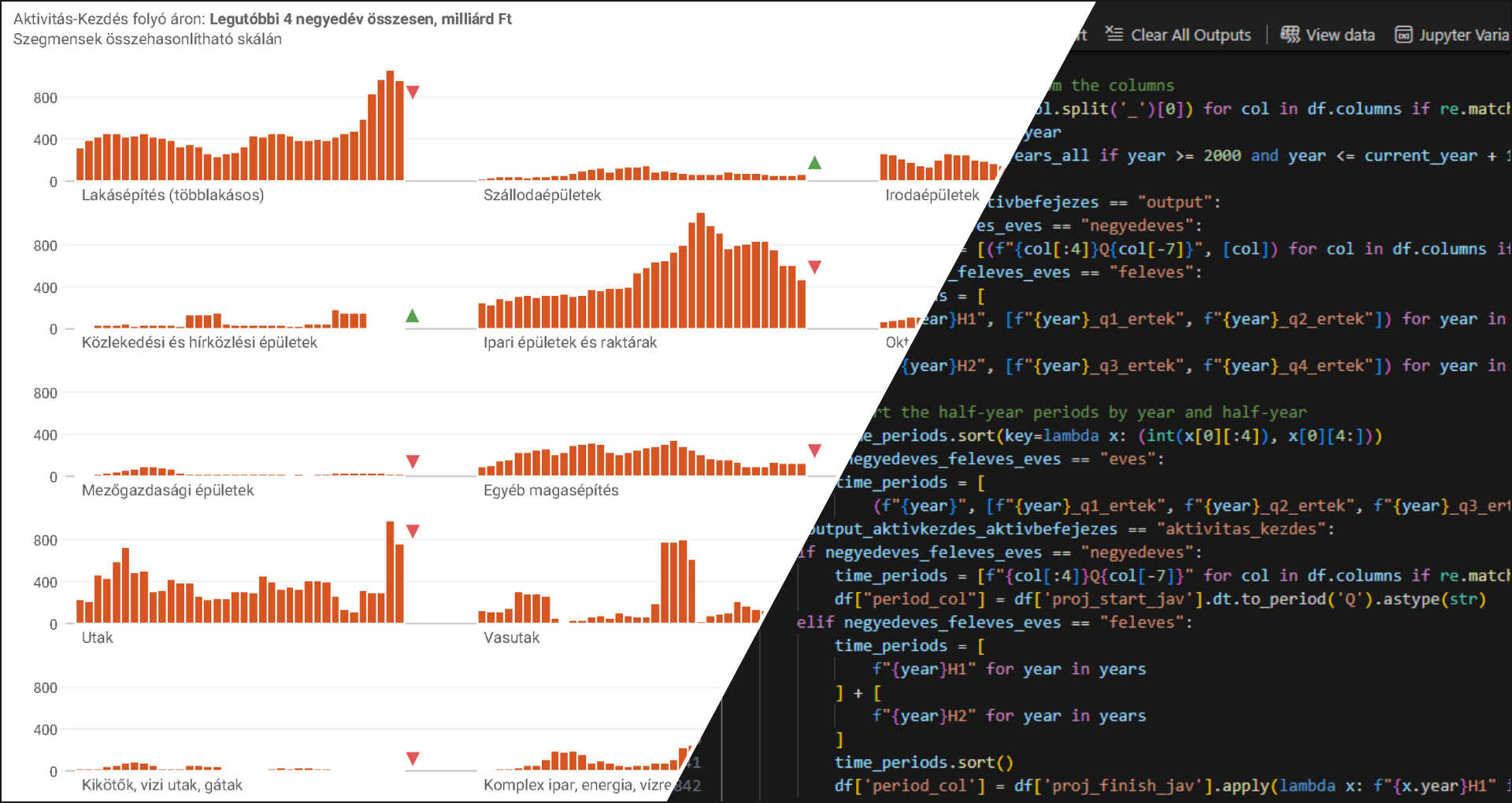

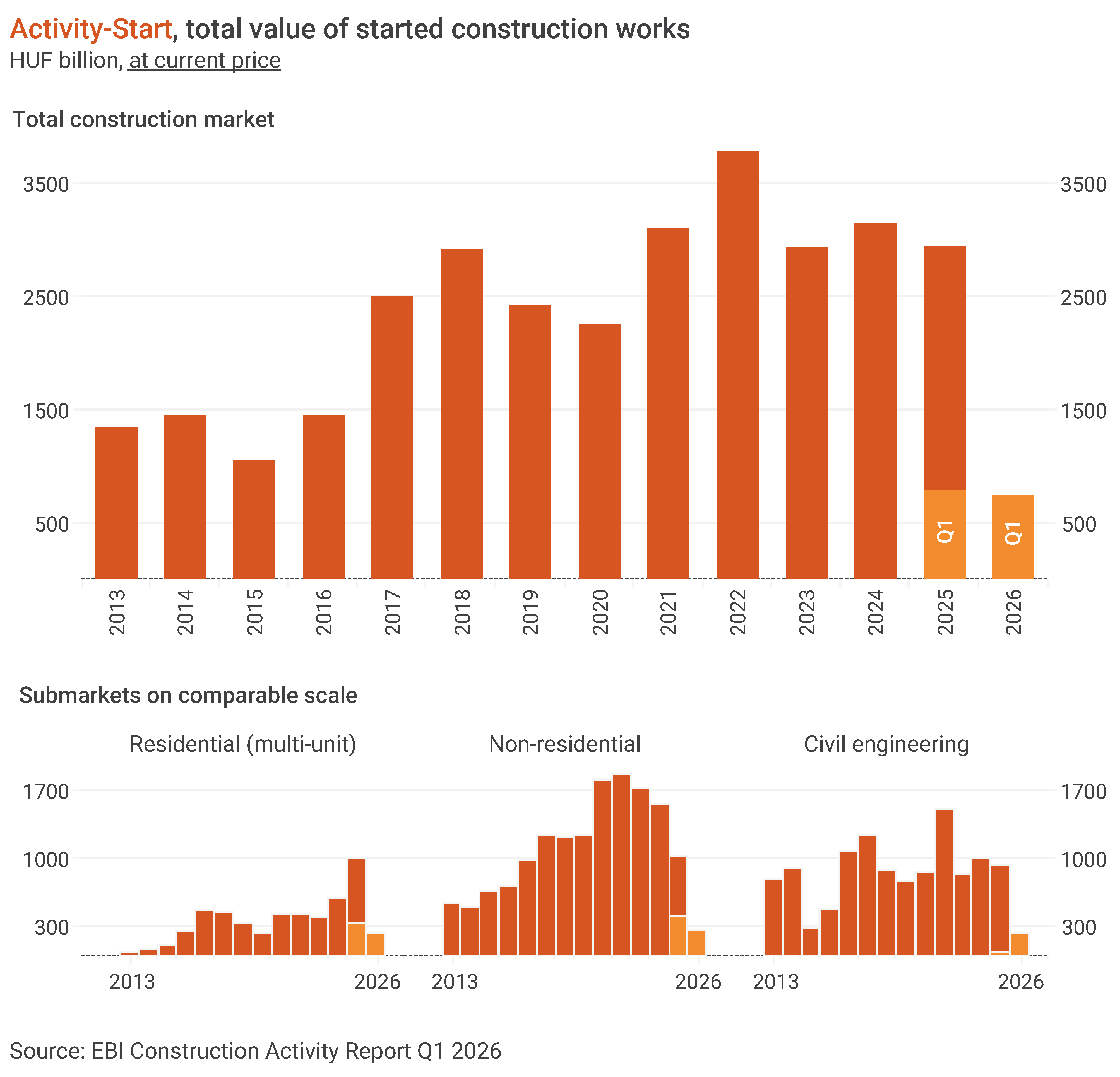

As per the latest EBI Construction Activity Report, 2026 did not start badly in Hungary for construction. Activity-Start in Q1 did not substantially lag behind Q1 2025 and Q1 2023, in fact, it slightly exceeded the average quarterly values of these years. At the same time, the start of foundation works of Block 5 of Paks 2 nuclear plant played a major role in higher numbers, adding a more nuanced picture. Projects worth around HUF 740 billion entered construction in Q1 2026. At constant price, Activity-Start did not lag greatly behind the same period of 2025 (-9%), but we have still seen the weakest first three months since 2016.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To obtain the report, please contact us.

Building construction returns to last year’s level

2026 started much weaker in building construction than last year, but the Activity-Start of around HUF 500 billion was roughly in line with the average quarterly level of 2025 and was only 6% below the average quarterly value of 2024. Hence, no major decline compared to the previous two years at current price. Even at constant price, the value of construction projects started in the first three months was close to the average quarterly level of last year, but it was double-digit below the average three-month Activity-Start between 2016 and 2024.

Multi-unit housing construction is still the segment keeping building construction at a higher level. Activity-Start for non-residential construction between January and March this year (HUF 263 billion) exceeded the average quarterly value of 2025, which was considered weak, but fell 33-44% short of the average values between 2021 and 2024. At constant price, this year’s first-quarter Activity-Start has been one of the weakest since 2015.

Biggest started non-residential projects in Q1 2026 comprised several logistics and office buildings such as Phase 3 of Láng-negyed V1 office building and Frontiers Campus office and research centre in Budapest, and the renovation of BorsodChem offices in Kazincbarcika, Phase 3 of CTP VCS5 Logistics Centre in Vecsés, building D of VGP Park Beta logistics centre in Győr, building B of Panattoni Logistics Park in Mosonmagyaróvár, and Phase 1 of Penny Market logistics centre cold storage in Alsónémedi.

Paks 2 boosted civil engineering figures

In Q1 2026, the value of started civil engineering works neared HUF 240 billion boosted by the start of foundation works of Block 5 of Paks 2 nuclear plant, while the Activity-Start in road and railway projects was only HUF 20 billion. Apart from Paks 2, only one civil engineering project got into the largest projects in Q1 2026: the construction of Phase 2 of the industrial park in Nyíregyháza.

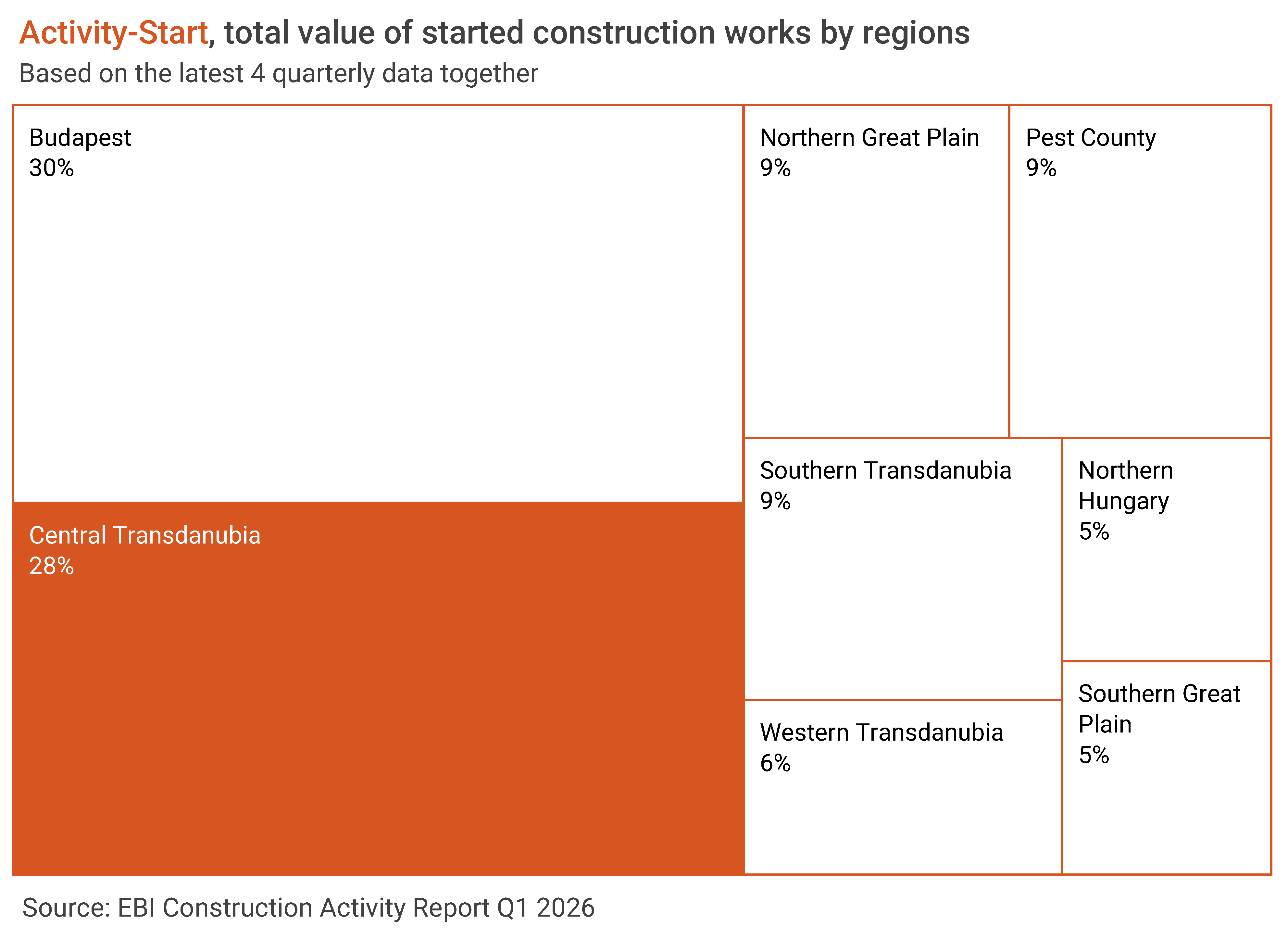

Budapest: regional heavyweight again

Budapest continued to be the region with the highest value of construction works started in Hungary with a share of 30% in total Activity-Start in Q1 2026. Based on the four-quarter moving averages, the share of Central Transdanubia was still considerably higher than in previous years thanks to the M1 motorway expansion launched in Q3 2025. Pest County, Southern Transdanubia and the Northern Great Plain accounted for about 9% of started constructions, while the share of other regions varied between 5% and 6%.

Multi-unit home construction still high

After a weaker final quarter last year, this year started with an extremely strong first three months for multi-unit housing. Between January and March, the value of started construction works exceeded HUF 240 billion at current price; the third highest quarterly Activity-Start since 2014. This value is significant even at constant price: only 2017-2018 and last year had stronger quarters.

The great increase in permits last year suggested strong activity at the beginning of this year. The latest EBI Construction Activity Report has found that many large projects have moved closer to planned start recently, also predicting a higher Q2 Activity-Start in the segment. However, there is a lot of uncertainty in the market now as projects within the Otthon Start Program are expected to be reviewed, which may change developers’ plans.

In Q1 2026 the value of completed multi-unit building was about HUF 83 billion, still considered a moderate level. At constant price, it is particularly low. But it comes as no surprise as previous years were characterized by restrained project launches, and the large-scale projects that started last year are set to be completed only later.

Looking at the past four quarters, about two-third of multi-unit building projects entering construction phase concentrated in Budapest, so the capital’s share remains exceptionally high. About 69% of projects started in Central Hungary, 13% of the Activity-Start was linked to Eastern Hungary, while Western Hungary’s share was 18%.

Non-residential construction: after a weaker last year, this year started slowly

Within the subsector, two segments accounted for the majority of the Activity-Start: offices and industry. Offices performed rather poorly in previous years but recovered somewhat in Q1 2026 with their share within non-residential construction going up to 34% compared to 9% in the previous two years. Industrial properties and warehouses continued to account for the other major part despite the decline (their share dropped to 36% against 44-54% in the previous four years). In the first three months of this year, about 9-10% of started non-residential projects were related to wholesale and retail and education.

In 2026, besides the previously mentioned office, industrial and logistics projects, the largest non-residential projects also included Cholnoky Jenő Student Camp in Révfülöp, Rheinmetall RDX explosives factory in Várpalota, Mixvill shopping center in Debrecen, and Phase 1 of MyRA Park M3 shopping park. In 2025, non-residential construction was also characterized by weaker Activity-Start, but several high-value projects were launched such as the special operations barracks in Szolnok, BYD’s assembly hall, logistics warehouse, press plant and lightweight construction plant in Szeged.

In the past three years, non-residential projects reached completion at an exceptionally high value, between HUF 1,600 and 1,700 billion. During this period, Phase 1 of eMAG logistics centre, certain elements of BMW and Mercedes-Benz projects and several logistics projects were completed, including Robert Bosch logistics hall in Miskolc. Activity-Completion indicator may remain at a high level this year as well. The Hungaroring paddock building has already been handed over and several elements of BYD projects, Samsung Göd expansion, and several CATL buildings in Debrecen may also be completed.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

Written by Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members

The Croatian economy, including its construction sector, is threatened with serious damage this summer. For now, the pain has not been intense and the danger perceived only vaguely. This could change massively for the worse, though, both as to the actual injury and the perception of danger, by the middle of June and even as early as the end of May. Many factors are at work, but there is only one cause: the US-Israeli-Iran war.

Croatian tourism Summer 2026? – Split, Croatia. Photo by Tatjana Halapija

The cause

Ship traffic through the Strait of Hormuz, which links the Persian Gulf with the Arabian Sea and so with the rest of the world, has fallen 97%. This is twice as much as in any other oil crisis. This means that crude oil and liquified natural gas (LNG) are no longer being transported in anything resembling normal quantities. Nor are sulfur (an important chemical industry feedstock) or helium (used mostly in cooling, e.g., of MRI scanners), which are produced primarily as byproducts of oil and gas extraction and of which Gulf countries are major suppliers. The same holds true for fertilizer, ethanol, graphite, aluminum, iron and steel pellets and glycol, of which, again, Gulf countries manufacture a large portion of global production. (Pistachio nuts, too, but the effect on the world economy is likely to be less pronounced.) Worse, a significant amount of Gulf petroleum, gas and chemical production capacity has been destroyed or damaged (e.g., up to 17% of Qatar’s LNG production capacity) or will be if the war continues (shut downs often damage oil and gas wells and pipelines).

Although Asia is already suffering severely, with some countries mandating four-day work weeks to save energy, Europe and the United States have been spared the worst effects of these developments so far. That is about to change as supplies of oil, LNG and, even more important in the immediate and short terms, their refined products such as jet fuel and diesel become tight after ships in transit unload and private and national reserves are depleted.

Effects on Croatia: tourism, economy and construction

For Croatia, this will likely alter the sources, type, number and ability to spend of the tourists on which the country’s economy in large part depends .Tourists from distant countries will be deterred from flying to Croatia as the price of tickets and the number of canceled flights, already in the tens of thousands, rapidly rise because of enormous increases in jet fuel prices (doubling in Europe since February 28, 2026). Some in Europe may decide to drive instead, but they and tourists that normally drive to Croatia will find that fuel is expensive. Croatia’s languid approach to upgrading and extending its railways means that rail will for the most part not be a realistic alternative, and anyway rail ticket prices will rise, too, because of higher electricity and diesel prices. The upshot for Croatia is that many tourists may decide to completely alter their holiday plans and vacation nearer to home than Croatia, while those that do come will probably not stay as long and have less money to spend than in the past. This would significantly reduce the income Croatia derives from tourism. Croatia’s reputation for high costs, which higher agricultural product prices due to fertilizer shortages will worsen, will likely exacerbate the problem.

The implications for the Croatian construction industry are that hospitality-facility construction will likely fall in the near term, as owners, operators and investors wait to see just how bad and how long the economic effects of the war will be. The wait could be a long one, given that analysts forecast that these effects will last for at least eighteen months and perhaps considerably longer, particularly if the industrial and storage facilities of belligerents and their allies are targeted in a new outbreak of hostilities.

Damage to Croatia’s tourism sector will of course flow through to the country’s other economic sectors, given how important tourism is to Croatia’s economy. But these sectors will likely be hit directly as well. Further stagnation in countries to which Croatia exports non-tourism goods and services is to be expected because of the rise in the costs of energy and raw and intermediate materials, especially but not only plastics and others made from petroleum. This will put further strain on the Croatian economy.

Aggravating this will be a likely rise in the prices of at least some construction materials. Three examples among many are rebar and cement, both of which are energy intensive to produce, and concrete, which uses petrochemical-based additives. And of course transportation costs will rise. One, rather dim, bright spot is that weak economies in countries to which Croatian construction workers have emigrated could encourage them to return home, helping to keep construction costs down. But taken all in all, the growth rate in output of Croatia’s non-hospitality construction sectors is likely to decline and in some cases to go negative. Even government construction projects may be at risk, because payment of energy, agricultural and other subsidies will deplete the government’s cash reserves and reduced economic activity will diminish its tax take.

The future

The question now is not whether the US-Israeli-Iran war will have significant negative effects on construction in Croatia but rather just how bad those effects will be. In the unlikely event that shipments through the Strait of Hormuz resume before the end of May, the effects would be minimized, although to be clear that does not mean that they would be minimal. If the Strait remains blocked beyond the end of June, consequences for Croatia could be quite substantial, since, analysts believe, European reserves of oil, gas and other important products would by then be exhausted. This would cause prices to jump sharply and continually until recession or other events reduced demand to a level that accorded with supply. If hostilities cause additional significant degradation in Gulf region infrastructure, the situation for the construction sector of Croatia, and that of many other countries, could become quite severe.

Croatian construction market forecast is available in the EECFA Forecast Report Croatia. For sample report or orders, contact us.

With the latest governmental decision, the number of projects in designated rust belt action areas reached 91 in Hungary. 50 thousand dwellings1 are estimated to be built on these brownfield sites. The sole purpose of this post is to follow these projects and to see how they will or will not help the recovery of the new residential construction sub-market in Hungary.

Status on 1 May 2026. Before the election project starts slowed down.The newly elected government promises to double the number of built homes. — Completed: 4 018 dwellings Under construction: 12 622 dwellings Before construction: 27 180 dwellings

Brief background

Rust belt action areas (let me shorten them to rusty) are practically brownfield areas with special benefits. The owner of the site or the developer should initiate the process (with specific development plans) and there is a Committee to examine if the proposed site is entitled for the rusty status. Based on the opinion of the Committee, the final decision is made by the government. The decisions (about the exact sites) are announced in a decree and the special benefits coming with it are:

priority investment status, meaning e.g. faster permitting procedures2,

newly built homes can be sold at 5% VAT without limitation in time3,

By the current regulations, it means a min. 5% and a max. 27% price advantage over competitors developing on non-rusty area until 2030 (depending on when the permit was obtained) and a 27% price advantage from 2031 on.

Our focus

What we do is to turn the mentioned decree into information we need for forecasting. With the help of Eltinga Building Permit Monitor database and the iBuild project information database, actual projects are identified from the lot numbers specified in the decree. Among all the general project specifics, the number of dwellings (where it is known), are attached to these projects.

The map shows the stages of the housing projects that were given rusty status. Bluish dots are those before construction, neon yellow dots are those under construction and the dot disappears once the project is completed.

OK, it is very convenient to see projects on a map, but our focus is more on the chart under the map where the yellow is the number of homes under construction.

What we are curious about is if and when the right end of the yellow curve shows a strong upturn.

In other words, we are curious whether the regulation ignites a recovery or not. In the first years of the regulation, it was more common that the yellow line has increased because projects having started in the past were given the rusty status. (So they were just re-qualified, it did not mean new project starts.) In parallel, it was less common that projects start after they were given the status. Just two extreme examples for these: Unipark Buda had been under construction between 2019 and 2024 and it got the rusty status at the end of 2023, while Láng District was given the rusty status in 2021 and actual works commenced 5 years later. This has changed by now. So currently the yellow line increases if new projects starts. More precisely if the number of dwellings in newly started projects outnumbers the number of dwellings in completed projects.

The charts are updated quarterly.

Another way we like to look at it is a list. Here we do not separate the projects to phases (like on the map) and it gives a quick understanding on how each rusty project moves ahead from 1 February 2024 on.

Data sources

The data mostly come from Eltinga Building Permit Monitor (in Hungarian: Építési Engedély Figyelő). This is a very detailed database on before construction multi-unit housing projects in Budapest. It is aiming primarily at developers who would like to understand the competition. For further information on this, please turn to Mr Zoltán Sápi, Eltinga, sapiz@eltinga.hu. Besides, we use the iBuild project information database.

This is an estimation based on the median size of those rusty projects where the number of homes were announced ↩︎

Written by Dejan Krajinović, Beobuild Core d.o.o., EECFA Serbia

The construction of the Belgrade Metro stands as the largest single civil engineering project on the horizon and is one of the primary drivers of future economic growth in the coming years in Serbia. For decades, public transport in Belgrade relied solely on buses, trams, and the city railway (BG Voz). Consequently, the development of a comprehensive underground system is expected to have a transformative effect on commuting patterns and travel times. It is worth noting that Belgrade remains the largest city in Europe without a functional underground metro. While the project faced delays for many years, its commencement is now certain, with preparatory works already well underway.

Two massive Belgrade metro Tunnel Boring Machines ready to be shipped from China. Photo by Beogradski metro i voz

Strategic infrastructure: impact of the Belgrade metro project

The project represents a large-scale international collaboration between China and France. The Chinese construction giant PowerChina is tasked with tunnel boring, while the renowned French company Alstom will provide the rolling stock and system management. Recent reports from China confirm that massive, custom-made Tunnel Boring Machines (TBMs) for the Belgrade Metro are ready, having undergone factory testing, and are set to be shipped to Serbia this June. Two TBMs have been constructed for the first phase of the project, specifically for Line 1. These machines will start boring from opposite ends of the line to meet halfway – a strategy that will make the construction process highly efficient and significantly faster, though it demands exceptional coordination and project management.

Line 1 of the Belgrade Metro is divided into two phases: Phase 1 spans 15km and includes 15 stations, while Phase 2 is a planned extension of an additional 6km and 5 stations. The majority of Phase 1 will be underground, with 11km consisting of deep tunnels and 2km constructed using the cut-and-cover method; only 2.1km of the line will be above ground. The city’s topography presents a significant challenge as some stations will be remarkably deep and complex, reaching up to 40m below ground level. The system will utilize driverless, autonomous vehicles and digital signaling, ensuring maximum efficiency, safety, and frequency.

The original plan envisioned the construction of Line 2 (21km with 23 stations) beginning two years after Line 1, allowing the two projects to partially overlap. However, at this stage, it is uncertain whether parallel realization will proceed as planned. The pace of other phases will depend on the progress of Phase 1 of Line 1, but financial considerations will remain the major factor affecting the speed of future development.

Nevertheless, with the start of Line 1, Belgrade has embarked on a long and ambitious journey that will define the city’s construction landscape for years to come. Estimates suggest that Line 1 could cost between EUR 3.5 and EUR 3.8 billion,meaning the project’s scale will have a tremendous impact on civil engineering output from 2027 onwards. This is a key infrastructure development aimed at boosting growth against recessionary trends in the EU and an unstable global economic environment. On the other hand, the looming dangers of energy shocks, high inflation, and global financial instability remain significant risks—not only for this project but for Serbia’s entire construction industry and the economy as a whole.

Serbian construction market forecast is available in the EECFA Forecast Report Serbia. For sample report or orders, contact us.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Dr. Sebastian Sipos-Gug, EECFA’s Romanian analyst has looked at the trends that are worth monitoring in the residential market in Romania this year. Among them are the construction costs boomerang, the drop in wages and consumption, considerable interest in multi-family buildings, smaller homes and a greater dependence on mortgage loans.

What we saw in 2025

The construction market faced many challenges in the previous year, alongside the entire national economy. While there was a focus on civil engineering, especially when it comes to EU co-funded projects, the rest of the segments lagged behind.

In early 2025, the removal of fiscal facilities for construction employees led to the decline of their net incomes, and an increase in wage-related expenses for companies. Overall, the effect of this measure was an increase in construction costs.

Then came the multiple shocks of the liberalization of energy markets in July, and a VAT increase in August, which pushed inflation upwards significantly, with the CPI reaching 9.88% in September. In a snowball effect, this led to lower real wages and disposable income, which translated into a reduction in private consumption, and, ultimately, means lower demand for residential construction on the short and medium terms.

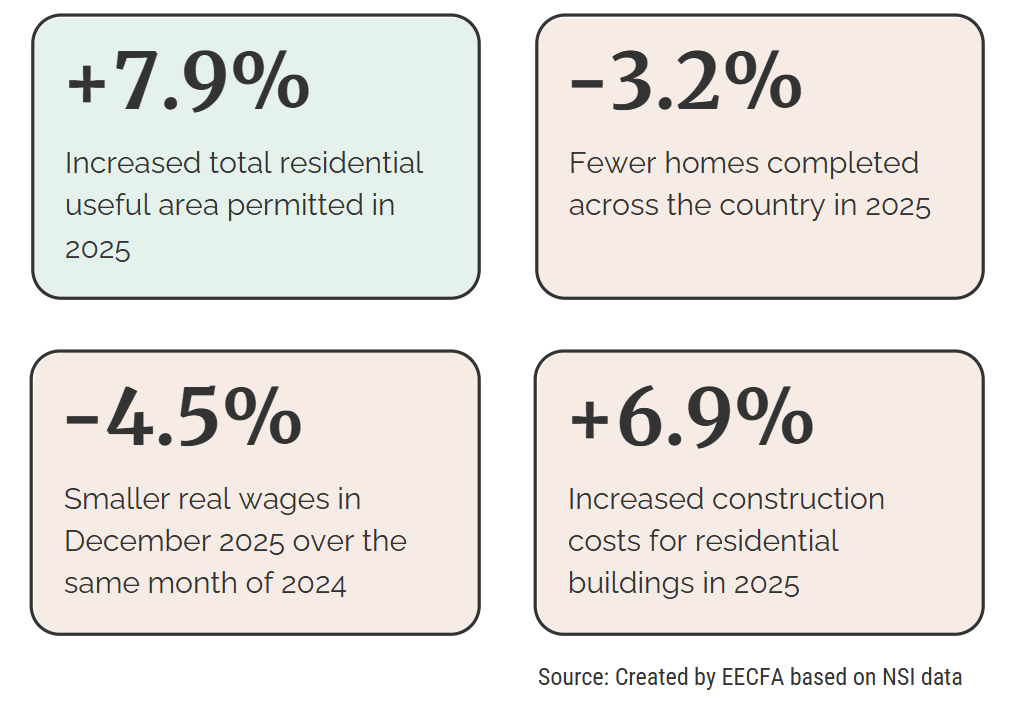

The optimism shown in the increased number of permits, and the useful building area in them, compared to 2024, is countered by the decline in the number of completed homes. Thus, while developers might be looking to the future, their actions in the present are lacking, also evidenced by a significant (-21%) annual decline in the value of started construction works in 2025 (source: EBI Construction Activity Report).

What to watch in 2026

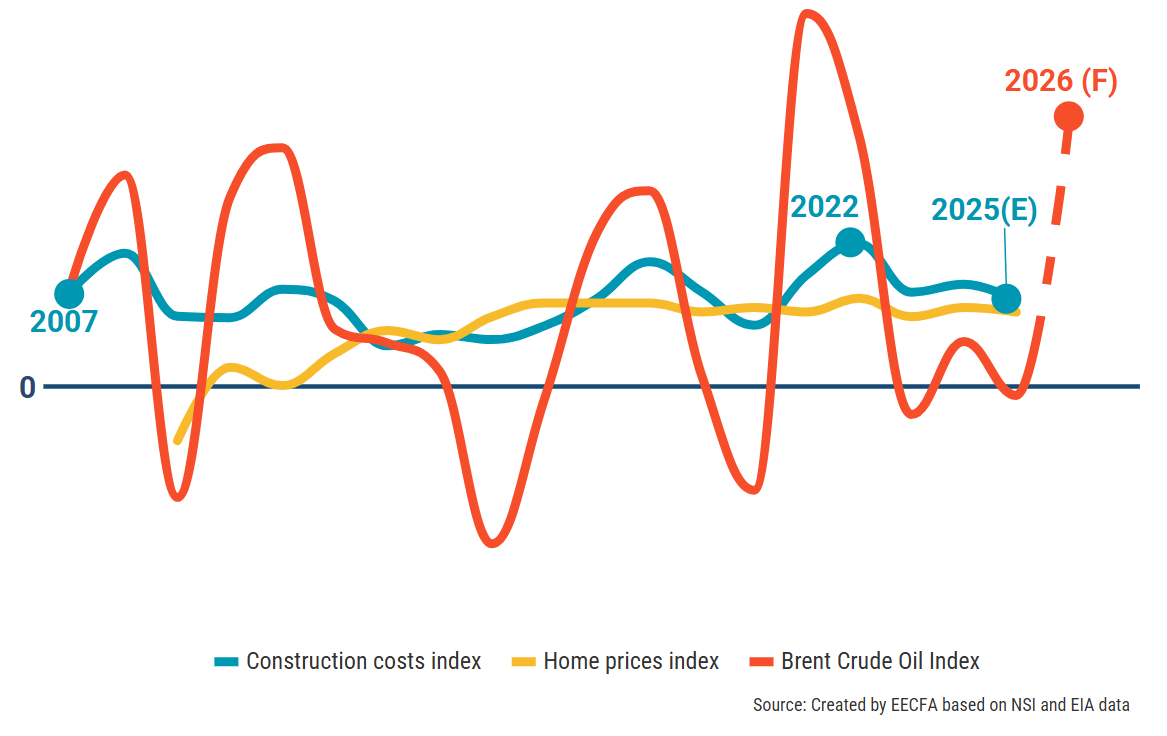

Construction costs boomerang. While previously the expectation was that construction costs would gradually decline in 2026, they proved quite resilient to changes in wages, and fuel and construction materials prices remained relatively stable in the past year. Thus, late 2025 forecasts placed construction costs on a small, descending trend.

The conflict in Iran and its repercussions on oil and gas prices might throw astray these predictions. As of March 2026, oil prices were approaching 2022 levels, and, if they are not reversed rapidly, might have a similar impact on world-wide inflation, energy prices and, eventually, construction costs. A reversal, however, seems rather unlikely at the moment as the damage to energy infrastructure could take years to undo.

To make matters worse, in the past few years home prices grew slower than construction costs, reducing potential profit margins for developers. Added to the decline in real wages, it remains quite unlikely that there will be room for prices to increase alongside construction costs, again similar to 2022, further eating into builders’ financial return potential.

Decline in wages and consumption. Wage growth for 2026 was already forecasted to remain low, underperforming inflation (source NFC – National Forecasting Commission Autumn 2025 Report). Add to that the further shocks now expected from increased energy costs (due to oil and gas prices rising considering the conflict in Iran) and food costs further rising due to increased fertilizer prices, the downwards pressure on real wages is likely to be worse than forecasted, with a slower recovery.

Real wage decline will make it harder to purchase and build new homes, with a negative impact on demand for residential construction. But it could provide a boost to renovation activity, especially when it comes to energy efficiency, as switching homes becomes harder.

High interest in multi-unit residential buildings. Looking at building permits trends for the past decade, single-home buildings have remained relatively stable, while the majority of growth was due to multi-unit buildings. Under price pressure, on the backdrop of restricted wage growth and a contractionary macro-economic outlook, it remains most likely that for the near future we’ll continue to see more interest in the latter. Another connected issue is that of internal mobility, with migration from rural to urban areas in search for education and economic opportunities, increasing demand for denser residential construction.

Smaller homes. While the mean area in permits remained relatively stable between 2017 and 2025, there is a historical precedent in economic downturns leading to smaller homes being built so as to increase accessibility. Since the economic outlook for the year seems to have worsened, this could be the case again in 2026.

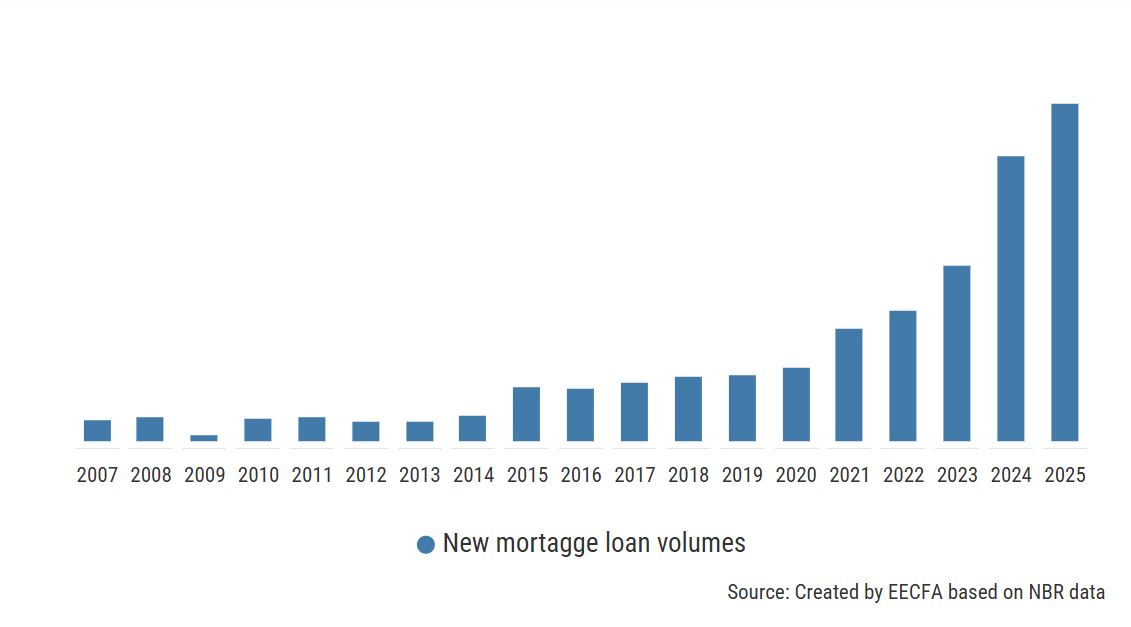

Increased reliance on mortgage loans. Despite the highest interest rates seen in a decade, the volume of new mortgage loans increased dramatically in 2024 and 2025. While some of this could be blamed on higher home prices, there remains a major portion that cannot be explained by price or transaction dynamics. Thus, it is quite likely that it reflects a reduced ability to buy homes without applying for a loan. This is also evidenced by the fact that the share of the population currently housed in a dwelling that was purchased with a mortgage loan grew steadily from a low of 0.5% in 2007, to 1.5% in 2024 (source: Eurostat). This could have been further boosted by the expected drop in interest rates as inflation seemed to be heading in the right direction. However, as of March 2026, this seems less likely, as the conflict in Iran would lead to another energy-led inflation event. Nonetheless, with real wages on the decline, mortgage loans will continue to be relied on for boosting home affordability.

Residential, non-residential and civil engineering forecasts up to 2027 can be found in the EECFA Romania Construction Forecast Report. Sample report and orders: https://eecfa.com/