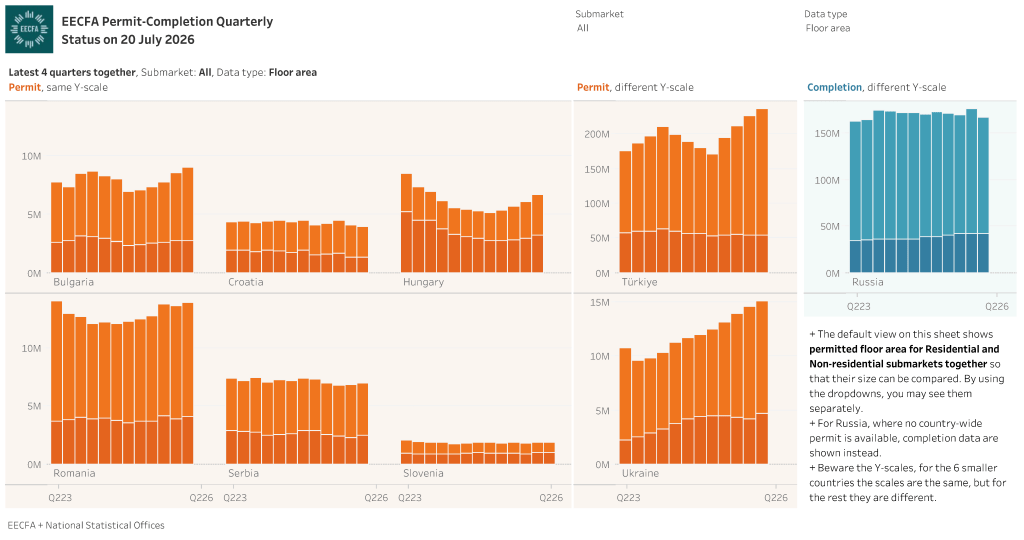

The viz was updated on 20 July 2026. → The first Q2 data is in. It is about Slovenia. The rest is arriving in the coming weeks. The text will be refreshed when all data are published.

Optimism in Croatia and Serbia prevails. Both countries experienced massive permit expansions between 2014 and 2022 and both have remained close to their peak ever since. Croatia has had around 4 million, while Serbia has had around 7 million permitted m2 for over four years. Slovenia remained below its 2022 high despite the positive correction in Q1 2026. Expansion continued in Bulgaria and the 9 million m2 was reached, a record in the last 15 years. Recovery in Romania and in Hungary is ongoing, led by residential projects.

You may use the dropdown in the viz for selecting either the residential or the non-residential submarket, or both.

In the full visualization, not only permit but completion data can be followed (where available).Just click on the Country-by-country sheet.

Figures in Türkiye are getting extremes, representing the highest optimism since 2017. Residential projects drive the growth, 1.25 million dwellings obtained construction permit in the last 4 quarters. (From Q2 2025 on, permits issued by authorities other than the municipalities are also published by TUIK. So the scope is bigger, the results show the full picture. Click through the below viz for understanding the size and the impact of this revision.) Q1 2026 has been the best quarter in Ukraine since the beginning of the war. This was the first quarter, however, when residential was not able to grow. After the strong year-end, 2026 started with shrinking completion in Russia.

This visual about the significance of the permit revision in Türkiye was compiled back in September 2025.

EECFA’s 2026 Summer construction forecast up to 2028 was released on 22 June. Sample report can be viewed at eecfa.com. To obtain the new reports, please contact us

Southeast European construction markets up to 2028

Bulgaria stepped into this year as the 21st member state of the eurozone in the middle of an evolving political turbulence that inevitably impacted the construction sector, most notably, projects that rely on public funding. Nevertheless, according to Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian member institute, Bulgaria’s total construction output is anticipated to increase by approximately 2% on average in the forecast period of 2026-2028. He also notes that “Last year Bulgaria’s construction sector excelled with a strong performance, largely thanks to the residential and non-residential submarkets which fared better than previously predicted. In 2026-2028, however, the country’s total construction output could see a heterogeneous performance.”

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s members for Croatia, point to funding from the EU’s Military Mobility Package (MMP) as a promising source of finance for a wide variety of Croatian construction projects. Transportation ones, both straightforwardly military and dual use, are obvious contenders, so the availability of MMP money should lift output in those civil engineering segments. MMP will likely boost some non-residential segments, too, since it can finance, e.g., factories and logistics centers (perhaps even flight schools?) that have a military or dual-use purpose. This will help sustain total construction output despite rapidly declining levels of finance under the EU’s post-2022-earthquake rebuilding programs and RRF. In non-residential generally, while some developments will affect all segments, specific factors will ensure that output growth varies greatly from segment to segment. The picture for energy construction is also confused, with solid, well-known technologies competing with much-hyped, as-yet-unproven, “hi-tech” alternatives. Residential is buffeted by the conflicting influences of rising prices, declining GDP growth and interventions by the central bank and the government.

Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild, notes that Romania’s construction market is still in a tight spot. “Growth potential is limited with global and national factors conspiring against it. Recent economic forecasts are more pessimistic; 2026 might see a stagnant GDP, declining real wages and the highest inflation in the EU. This is coupled with the looming specter of national deficit causing high taxation and austerity measures: lower public spending, and wage and hiring freezes for public employees. Not to mention that construction costs, which started evening out in 2025 after the 2022 shock, are now again on the rise due to climbing energy prices and labor costs. The saving grace of construction is the EU programs funding infrastructure projects. Yet, with the NRRP running out in mid-2026, and other programs having an inconsistent performance, the boost they can provide is limited. Adding to all this is a political crisis that could lead to a government change at a critical moment (the end of NRRP absorption, projects phased into other funding sources). But the silver lining: most of these issues should be transitory. By 2028 Romania’s construction might return to growth on the back of improved economic indicators, inflation levels within the target range, a more efficient energy sector, and hopefully, a more stable political situation.”

“Serbia’s overall construction output is still consolidating in 2026 led by the correction in civil engineering, while buildings continue to grow in this forecast” – according to Dejan Krajinović, EECFA’s Serbian researcher at Beobuild. He adds that the performance in the residential submarket remains stable and is predicted to continue to grow with moderate growth rates. Non-residential, on the other hand, is booming, driven by massive investments related to the EXPO 2027, with another year of double-digit growth expected in 2026. Main segments benefiting from ongoing developments are office, commercial and hotel, but health-related construction is also breaking records in 2026. The consolidation in civil engineering is anticipated to end in 2027, with new growth on the horizon in 2028 and onwards. The large-scale infrastructure projects in the pipeline should launch a next big growth cycle in overall outputs. However, the war in the Middle East is already pushing construction costs up and the economic uncertainty and fragmentation are still risks that continue to linger in the coming period.”

“Slovenia’s construction sector’s output was holding steady at just under €6bn in 2024 and 2025 but is set to edge higher in the forecast period, supported mainly by public spending” – says Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia. “Growth is increasingly uneven: residential construction remains constrained by limited supply and rising costs despite strong demand, while private non-residential segments such as offices, retail and industry face cautious investors and only modest expansion. By contrast, publicly financed segments, notably education, health and civil engineering renovation, are providing stability, with infrastructure upgrades, railway investment and energy-transition projects sustaining activity. Transport and utility constructions are shifting from large expansions to maintenance and modernisation, and investment in electricity networks and pipelines is set to rise further due to the energy transition. Overall, the sector is moving into a more stable but slower phase where public policy and infrastructure spending play a decisive role in keeping output on track – as long as public financing remains available.”

Eastern European construction markets up to 2028

According to Andrey Vakulenko at Macon, EECFA’s Russian research institute, the downward trend in Russia’s construction market, which began in 2025, is likely to continue and intensify in 2026–2027. The main reason behind is the combination of a decelerating economy and a prolonged period of high interest rates, which negatively impacts demand, limits the availability of financing and restrains investment activity. Residential construction is experiencing the strongest pressure as the market struggles to find a new balance amid reduced mortgage availability, declining demand and decrease in new construction. Most non-residential segments may also show negative dynamics in the coming years impacted by the slowdown in consumption volumes and business activity, weak household income growth and changes in the direction and scope of government funding in certain segments. Civil engineering will likely stay the most resilient subsector due to the implementation of major transport and energy projects. The planned acceleration of infrastructure construction, the expected growth in the residential submarket and the easing of monetary policy are the conditions for the construction market to return to a growth trajectory in 2028.

“In Türkiye, state involvement in housing development has grown in recent years” – say Prof. Ali Türel and Prof. Leyla Alkan Gökler, EECFA’s Turkish researchers. “Policies to curb inflation have depressed households’ disposable income, creating a serious housing affordability issue for both ownership and renting as home prices and rents have spiked. As moderate-to lower-income households have found it increasingly difficult to accumulate sufficient equity for home purchases, the government has intervened. It launched a large number of residential projects for dwellings that can be bought on affordable terms by households not owning a house in Türkiye. Dwellings will be built by the Housing Development Administration (HDA), the key state actor in housing production in Türkiye. Since HDA has also been involved in rebuilding the about 550,000 dwellings damaged in the February 2023 quake, the share of housing built by the public sector has greatly risen in recent years, while the share of the private sector has been declining from its former share of about 90%. Our latest forecast indicates that total construction output in Türkiye may reach nearly 8 trillion TL (nearly EUR 180 billion) in 2028, at 2025 prices.”

“Ukraine’s construction market exhibited high resilience in 2025 despite the ongoing war and challenging security conditions. While it is recovering and it nominally returned to pre-war levels last year, it was still 40% below the 2021 output at comparable prices.” – notes Professor Sergii Zapototskyi at Uvecon, EECFA Ukraine. “Key growth drivers were commercial, industrial, warehouse, and logistics developments, an uptick in residential construction in relatively safe regions, and large-scale projects aimed to restore public and transport infrastructure. In the coming years, the construction market is expected to continue to grow, supported by post-war reconstruction needs, government housing support programs, and an increase in international funding for Ukraine’s recovery. The greatest growth potential will remain in residential, commercial, as well as industrial and warehousing construction. At the same time, the future performance of the market will largely depend on the security situation, the availability of investment resources, the ability to address labour shortages, and the effectiveness of government reconstruction policies.”

With the latest governmental decision, the number of projects in designated rust belt action areas reached 91 in Hungary. 50 thousand dwellings1 are estimated to be built on these brownfield sites. The sole purpose of this post is to follow these projects and to see how they will or will not help the recovery of the new residential construction sub-market in Hungary.

Status on 1 May 2026. Before the election project starts slowed down.The newly elected government promises to double the number of built homes. — Completed: 4 018 dwellings Under construction: 12 622 dwellings Before construction: 27 180 dwellings

Brief background

Rust belt action areas (let me shorten them to rusty) are practically brownfield areas with special benefits. The owner of the site or the developer should initiate the process (with specific development plans) and there is a Committee to examine if the proposed site is entitled for the rusty status. Based on the opinion of the Committee, the final decision is made by the government. The decisions (about the exact sites) are announced in a decree and the special benefits coming with it are:

priority investment status, meaning e.g. faster permitting procedures2,

newly built homes can be sold at 5% VAT without limitation in time3,

By the current regulations, it means a min. 5% and a max. 27% price advantage over competitors developing on non-rusty area until 2030 (depending on when the permit was obtained) and a 27% price advantage from 2031 on.

Our focus

What we do is to turn the mentioned decree into information we need for forecasting. With the help of Eltinga Building Permit Monitor database and the iBuild project information database, actual projects are identified from the lot numbers specified in the decree. Among all the general project specifics, the number of dwellings (where it is known), are attached to these projects.

The map shows the stages of the housing projects that were given rusty status. Bluish dots are those before construction, neon yellow dots are those under construction and the dot disappears once the project is completed.

OK, it is very convenient to see projects on a map, but our focus is more on the chart under the map where the yellow is the number of homes under construction.

What we are curious about is if and when the right end of the yellow curve shows a strong upturn.

In other words, we are curious whether the regulation ignites a recovery or not. In the first years of the regulation, it was more common that the yellow line has increased because projects having started in the past were given the rusty status. (So they were just re-qualified, it did not mean new project starts.) In parallel, it was less common that projects start after they were given the status. Just two extreme examples for these: Unipark Buda had been under construction between 2019 and 2024 and it got the rusty status at the end of 2023, while Láng District was given the rusty status in 2021 and actual works commenced 5 years later. This has changed by now. So currently the yellow line increases if new projects starts. More precisely if the number of dwellings in newly started projects outnumbers the number of dwellings in completed projects.

The charts are updated quarterly.

Another way we like to look at it is a list. Here we do not separate the projects to phases (like on the map) and it gives a quick understanding on how each rusty project moves ahead from 1 February 2024 on.

Data sources

The data mostly come from Eltinga Building Permit Monitor (in Hungarian: Építési Engedély Figyelő). This is a very detailed database on before construction multi-unit housing projects in Budapest. It is aiming primarily at developers who would like to understand the competition. For further information on this, please turn to Mr Zoltán Sápi, Eltinga, sapiz@eltinga.hu. Besides, we use the iBuild project information database.

This is an estimation based on the median size of those rusty projects where the number of homes were announced ↩︎

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Dr. Sebastian Sipos-Gug, EECFA’s Romanian analyst has looked at the trends that are worth monitoring in the residential market in Romania this year. Among them are the construction costs boomerang, the drop in wages and consumption, considerable interest in multi-family buildings, smaller homes and a greater dependence on mortgage loans.

What we saw in 2025

The construction market faced many challenges in the previous year, alongside the entire national economy. While there was a focus on civil engineering, especially when it comes to EU co-funded projects, the rest of the segments lagged behind.

In early 2025, the removal of fiscal facilities for construction employees led to the decline of their net incomes, and an increase in wage-related expenses for companies. Overall, the effect of this measure was an increase in construction costs.

Then came the multiple shocks of the liberalization of energy markets in July, and a VAT increase in August, which pushed inflation upwards significantly, with the CPI reaching 9.88% in September. In a snowball effect, this led to lower real wages and disposable income, which translated into a reduction in private consumption, and, ultimately, means lower demand for residential construction on the short and medium terms.

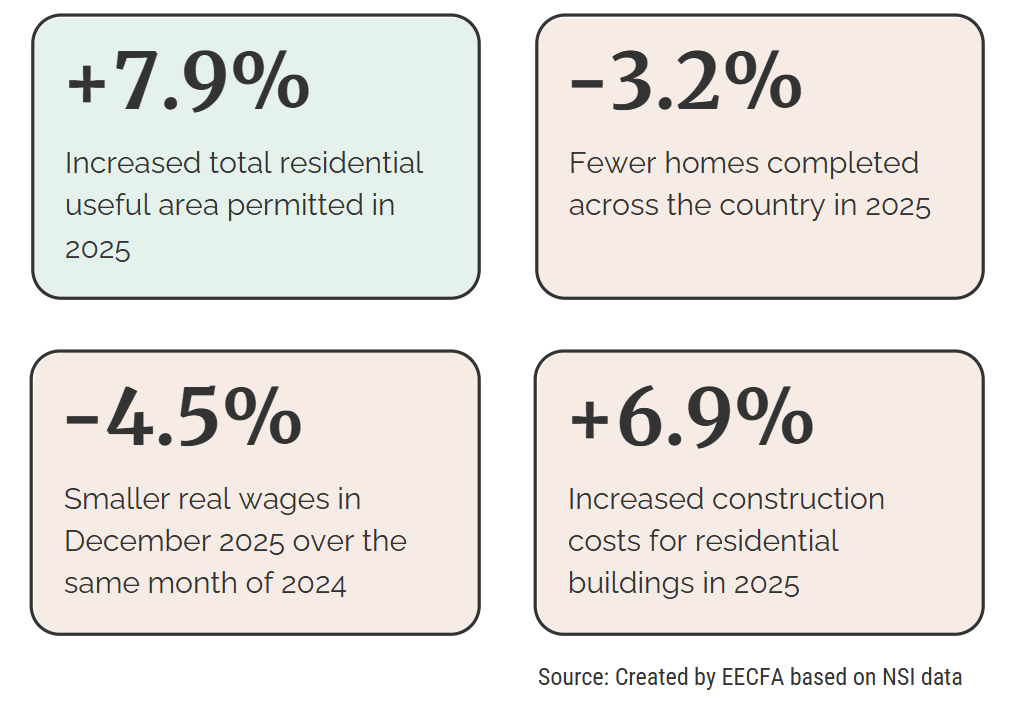

The optimism shown in the increased number of permits, and the useful building area in them, compared to 2024, is countered by the decline in the number of completed homes. Thus, while developers might be looking to the future, their actions in the present are lacking, also evidenced by a significant (-21%) annual decline in the value of started construction works in 2025 (source: EBI Construction Activity Report).

What to watch in 2026

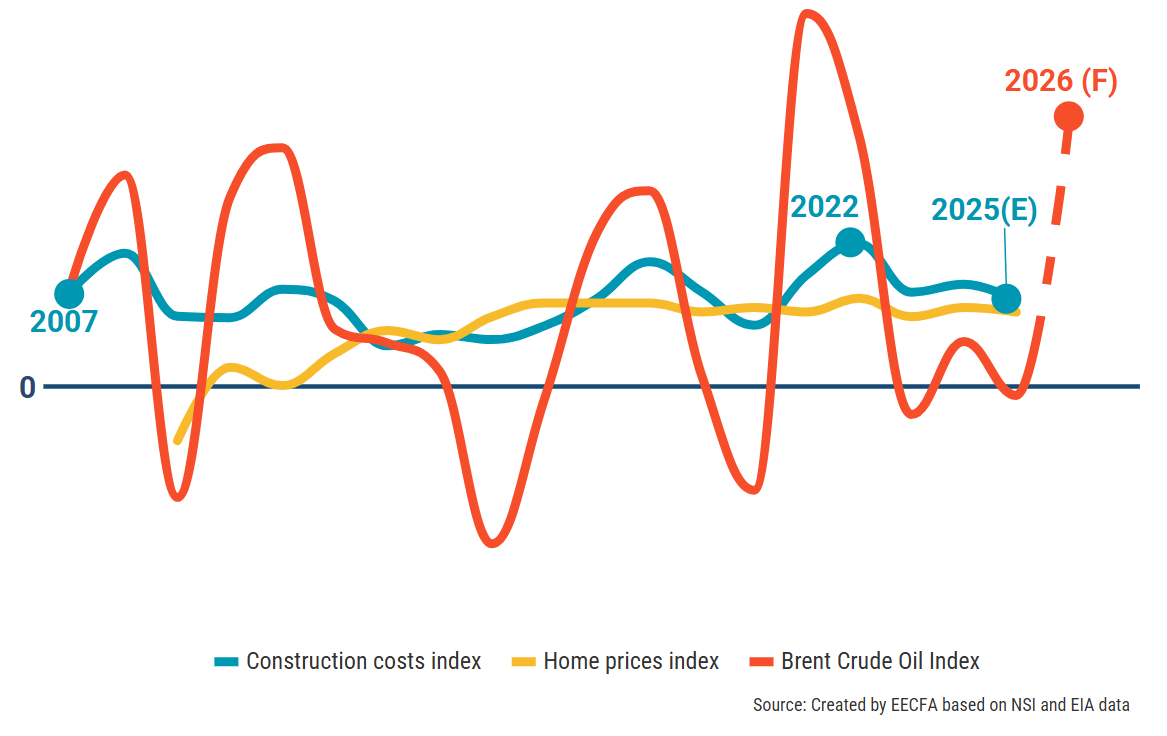

Construction costs boomerang. While previously the expectation was that construction costs would gradually decline in 2026, they proved quite resilient to changes in wages, and fuel and construction materials prices remained relatively stable in the past year. Thus, late 2025 forecasts placed construction costs on a small, descending trend.

The conflict in Iran and its repercussions on oil and gas prices might throw astray these predictions. As of March 2026, oil prices were approaching 2022 levels, and, if they are not reversed rapidly, might have a similar impact on world-wide inflation, energy prices and, eventually, construction costs. A reversal, however, seems rather unlikely at the moment as the damage to energy infrastructure could take years to undo.

To make matters worse, in the past few years home prices grew slower than construction costs, reducing potential profit margins for developers. Added to the decline in real wages, it remains quite unlikely that there will be room for prices to increase alongside construction costs, again similar to 2022, further eating into builders’ financial return potential.

Decline in wages and consumption. Wage growth for 2026 was already forecasted to remain low, underperforming inflation (source NFC – National Forecasting Commission Autumn 2025 Report). Add to that the further shocks now expected from increased energy costs (due to oil and gas prices rising considering the conflict in Iran) and food costs further rising due to increased fertilizer prices, the downwards pressure on real wages is likely to be worse than forecasted, with a slower recovery.

Real wage decline will make it harder to purchase and build new homes, with a negative impact on demand for residential construction. But it could provide a boost to renovation activity, especially when it comes to energy efficiency, as switching homes becomes harder.

High interest in multi-unit residential buildings. Looking at building permits trends for the past decade, single-home buildings have remained relatively stable, while the majority of growth was due to multi-unit buildings. Under price pressure, on the backdrop of restricted wage growth and a contractionary macro-economic outlook, it remains most likely that for the near future we’ll continue to see more interest in the latter. Another connected issue is that of internal mobility, with migration from rural to urban areas in search for education and economic opportunities, increasing demand for denser residential construction.

Smaller homes. While the mean area in permits remained relatively stable between 2017 and 2025, there is a historical precedent in economic downturns leading to smaller homes being built so as to increase accessibility. Since the economic outlook for the year seems to have worsened, this could be the case again in 2026.

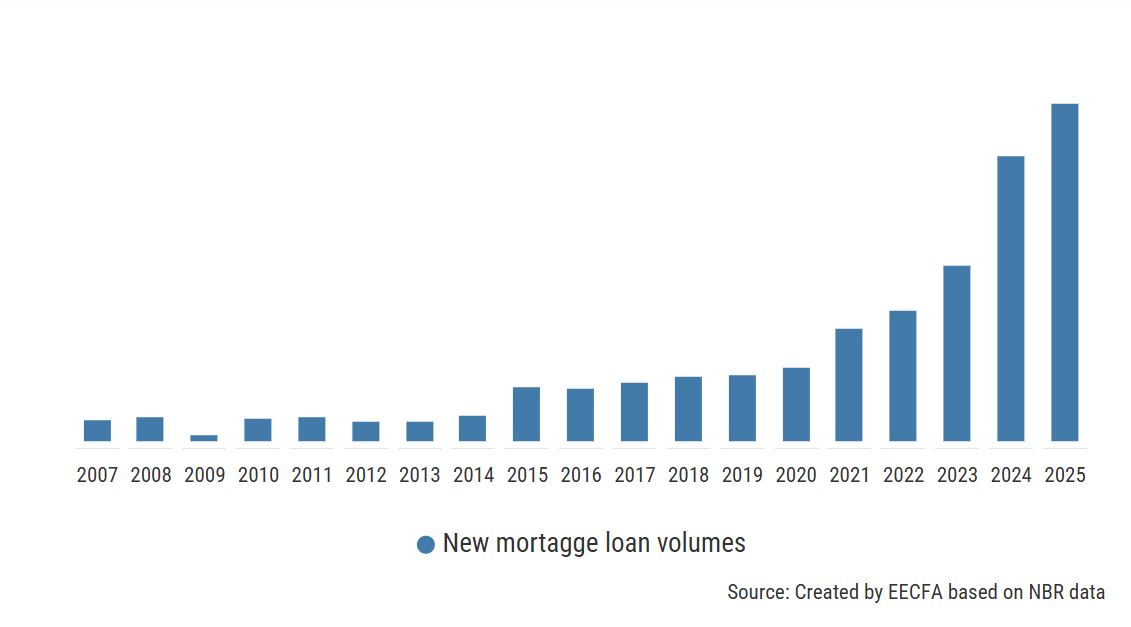

Increased reliance on mortgage loans. Despite the highest interest rates seen in a decade, the volume of new mortgage loans increased dramatically in 2024 and 2025. While some of this could be blamed on higher home prices, there remains a major portion that cannot be explained by price or transaction dynamics. Thus, it is quite likely that it reflects a reduced ability to buy homes without applying for a loan. This is also evidenced by the fact that the share of the population currently housed in a dwelling that was purchased with a mortgage loan grew steadily from a low of 0.5% in 2007, to 1.5% in 2024 (source: Eurostat). This could have been further boosted by the expected drop in interest rates as inflation seemed to be heading in the right direction. However, as of March 2026, this seems less likely, as the conflict in Iran would lead to another energy-led inflation event. Nonetheless, with real wages on the decline, mortgage loans will continue to be relied on for boosting home affordability.

Residential, non-residential and civil engineering forecasts up to 2027 can be found in the EECFA Romania Construction Forecast Report. Sample report and orders: https://eecfa.com/

Written by Dr Aleš Pustovrh – Bogatin, EECFA Slovenia

Slovenia’s housing market is in a curious state. Prices for both new and existing homes keep rising, yet the country still lacks a reliable measure of how far supply trails demand. Official data show steady appreciation across all major cities—Ljubljana most of all—while construction remains hampered by slow permitting, high input costs and a fragmented building industry. Politicians promise a surge in public and affordable housing but estimates of the true shortfall—whether based on household formation, demographics or unmet rental demand—are patchy and inconsistent. The average price per square metre has jumped by roughly 50% since 2021, but the structural imbalance behind this surge is harder to pin down, leaving policymakers to grapple with a problem they can only describe vaguely.

Ljubljana, Slovenia. Photo by Alexander Nadrilyanski on pexels.com

With a general election looming in March 2026, the absence of clear data creates fertile ground for confusion and political spin. The ruling coalition boasts of raising annual public‑housing investment to €100mn, pledging €1bn over the next decade. The public housing fund plans around 2,000 new units in the coming years, with perhaps 1,000 more from other public bodies. Private developers, especially in Ljubljana, are building briskly, too. Given that Slovenia completes about 5,000 homes a year, these additions ought to shift the market—at least in theory.

But the scale of need remains uncertain. In 2021 Slovenia counted 864,300 dwellings for 859,782 households—roughly one per household. Prices, though rising fast, remain below those in some neighbouring countries. The median price of used homes was €3,070 per square metre (nearly €5,000 in Ljubljana), while the average gross monthly wage was €2,500—yielding a price‑to‑income ratio lower than in many EU states. Mortgage credit is widely available and relatively cheap, with interest rates well below 4%. Outstanding housing loans rose from €8.5bn to more than €9bn in 2025, suggesting that many households are managing their residential construction investments without state support.

One of the outgoing government’s flagship measures—a clampdown on short‑term rentals—was meant to push more homes into the long‑term market. It may instead swell the ranks of empty properties: around 19% of dwellings already stand vacant. A straightforward remedy, a property tax to nudge owners to rent out unused homes, was avoided for fear of angering voters in a country where 75% of households own their homes.

The lack of solid data allows politicians to champion measures unlikely to achieve their stated aims, while sidestepping those that might work but would prove unpopular. Election season is rarely conducive to sober policymaking, but the next government will need better data—and the courage to act on it—if it hopes to make any meaningful dent in Slovenia’s housing woes.

More on Slovenia’s housing market and housing forecast up to 2027 can be found in the EECFA Slovenia Construction Forecast Report. Sample report and orders: https://eecfa.com/

EECFA released its 2025 Winter construction forecast on 12 December. Check out a sample report and place your order on eecfa.com. For discount, please contact us.

Southeast European construction markets

“Bulgaria’s total construction output is forecasted to increase by 3% on average for 2026-2027” – says Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian research institute. He adds that this is to follow estimates for a similar performance of almost 3% in 2025. The sectoral background, however, shows, a nuanced picture – cooling of residential construction, positive news from non-residential and a robust performance of civil engineering. The latter will benefit from investments which will be backed by the absorption of EU funds through the Recovery and Resilience Plan (RRP) and classical operational programmes, both with implementation deadlines in 2026 and 2027. At the same time, Bulgaria’s economy is to expand by 2.4% on average in 2026-2027 – a period continuously shaped also by the Euro adoption on 1 January 2026.

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members, think that declining dwelling sales in Croatia have, paradoxically, failed to stop the growth in the value of Croatian residential output, because increases in the price per square meter of those dwellings that do get sold have more than compensated for the lower number of square meters bought. “But how long this can continue is unclear” – they add. “The policies that the Croatian government is implementing in order to ease the country’s housing crisis are confusing the residential picture still more, since a number of those policies have contradictory effects on output. As to non-residential building construction, output growth during the period covered by the current forecast will depend greatly on the sector, with some likely to continue to benefit from catch-up growth and EU support for a bit longer and others moving toward a steady state or even a decline. In civil engineering, EU funds continue to play the dominant role in financing construction of all sorts. Sports facility construction is experiencing a boom, but given the speed with which such projects are completed, the effect on output will be relatively brief. Renewable energy construction should be growing rapidly, but regulators’ hostility toward the sector are holding it back.”

“Romania’s economy is entering a challenging period as the recently implemented measures to reduce the national account deficit begin to take effect” – reports Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild. “While most forecasters do not anticipate a recession, economic growth is expected to remain subdued over the next two years. Inflation is the highest in the EU, boosted in 2025 by increases in sales taxes. As a result, consumer prices are rising at a pace that is forecasted to outstrip wage growth, leading to a decline in real incomes in both 2025 and 2026. Government spending is also facing cuts, thus both private and public consumption are predicted to decline, with a chilling effect on most construction activity types. There is also the challenge of the massive level of public investment required by civil engineering projects that have started since 2023, which will be difficult to sustain under the austerity and the mounting pressure of losing even more EU funding. On the brighter side, both the economy at large and the labour market are expected to be quite resilient. By 2027, assuming the deficit reaches manageable levels, the effects of contractionary policies should fade out, inflation could ease, and interest rates could come down. This means that demand for construction would rebound and with it, construction activity.”

Dejan Krajinović, EECFA’s Serbian researcher (Beobuild) says that “Serbia’s overall construction output sank into a negative territory in 2025, primarily owing to the weaker performance in civil engineering. This year recorded growth in building construction, but the substantial consolidation in civil engineering dragged totals in red. The completion of major road, railway and energy projects contributed mostly, but delayed construction starts played a role as well. Residential construction is stable and is on historical levels, while non-residential construction is booming led by the hosting of the EXPO 2027 in Belgrade. Investments into commercial, hotel and office buildings are all spurred by the event, with the purposely built EXPO 2027 complex consisting of numerous venues being the single largest investment in non-residential. Improving financial conditions and sustained demand still support relatively high construction activity, but a lot of global political and economic uncertainties are dimming future prospects.”

Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia, says that Slovenia’s construction sector is holding steady at EUR 6bn, though growth has cooled. Residential buildings remain the anchor, with output expected to show only a slight dip in 2025, helped by strong employment, rising wages and cheaper mortgages. Property transactions rebounded in early 2025, reversing last year’s slump, while prices continue to climb amid land shortages and slow permitting. Public housing programmes are ambitious, but private developers are concentrating on Ljubljana and coastal towns. Non-residential construction is mixed: offices are recovering slowly, retail stays subdued, but industrial and warehousing thrive on export demand and automation while health and education remain at very high levels. Civil engineering and public works lean on EU-backed projects and are anticipated to reach historically high levels by 2026.

Eastern European construction markets

Andrey Vakulenko at Macon, EECFA’s Russian research institute notes that “the high key rate and the overall economic slowdown are constraining the Russian construction industry with negative trends expected for the current year and over the next two years. An easing of monetary policy, which has already begun, could help normalize the situation, but a positive effect is not expected until 2027. The main drag on construction output will likely be the residential subsector where high rates and revised government demand support principles are reducing activity among both buyers and developers. Negative trends will also likely persist in most non-residential segments due to declining growth rates of budget financing, a general decrease in business activity and a slowdown in consumption. The overall descending dynamics in the construction market may somewhat be mitigated by stable growth in civil engineering driven by export projects in energy and transport, but this growth is not predicted to be enough to keep the construction market in a positive zone”.

Prof. Ali Türel, EECFA’s Turkish researcher, reports that “the major effect of inflation-curb policies in Türkiye is the decline in disposable income and in the purchasing power of wage earners and pensioners. The moderate to lower-income population is unlikely to save enough equity for buying a home when rents have also become unaffordable for many. Ironically, housing sales have been increasing at a much higher rate than the growth of households. This can be attributed to the typical trend in Türkiye, where, during inflation, people expect a higher real return on their financial assets from real estate investments compared to alternative investment options. The reconstruction of earthquake-damaged buildings and infrastructure also contributed to the high rate of growth in building starts and completions from Q2 2025 onward, leading to the highest rates of change in the construction sector’s contribution to GDP compared to other sectors. Our latest forecast indicates that total construction output in Türkiye may reach 6.4 trillion TL in 2027 (EUR 180 billion), all at 2024 prices.”

According to Prof. Sergii Zapototskyi of Uvecon, EECFA Ukraine, despite the war and high risks, Ukraine’s construction industry remains one of the key drivers of economic recovery in 2025. The RDNA4 (the latest Rapid Damage and Needs Assessment Report) estimates Ukraine’s reconstruction needs for the next decade to be USD 486-524 billion, creating long-term demand for residential, non-residential and civil engineering construction works. Major challenges persist, including the uncertainty regarding the duration of the war, especially in frontline regions, labour shortages, bureaucratic barriers in the urban planning legislation, and logistical constraints due to the relocation of production facilities, and often, shortages in building materials. At the same time, the industry is demonstrating resilience: developers are diversifying supply chains, stabilizing procurement schedules, and increasing activity in the Central and Western regions. Demand for housing, intensive infrastructure restoration, and international investment from the EBRD, EIB, and other partners continue to support positive dynamics. The sector’s development prospects for 2026-2027 will largely depend on the security situation and the effectiveness of state recovery programs.

Written by Sergii Zapototskyi – UVECON, EECFA Ukraine

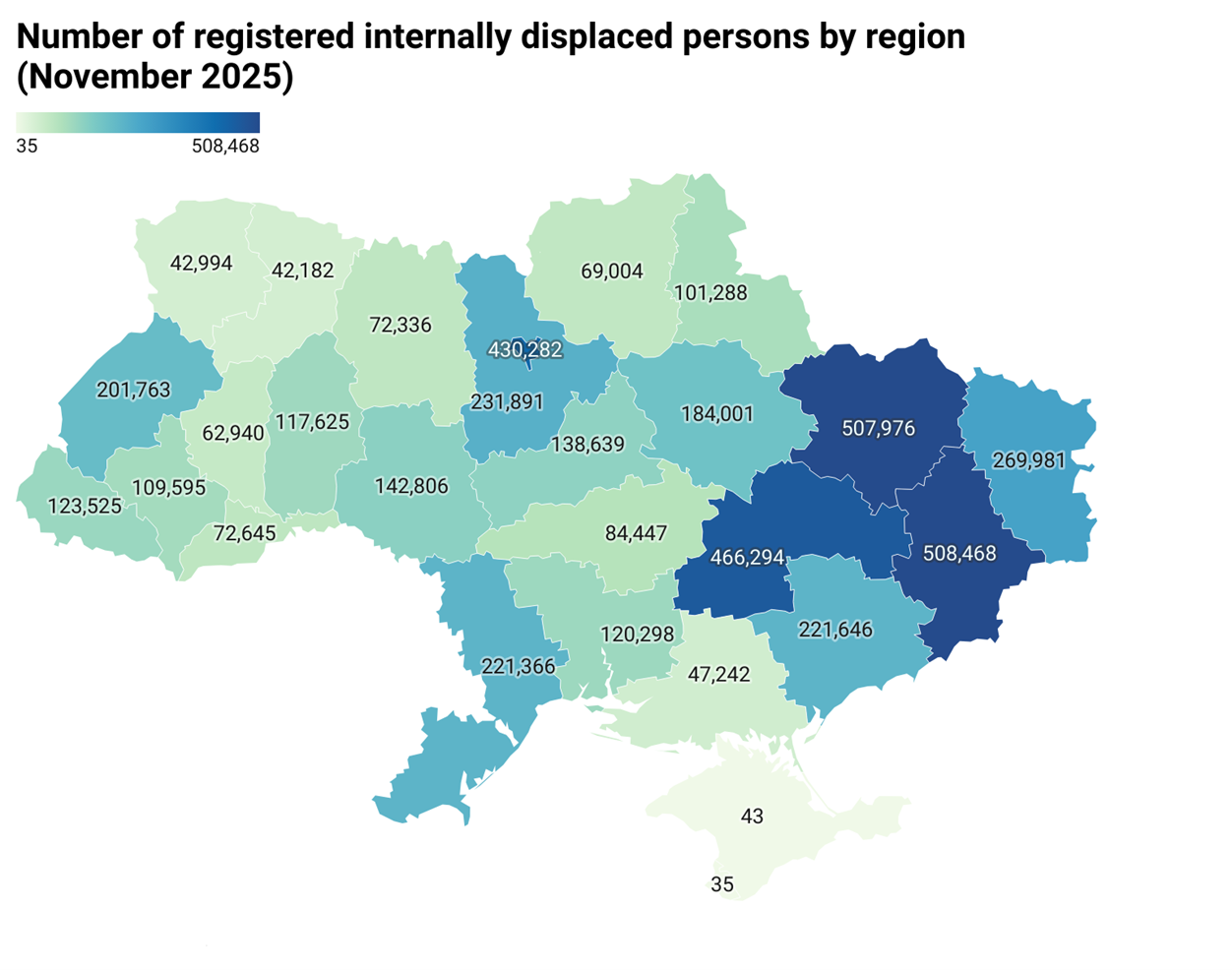

The full-scale invasion of Russia caused a deep humanitarian crisis and exacerbated socio-economic disparities in Ukraine. One of the key challenges is to provide homes for internally displaced persons (IDPs). The mass movement of the population created a shortage of affordable and temporary housing as the infrastructure was not ready for such a load. The government is already working on a new housing policy, which might also help resolve the issue of housing for IDPs.

As of 1 November, this year, 4,588,045 internally displaced persons were officially registered in Ukraine, including 838,436 children under the age of 18 [1]. Most IDPS are in Kharkiv region (508 thousand or 11%), followed by Dnipropetrovsk region (467 thousand or 10%), the city of Kyiv (430 thousand or 9.4%) and Kyiv region (232 thousand or 5%). [3]. IDPs in these regions total about 1.6 million people [1]. As per the result of the 16th round of the survey conducted by The International Organization for Migration (IOM, UN Migration), as of April 2024, about 2.7 million internally displaced people were from frontline areas.

Housing damages, needs and solutions

In total, more than 1.3 million Ukrainian households lost their homes because of the war, including not only IDPs, but also residents of settlements that suffered extensive destruction. The World Bank estimates total housing needs in Ukraine between 2025 and 2035 to be USD 86 billion, mostly to finance repair and reconstruction works of the housing stock (estimated at USD 75.5 billion including the cost of clearing rubble at USD 5.7 billion). USD 404.6 million should go to acute housing needs and funding has also been identified for organizational measures (USD 37.5 million) and regulatory and technical processes, including the development of strategies (USD 12.5 million) to coordinate and implement reconstruction programs [4].

Citizens have already submitted over 850,000 reports of housing damage through the Diia app (the national public-services portal) totalling over 60 million sqm of losses. For comparison, in the pre-war period, an average of 9-10 million sqm of homes were completed in Ukraine each year, demonstrating the scale of challenge and need for multi-level solutions in housing policy. Preferential lending programs are unable to solve this situation and cover the housing needs. The ‘jeOselia’ program provided loans worth over UAH 28 billion, but 52% of this went to military personnel, while IDPs received only 566 pieces of loans. In 2024, within the framework of this 3% mortgage program, only 500 families were provided with housing. The situation is even more critical in the rental market as the state program for subsidizing rental housing has shown low efficiency. The majority of IDPs (90-95%) rent homes unofficially, making them vulnerable to unreliable living conditions and unjustified rental charge increases or evictions.

Modular settlements are a key temporary housing for IDPs, although living conditions here cannot be considered fully comfortable. Initially, they were meant to be short-term but gradually became long-term housing for many families due to their limited finances. Today, besides the psychological difficulties and discomfort of residents, operating such facilities is also a major challenge. The maintenance of modular settlements, including payment for utilities, repairs and security, falls entirely on local budgets, an additional financial burden for communities which often do not have enough resources to sustainably finance these.

As the problem of providing housing for IDPs is systemic in nature and cannot be solved solely through financial instruments, a comprehensive review of state housing policy has become necessary, particularly the development of an affordable rental housing segment, social programs, and long-term support mechanisms for both IDPs and vulnerable categories of the population in general.

The Ukrainian Parliament is already working on several key legislative initiatives. The central one is draft law No. 12377 ‘On the Basic Principles of Housing Policy’ to replace the current Housing Code from 1983 which does not contain basic concepts for modern housing policy such as social rental housing or housing stock of communal ownership. Draft law No. 4080 is also important on the inventory of the housing stock. In parallel with drafting these laws, necessary by-laws are being prepared to regulate the practical mechanisms for implementing housing policy (creation and maintenance of housing queues, criteria for selecting recipients of state support, and the procedure of providing various forms of housing assistance). In addition, the government’s plans until 2027 include allocating EUR 650 million to the eRecovery Program, EUR 450 million to support IDPs, military personnel and the families of the deceased, creating a social housing fund and introducing a unified state online system for the long-term strategy of social integration and support for vulnerable categories of the population. All this might help resolve housing for IDPs.

Sources:

Internally Displaced Persons. State Enterprise “Information and Computing Center of the Ministry of Social Policy, Family and Unity of Ukraine”: https://www.ioc.gov.ua/analytics/dashboard-vpo

More on the Ukrainian housing market and forecast for the segment, as well as the rest of the construction market will be in our Winter Forecast Report Ukraine to be out on 12 December, along with our other 7 country reports. To obtain it and check a sample report: https://eecfa.com/

EECFA released its 2025 Summer construction forecast on 23 June. See a sample report and place your order on eecfa.com. To get discounts, you may contact us.

Southeast European construction markets up to 2027

According to Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian research institute, total construction output in Bulgaria is anticipated to grow by 3% on average for 2025-2027 with a stronger growth in the middle of the period when the absorption of operational programmes and the implementation of the Recovery and Resilience Plan are to gain momentum. According to the sectoral breakdown, residential construction is expected to be the subsector with the weakest performance, while non-residential construction and particularly civil engineering are predicted to see stronger growth figures. Against this backdrop, the country’s economy is set to register a slower-than-expected growth in 2025 and 2026. In parallel, it is awaited to benefit from the effects from the full Schengen area membership effective from the beginning of 2025 and from the euro adoption expected on 1 January 2026.

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members think that Croatia’s construction as a whole continues vibrant due to the combination of continuing transitioning-economy catch-up growth and large inflows of EU money. Both are beginning to diminish, however, and that will affect all construction segments, some more strongly and more quickly than others. In building construction several sectors have seen the end or are close to seeing the end of catch-up growth. Others, particularly those that benefit most from EU finance, are still going strong. Civil engineering continues to profit greatly from EU funding, and because of the poor initial condition of Croatia’s infrastructure after independence, much catch-up construction remains to be done. Certain government policies will have a great influence on specific building and civil engineering sectors. Those policies include the housing policies embodied in Croatia’s new National Housing Policy Plan until 2030, the new tax on real estate and the country’s renewable energy permitting and electrical grid hook-up fee rules.

‘Romania’s macroeconomic outlook remains positive, but more reserved as the political instability and fiscal uncertainty have done little to improve growth opportunities’ – says Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild. At the same time, he adds, the country has the largest government deficit in the EU, which will dampen public investment capabilities. All these will make it harder to finance public works and could negatively impact civil engineering. This is doubly worrying as this subsector countered the decline in other construction segments in 2024, and thus the outlook for total construction remains negative in 2025 and 2026 in real terms. Not all is gloom and doom, however. As inflation and interest rates come down, and employment indicators remain strong, private consumption could boost demand for residential and non-residential construction.

‘In 2025 Serbia’s construction is making new gains in building construction, while civil engineering has entered a period of consolidation after the strong expansion during 2023 and 2024′ – believes Dejan Krajinović, EECFA’s Serbian researcher at Beobuild. Building construction is supported by both public and private investments, boosted by the hosting of the EXPO 2027 in Belgrade. Non-residential construction is the main beneficiary of this event, particularly commercial, office and hotel segments, while residential construction is also keeping historically high volumes. Some delays are seen in civil engineering, but the overall performance is still strong with a long list of planned projects in all major subsegments. Domestic demand is still relatively strong, but economic growth and the level of investments are being muffled this year by uncertainties in the global markets, particularly the weak EU economy, international trade issues and the ongoing wars in Ukraine and the Middle East.

‘Total construction output in Slovenia is expected to decrease from the historic high of EUR 5,5 billion reached in 2023. In both 2024 and 2025, it could contract but remain above EUR 5 billion annually’ – as per the opinion of Dr. Aleš Pustovrh at Bogatin, EECFA’s Slovenian member institute. He predicts the sector to return to growth in 2026 and 2027, mostly on the back of a healthy growth in residential construction buoyed by decreasing mortgage rates. On the other hand, civil engineering is prognosticated to shrink significantly in 2024 and 2025 due to some large projects nearing completion, like the new railroad connecting Port Koper. Both non-residential and civil engineering depend to a large degree on public financing that was widely available in the post-Covid period but will become much less available in 2025-2027. Especially if the overall economic activity continues to slow down. This deceleration and more foreign labourers have also caused lower construction cost growth, but other challenges persist such as the additional bureaucratic burdens (changed permitting process, increase in tax, ongoing discussion on changes to short-term rental legislation, among others) and many external risks in the global economic and political environment.

Eastern European construction markets up to 2027

‘In the forecast horizon, the construction sector of Russia will be under pressure from a range of macroeconomic factors, the main one being the high key rate, which will negatively affect the pace and volume of construction projects’ – according to Andrey Vakulenko at MACON, EECFA’s Russian research institute. The tight monetary policy and the reduced availability of mortgages will likely slow down housing construction, on the one hand. On the other, the high cost of project financing, the general cooling of the economy as well as reduced consumption and business activity will likely shrink the volume of investment in non-residential construction. However, these trends can partly be offset by high volumes of government financing of priority infrastructure and energy projects, which can support civil engineering and ensure near-zero growth in total construction market in 2025-2027.

Prof. Ali Türel, EECFA’s Turkish researcher says that Türkiye has been trying to control high inflation by raising the base rate and managing exchange rate increases through market instruments by the Central Bank and maintaining wage growth at zero or negative rates. This created financing difficulties for industries and businesses, reduced demand for basic consumer goods, and led to affordability problems for mortgage credits. Big declines in building starts and completions in Q1 2025 may also be related to these measures. Yet, the Central Bank’s inflation target for 2025 remains high at 24%. Positive real changes in housing prices relative to building construction costs encourage house building, while their negative real change compared to inflation may be the leading factor in the increase of home sales through equity financing when mortgage credits are not affordable for most households. Rebuilding the quake-damaged 870 thousand units requires about EUR 100 billion and these expenditures have been the primary factor of the large national deficits in recent years.

‘This year, in spite of the continuing war and the economic instability in the country, Ukraine’s construction industry shows signs of recovery and growth on the back of successful programs financing both the construction of new facilities and the reconstruction and restoration of infrastructure in eastern and southern regions’ – according to Prof. Sergii Zapototskyi at Uvecon, EECFA Ukraine. The World Bank estimates that reconstruction would require USD 486 billion. On the negative side for the sector are bureaucratic barriers in the urban planning legislation, shortage of workers caused by mobilization, shortage and high cost of building materials, and logistical difficulties. On the positive side for the sector is demand for housing and the need to restore damaged infrastructure. The near-term future of the industry depends on the level of security, the effectiveness of restoration programs and the volume of international investments.

A Boston Consulting Group (BCG) idén februárban publikált egy tanulmányt a tavaly felülvizsgált EU-s EPBD irányelv apropójából, amelyben az energiahatékony anyagok és technológiák iránti jövőbeli keresletet modellezte. A tanulmány szerzői: Johannes Blauhuth, Lorenzo Fantini, Martin Feth, Jannik Leiendecker, és Alberto Pizcueta. Kőrösi Péter (ELTINGA) összefoglalója.

Klímasemleges új épületek az EU-ban 2030-tól

A klímavédelem célkeresztjébe került a legnagyobb energiafogyasztó Európában: az építőipar. Európa szén-dioxid-kibocsátásának több mint egyharmadáért az épületek felelősek, ami összefügg azzal, hogy energiahatékonyságuk átlagosan igen alacsony. Emiatt az épületállomány dekarbonizációja középtávú uniós irány – már rövid távon is érzékelhető célkitűzésekkel.

Az Európai Unió célja a fosszilis tüzelőanyagok fokozatos kivezetése és a megújuló energiaforrások elterjedésének felgyorsítása, ezért tavaly májusban felülvizsgálták az épületek energiahatékonyságáról szóló irányelvet (Energy Performance of Buildings Directive – EPBD). Az új irányelv előírja, hogy a 2030-as évek elejére az épületállomány legrosszabbul teljesítő elemeit fel kell újítani, 2035-re pedig a lakóépületek energiafogyasztását 20–22%-kal kell csökkenteni. Továbbá 2028-tól minden új középületnek, 2030-tól pedig minden egyes új épületnek zéró kibocsátásúnak kell lennie.

A tagállamoknak 2026 májusáig kell átültetniük az irányelvet a nemzeti jogrendbe.

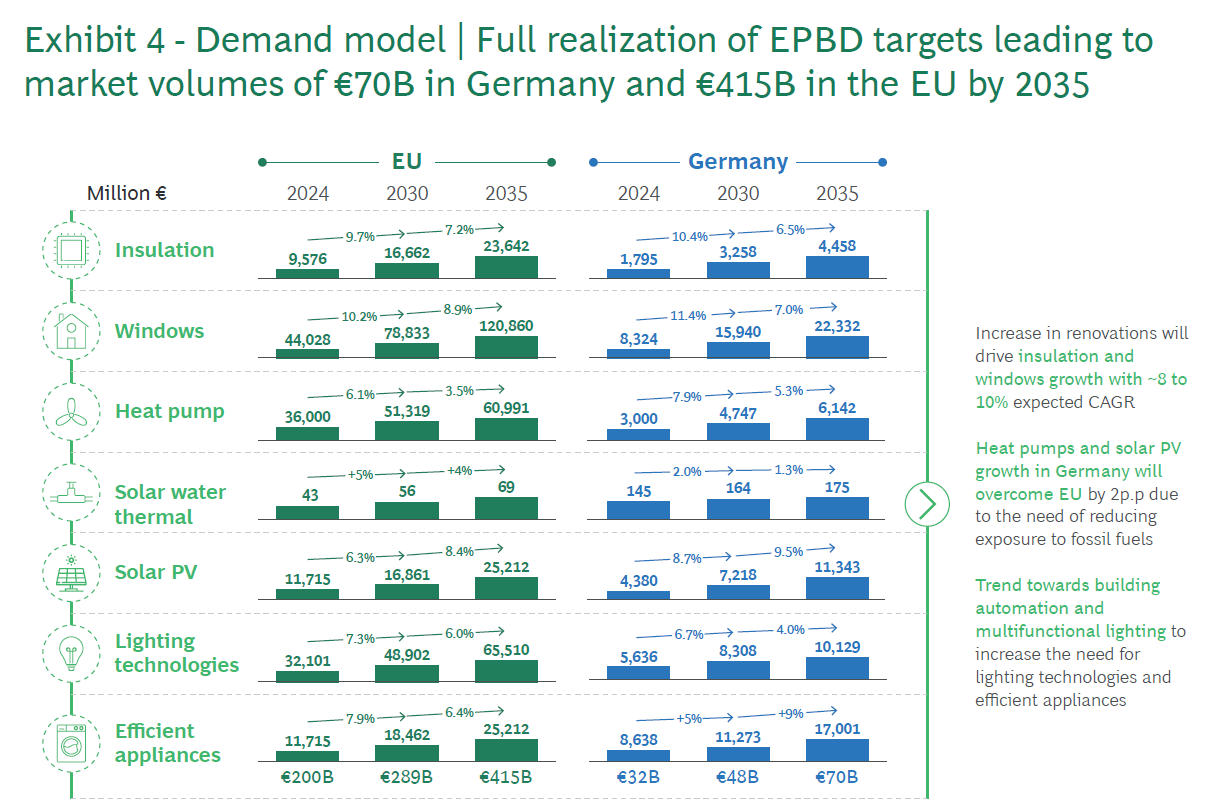

A BCG előrejelzése az energiahatékony építési technikák és anyagok iránti keresletre

Az új irányelv várhatóan már a következő negyedévekben hatással lesz az európai építőipar működésére. Bár a nemzeti szabályozás kidolgozása némi időt vehet igénybe, az első lépések már befolyásolhatják a befektetői döntéseket és a közbeszerzési szabályokat, különösen a középületek és az energetikai felújítások esetében.

Ha az EU-s célok teljes mértékben teljesülnek, jelentős felújítási hullámra számíthatunk és a zöld építkezés is fellendülhet. A BCG előrejelzése szerint a modern szigetelőanyagok és a nagy hatékonyságú ablakok iránti kereslet évi körülbelül 10%-kal, míg a hőszivattyúk és napelemek iránti kereslet évi 6-8%-kal bővülhet.

A lenti ábra a keresletet modellezi az EPBD-célok teljes megvalósulása esetén, mely 2035-re 70 milliárd eurós piaci volument jelent Németországban és 415 milliárd eurós piaci volument az EU-ban.

Az EPBD célkitűzéseihez időben alkalmazkodó vállalatok előnyre tehetnek szert versenytársaikkal szemben az egyre szigorúbb energiaszabványok és a fenntartható építési trendek környezetében.

Forrás: Boston Consulting Group (BCG), White paper: The building sector and EPBD – Demand impications for energy-efficient materials and technologies, February 2025 by Johannes Blauhuth, Lorenzo Fantini, Martin Feth, Jannik Leiendecker, and Alberto Pizcueta.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Reading the recent blog post regarding permit and completion data one can see that the trend for residential permits in Romania seems to have taken a downturn since 2021, and this naturally raises the questions: What has happened? Has the market peaked or is it just a temporary setback?

The supply-side story

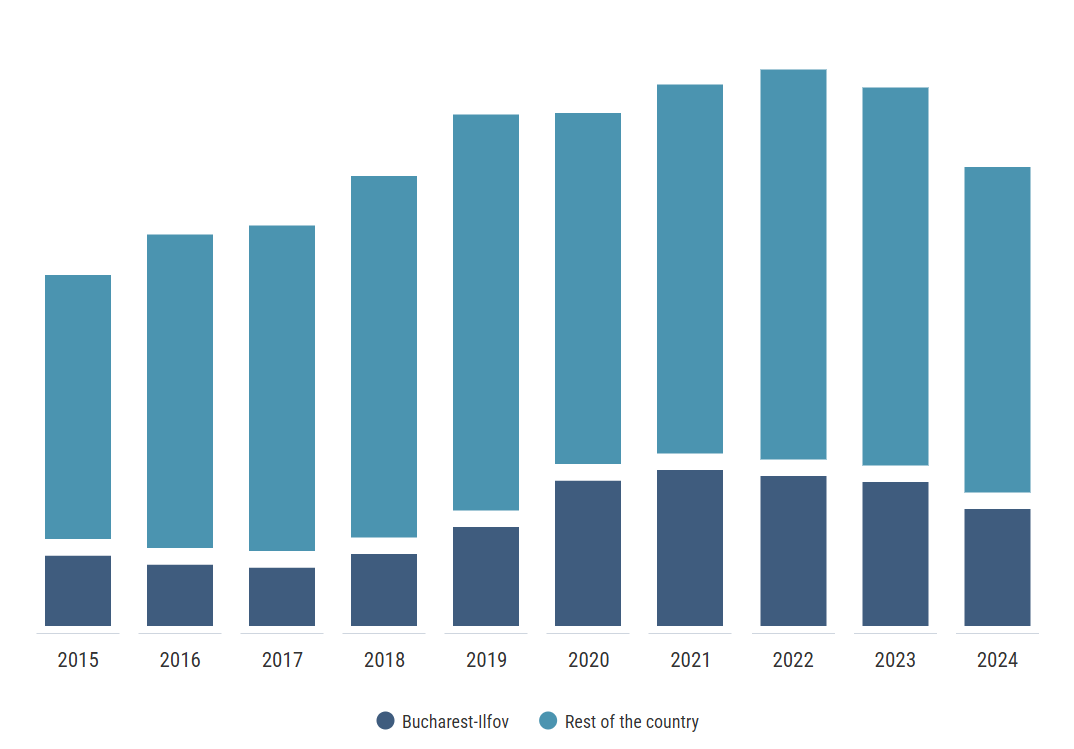

In order to attempt answering these questions, Dr. Sebastian Sipos-Gug, EECFA’s researcher on Romania, started by looking at permit data for a longer period and split by regions. The slowdown in 2023 and 2024 was present in most regions, but none of them was hit as hard as Bucharest where the useful area in residential permits nearly halved in 2024 compared to the peak of 2022. Thus, whatever effect led to the drop in permits, it disproportionately affected Bucharest. While it remains by far the most active region, the drop is oversized when adjusted for its share of the market.

In case of Bucharest, a non-trivial amount of this effect could be explained by the gridlock in the urban planning area, with permits for all types of construction hindered by the cancellation in 2022 of the existing zoning plans which have yet to be replaced by newer versions. This makes it more difficult to gain permits for new developments, and could be, at least partly responsible, for the observed shrinkage in residential permits in the last two years.

Figure 1: Useful area in residential permits, 2015-2024, Bucharest-Ilfov chart presented outside the map due to relative market size (Source: own calculations based on NSI data)

The next logical step seemed to be looking at other indicators such as completions and seeing what happened there. Indeed, they have also been on the decline with the number of completed homes country-wide in 2024 being comparable to that of 2018. Again, Bucharest-Ilfov saw a much larger drop in 2024 over the 2021 figures, standing at –33% compared to –12% in the rest of the country.

Figure 2: Home completions between 2015-2024 (Source: own calculations based on NSI data)

The decline is quite apparent in the supply of new housing overall, but that the situation is much more dire in Bucharest.

The demand-side story

Could the decrease in supply be a response to lower demand? After all, if developers have difficulties selling stock, they are unlikely to start new projects.

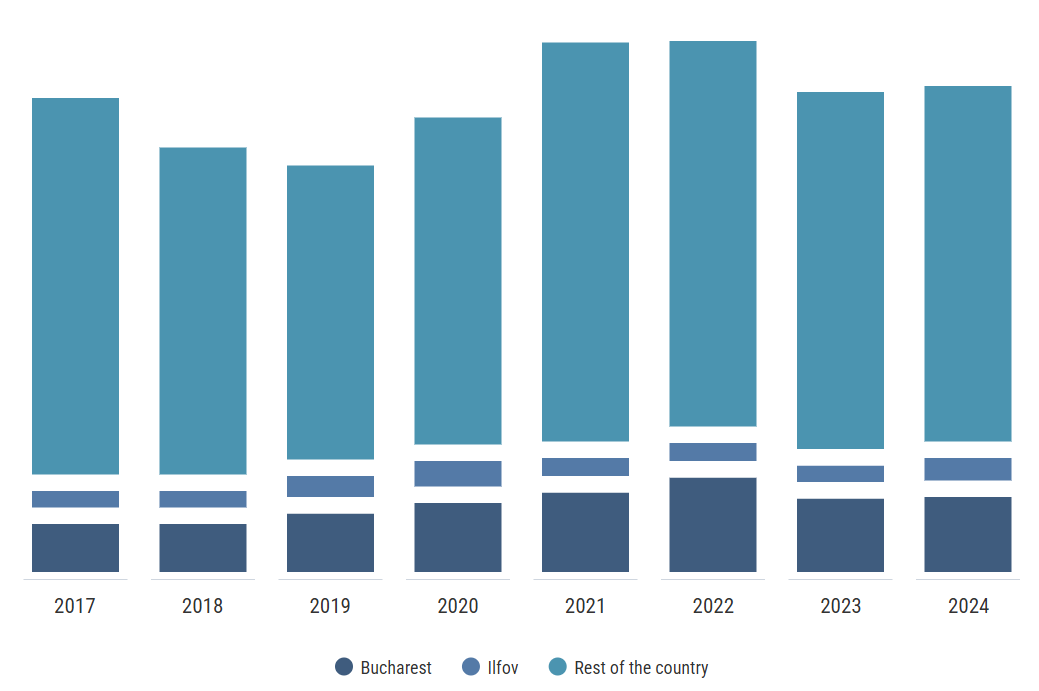

Looking at the number of transactions, they indeed declined overall in 2024 compared to the peak of 2021, but the effect was much smaller with just around 10% fewer properties being sold in the whole country, while in the Bucharest-Ilfov region there was barely any change (-0.3%).

At the same time, prices of homes continued growing, but this time Bucharest (+20%) lagged behind the country (+27%), meaning that the price gap between the capital and the rest of the country is slowly closing.

Figure 3: Number of real estate transactions between 2017 and 2024 (Source: own calculations based on ANCPI data)

However, when comparing the growth in home prices to that of the rise in construction costs, the situation looks more dire. As of 2024, residential construction costs grew 41% over the 2021 level, far outpacing the increase in prices. This was partly due to increased materials costs (+32%), but also due to much higher labor costs (+60%) for construction workers. Since in January 2025 tax breaks for construction workers were eliminated and the minimum wage for them grew, it’s unlikely for the situation to improve in the short term, potentially discouraging developers from new investments until prices reach a place where they offset the costs and offer similar margins as before.

What does this mean for housing affordability?

This topic was touched upon last year, in another blogpost, with the conclusion that it is useful to look at affordability from two standpoints: cash buyers and mortgage takers, since increased interest rates can negate the effects of wage growth.

Taking a regional split into account this time, it’s noticeable, and perhaps slightly surprising that homes are more affordable in Bucharest as the wage gap between it and the country average is higher than the residential prices gap.

This took a turn, however, in 2024 as home affordability in Bucharest started to drop, while the national average remained more or less the same. If the previously mentioned issues that limit permitting are not resolved, we can expect this trend to continue in the future as well since a limited supply will mean higher prices.

Another factor that could limit future supply, at a national level, is developer funding. It used to be the case that developers would focus on presales and use very high downpayments in the project phase (up to 90% in some cases) to fund the construction work, without requiring a bank loan.

Since a high-profile scandal regarding a large developer brought this issue into the limelight, confidence in this type of arrangement has declined and buyers are less likely to accept paying high downpayments before construction has even started. Concurrently, there is a bill underway aiming to limit downpayments for unfinished buildings to 10%. Should developers resort to banking loans for their projects, it would make the market more stable but more expensive for them, leading to either lower margins, or higher prices.

Figure 4: Home affordability for cash buyers: sqm in an average 2-room apartment one could afford with average monthly net wage (Source: own calculations based on data from NSI and imobiliare.ro)

When it comes to home affordability for those using a mortgage loan, things are not looking better than they did last year. Inflation has proved to be stickier than expected, and the Central Bank is lowering reference interest rates slowly, meaning mortgages will continue to be relatively expensive in the near future.

While the higher wages in the capital again prove to be an advantage, making homes slightly more affordable than for the average Romanian, this indicator was also on the decline in 2024 for Bucharest, and stable for the rest, shrinking the gap between the two.

Figure 5: Home affordability for mortgage buyers: size of the home (in sqm) one could afford to buy with a mortgage loan, assuming a 25% downpayment, a 30-year term and a debt-to-income ratio of 40% of the average monthly net wage (Source: own calculations based on data from NBR, NSI and imobiliare.ro).

In the context of high energy costs, in 2021 construction costs increased. Since then, the situation has not improved dramatically, and it’s unlikely to change in the near future as inflation and high wage growth will keep an upwards pressure on them in 2025 as well.

Bucharest is doubly feeling the pain when it comes to new residential development. Adding to high construction costs, there are issues with urban zoning and permits approvals. The supply constraints mean higher prices, leading to slightly declining home affordability, especially for those relying on mortgages.

Figure 6: Construction costs for residential buildings (Source: own calculations based on data from NSI)

Forecast for the Romanian residential market is available in the EECFA Forecast Report. EECFA conducts research on the construction markets of 8 Eastern-European countries, including Romania. Contact us for orders and sample report