A tavalyi rekord magas szintről ugyan visszaesett, de a megkezdett társasházi lakásépítési munkák összértéke az év eddigi részében még mindig magasnak mondható. A nem-lakás magasépítési részpiac az ami igazán gyenge; itt a tavalyi ritka alacsony Aktivitás-Kezdéshez képest látunk jelentős visszaesést. A második negyedévben elkezdődött a Visontai CCGT erőmű építése, így a mélyépítés növekszik. De a nagy növekedés azért csalóka, a tavalyi első félévben a projekt-kezdés rekord alacsony volt.

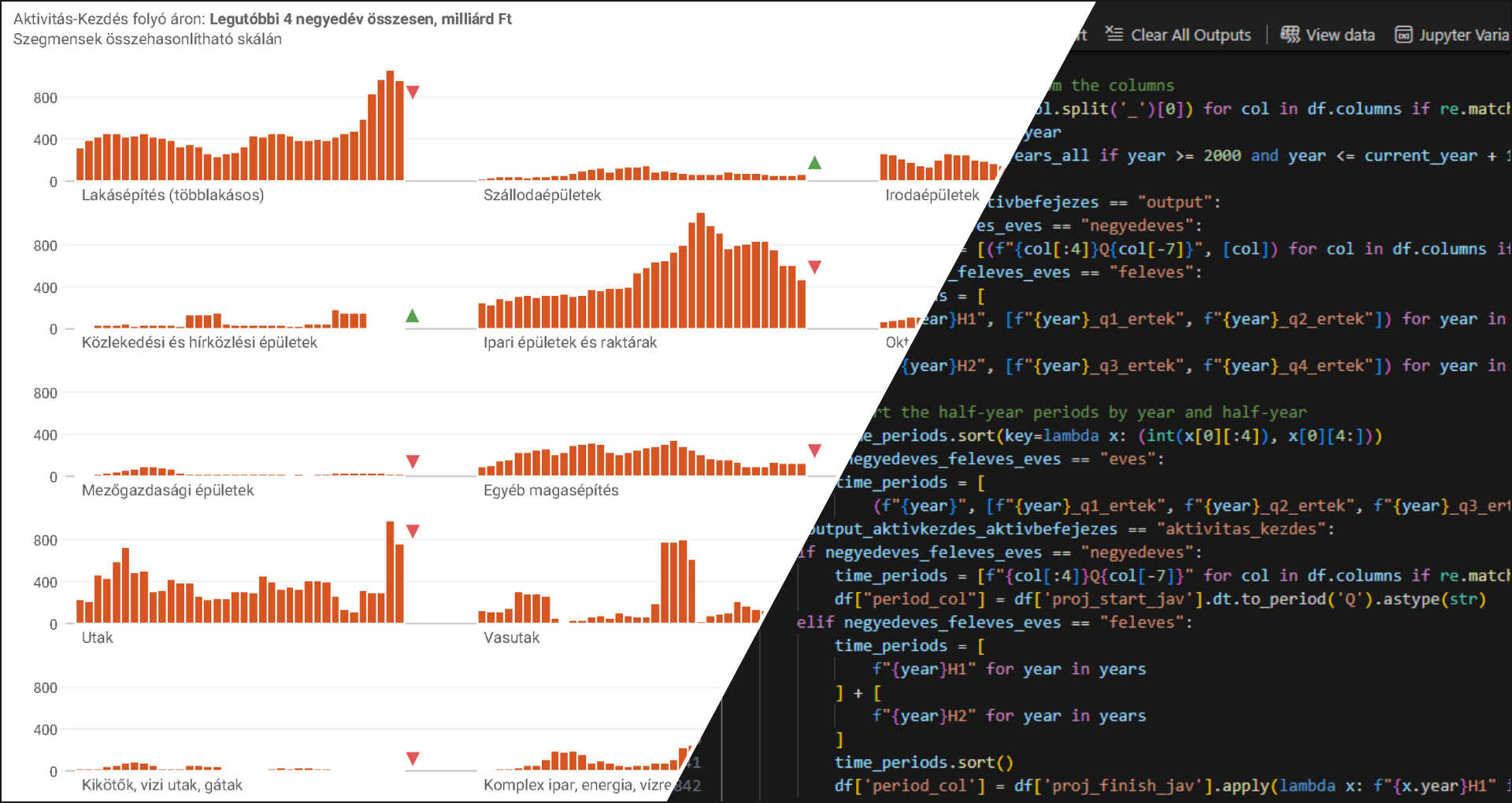

A poszter a két nagy építési részpiac Aktivitás-Kezdés indikátorának időszak/időszak változását mutatja, valamint a szegmenseket amelyekben a legnagyobb értékben indultak kivitelezések. Ezt a posztert minden hónapban kitesszük ide a blogunkra. A teljes építési piacot részletesen bemutató EBI Építésaktivitási Adatvizualizációt (összesen 18 szegmens adataival) is havonta frissítjük, és negyedévente az EBI Építésaktivitási Jelentésben is elmondjuk, hogy mit látunk a piacon. Ha érdeklik a részletek akkor a contact oldalon írjon nekünk.

Although it dropped from last year’s record high, the total value of started multi-unit residential construction works so far this year can still be considered high. The non-residential construction submarket is the one that is really weak; here we see a significant decline compared to last year’s quite low Activity-Start. In Q2 the construction of the CCGT power plant started in Visonta, so civil engineering Activity-Start is increasing. But the high growth is misleading as project starts were at a record low in the first half of last year.

The poster (above) shows the period/period changes of the Activity-Start indicator in the 2 main submarkets and the segments with the largest value of started works. This poster is published every month here in the blog. The EBI Construction Activity Data visualization with the details on the whole construction market (with altogether 18 segments) is also updated monthly and the EBI Construction Activity Report, summarizing what’s happening in the market, is published in each quarter. If your interest in construction markets is deeper, please contact us for the details.

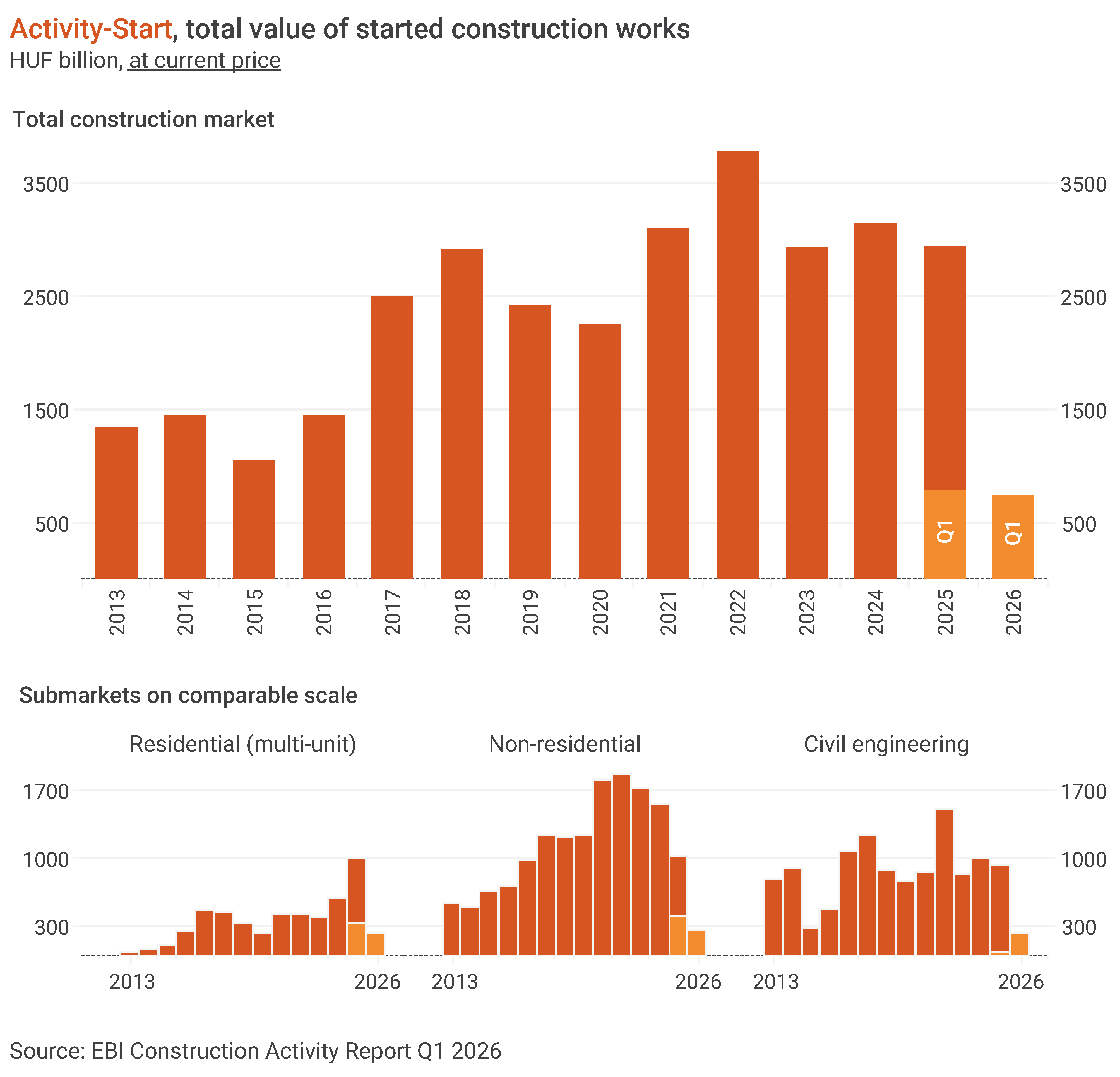

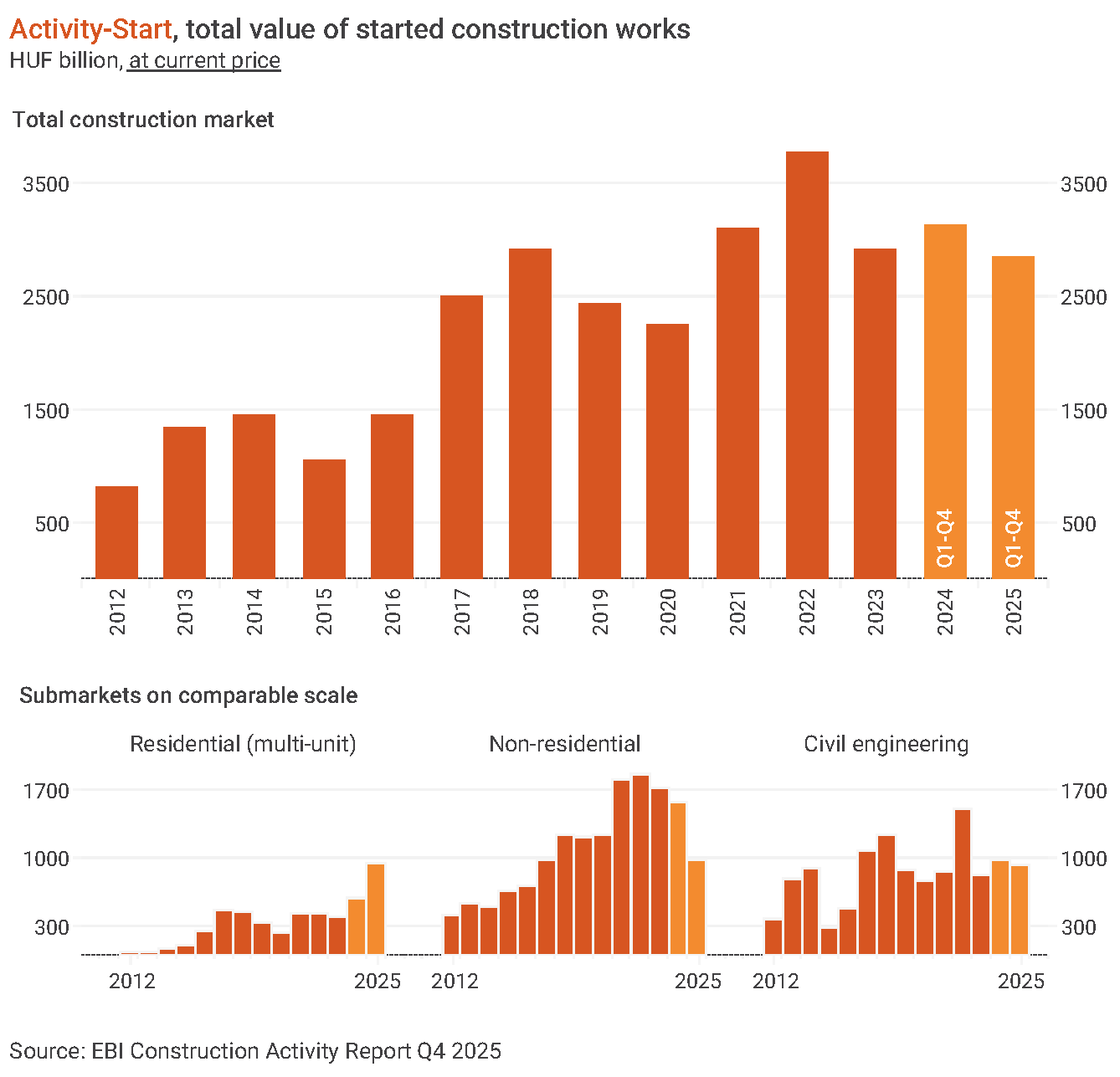

As per the latest EBI Construction Activity Report, 2026 did not start badly in Hungary for construction. Activity-Start in Q1 did not substantially lag behind Q1 2025 and Q1 2023, in fact, it slightly exceeded the average quarterly values of these years. At the same time, the start of foundation works of Block 5 of Paks 2 nuclear plant played a major role in higher numbers, adding a more nuanced picture. Projects worth around HUF 740 billion entered construction in Q1 2026. At constant price, Activity-Start did not lag greatly behind the same period of 2025 (-9%), but we have still seen the weakest first three months since 2016.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To obtain the report, please contact us.

Building construction returns to last year’s level

2026 started much weaker in building construction than last year, but the Activity-Start of around HUF 500 billion was roughly in line with the average quarterly level of 2025 and was only 6% below the average quarterly value of 2024. Hence, no major decline compared to the previous two years at current price. Even at constant price, the value of construction projects started in the first three months was close to the average quarterly level of last year, but it was double-digit below the average three-month Activity-Start between 2016 and 2024.

Multi-unit housing construction is still the segment keeping building construction at a higher level. Activity-Start for non-residential construction between January and March this year (HUF 263 billion) exceeded the average quarterly value of 2025, which was considered weak, but fell 33-44% short of the average values between 2021 and 2024. At constant price, this year’s first-quarter Activity-Start has been one of the weakest since 2015.

Biggest started non-residential projects in Q1 2026 comprised several logistics and office buildings such as Phase 3 of Láng-negyed V1 office building and Frontiers Campus office and research centre in Budapest, and the renovation of BorsodChem offices in Kazincbarcika, Phase 3 of CTP VCS5 Logistics Centre in Vecsés, building D of VGP Park Beta logistics centre in Győr, building B of Panattoni Logistics Park in Mosonmagyaróvár, and Phase 1 of Penny Market logistics centre cold storage in Alsónémedi.

Paks 2 boosted civil engineering figures

In Q1 2026, the value of started civil engineering works neared HUF 240 billion boosted by the start of foundation works of Block 5 of Paks 2 nuclear plant, while the Activity-Start in road and railway projects was only HUF 20 billion. Apart from Paks 2, only one civil engineering project got into the largest projects in Q1 2026: the construction of Phase 2 of the industrial park in Nyíregyháza.

Budapest: regional heavyweight again

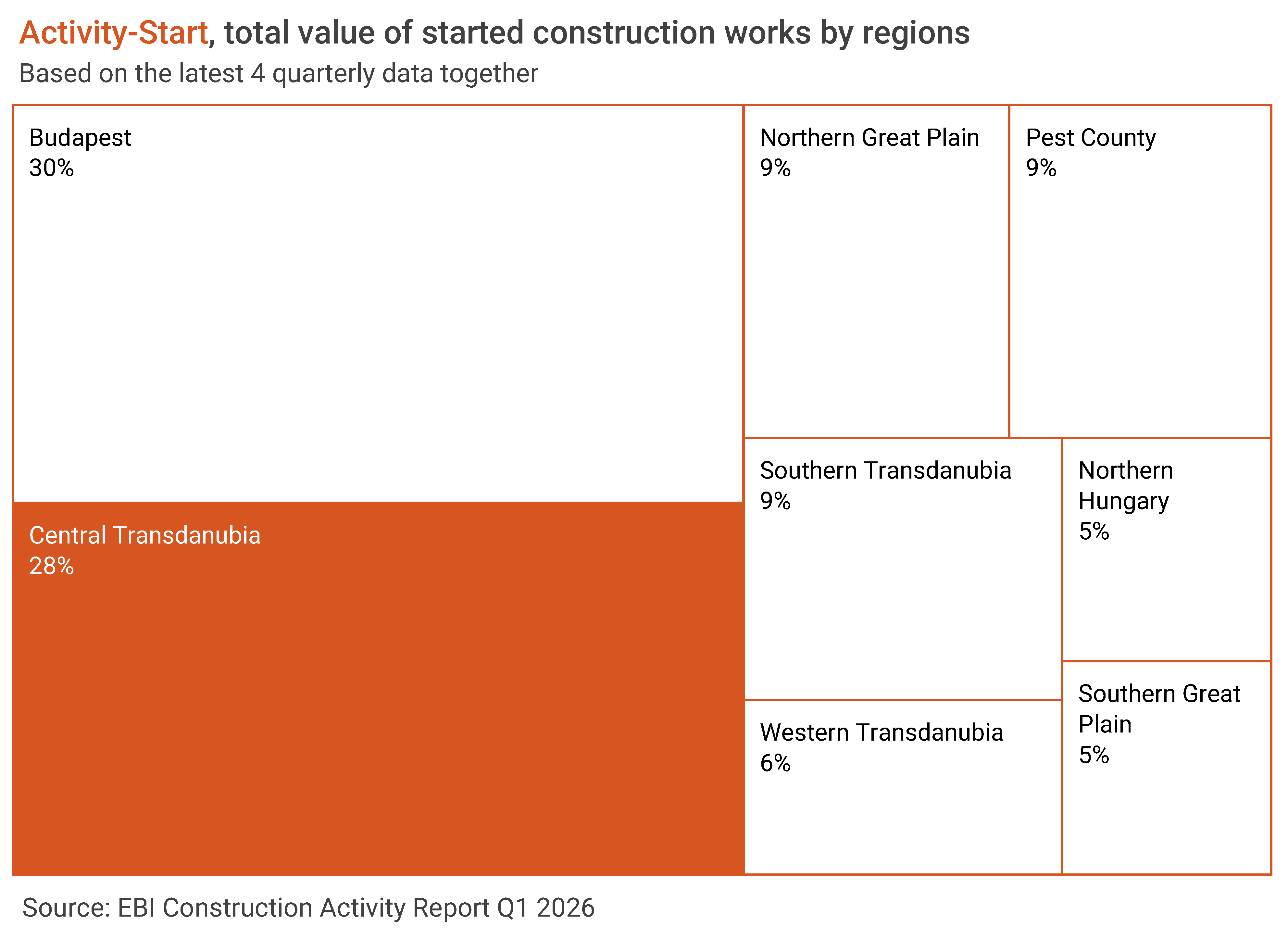

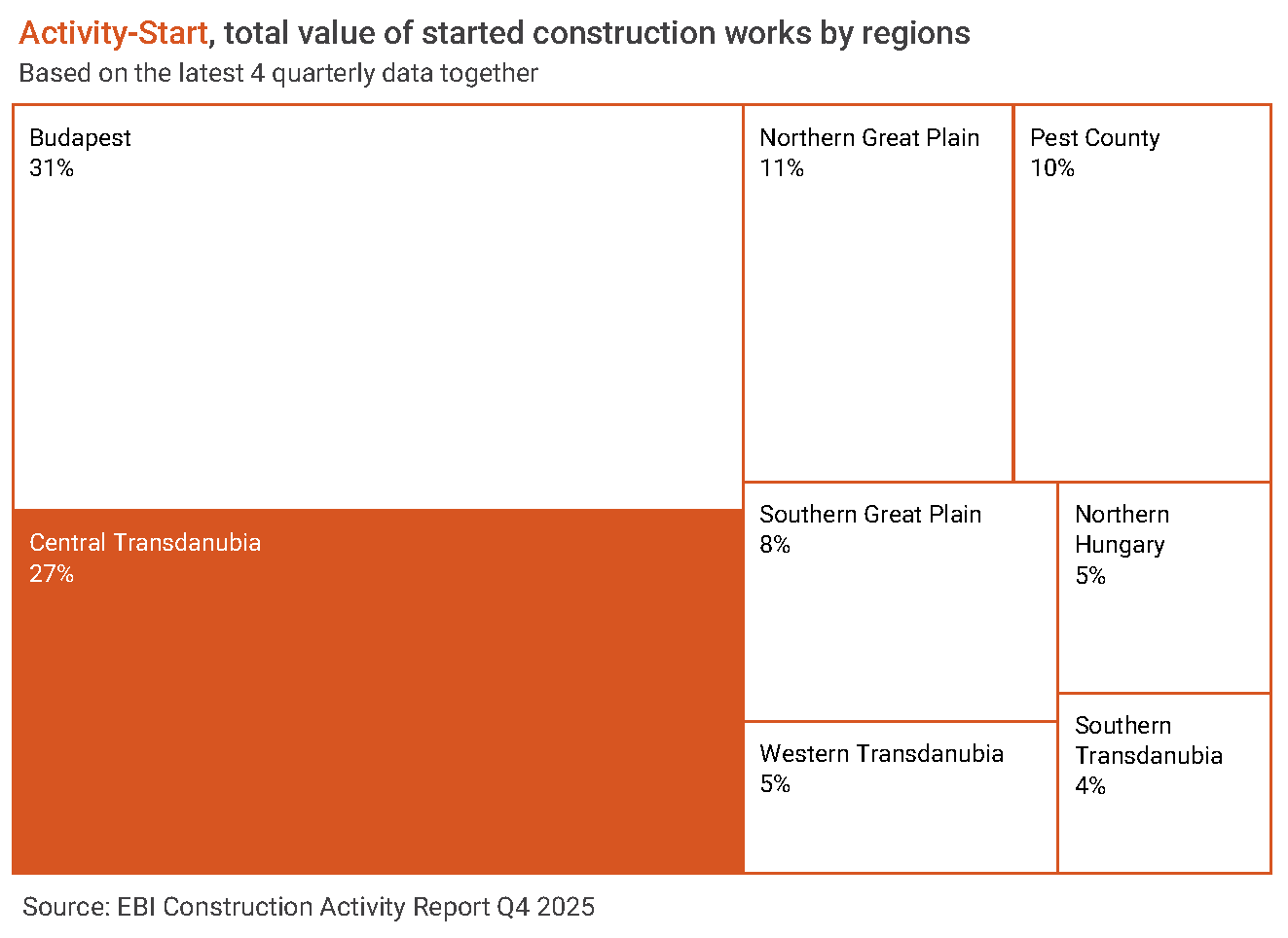

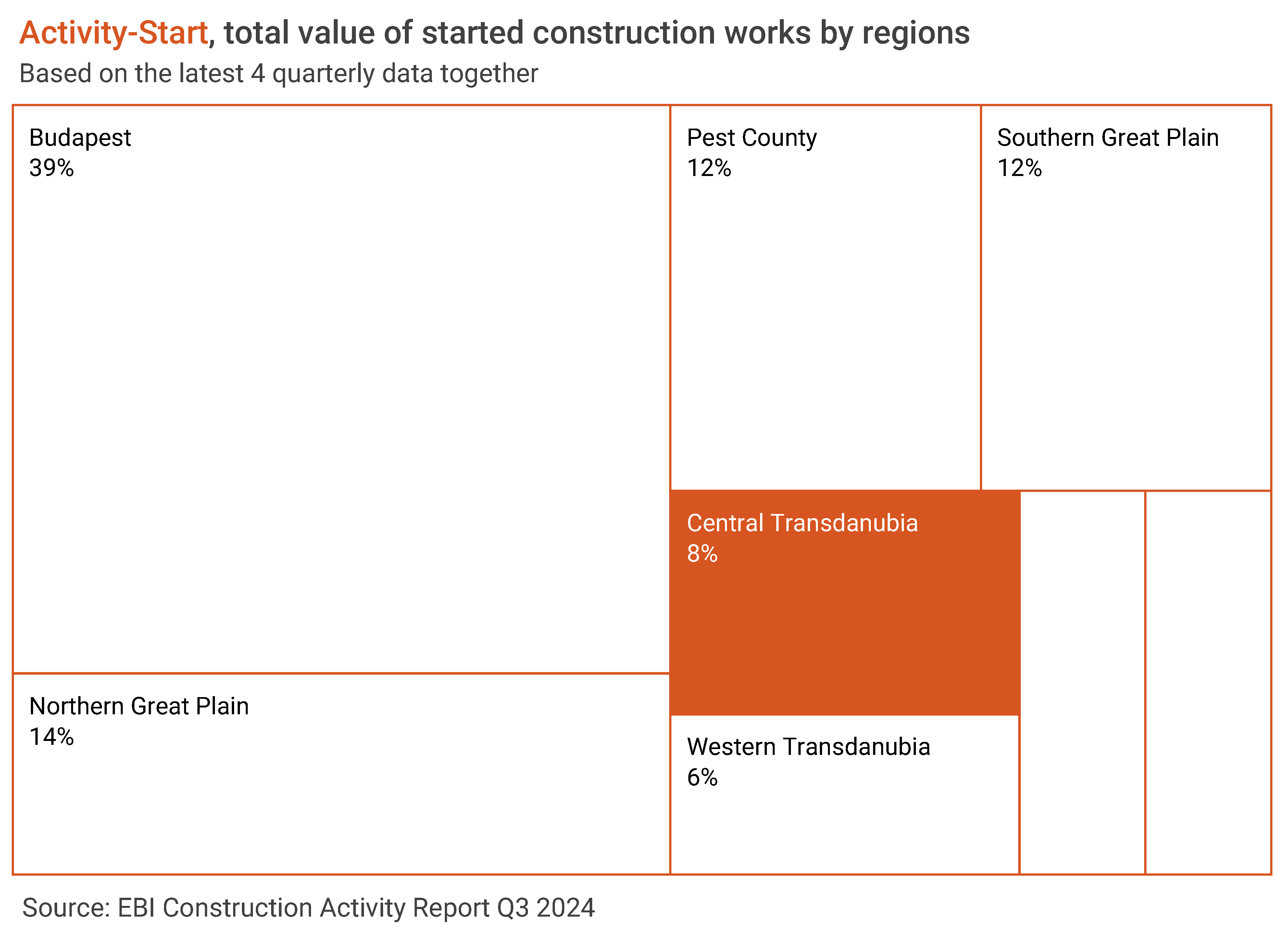

Budapest continued to be the region with the highest value of construction works started in Hungary with a share of 30% in total Activity-Start in Q1 2026. Based on the four-quarter moving averages, the share of Central Transdanubia was still considerably higher than in previous years thanks to the M1 motorway expansion launched in Q3 2025. Pest County, Southern Transdanubia and the Northern Great Plain accounted for about 9% of started constructions, while the share of other regions varied between 5% and 6%.

Multi-unit home construction still high

After a weaker final quarter last year, this year started with an extremely strong first three months for multi-unit housing. Between January and March, the value of started construction works exceeded HUF 240 billion at current price; the third highest quarterly Activity-Start since 2014. This value is significant even at constant price: only 2017-2018 and last year had stronger quarters.

The great increase in permits last year suggested strong activity at the beginning of this year. The latest EBI Construction Activity Report has found that many large projects have moved closer to planned start recently, also predicting a higher Q2 Activity-Start in the segment. However, there is a lot of uncertainty in the market now as projects within the Otthon Start Program are expected to be reviewed, which may change developers’ plans.

In Q1 2026 the value of completed multi-unit building was about HUF 83 billion, still considered a moderate level. At constant price, it is particularly low. But it comes as no surprise as previous years were characterized by restrained project launches, and the large-scale projects that started last year are set to be completed only later.

Looking at the past four quarters, about two-third of multi-unit building projects entering construction phase concentrated in Budapest, so the capital’s share remains exceptionally high. About 69% of projects started in Central Hungary, 13% of the Activity-Start was linked to Eastern Hungary, while Western Hungary’s share was 18%.

Non-residential construction: after a weaker last year, this year started slowly

Within the subsector, two segments accounted for the majority of the Activity-Start: offices and industry. Offices performed rather poorly in previous years but recovered somewhat in Q1 2026 with their share within non-residential construction going up to 34% compared to 9% in the previous two years. Industrial properties and warehouses continued to account for the other major part despite the decline (their share dropped to 36% against 44-54% in the previous four years). In the first three months of this year, about 9-10% of started non-residential projects were related to wholesale and retail and education.

In 2026, besides the previously mentioned office, industrial and logistics projects, the largest non-residential projects also included Cholnoky Jenő Student Camp in Révfülöp, Rheinmetall RDX explosives factory in Várpalota, Mixvill shopping center in Debrecen, and Phase 1 of MyRA Park M3 shopping park. In 2025, non-residential construction was also characterized by weaker Activity-Start, but several high-value projects were launched such as the special operations barracks in Szolnok, BYD’s assembly hall, logistics warehouse, press plant and lightweight construction plant in Szeged.

In the past three years, non-residential projects reached completion at an exceptionally high value, between HUF 1,600 and 1,700 billion. During this period, Phase 1 of eMAG logistics centre, certain elements of BMW and Mercedes-Benz projects and several logistics projects were completed, including Robert Bosch logistics hall in Miskolc. Activity-Completion indicator may remain at a high level this year as well. The Hungaroring paddock building has already been handed over and several elements of BYD projects, Samsung Göd expansion, and several CATL buildings in Debrecen may also be completed.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

There was no construction start indicator in Romania, so we have created an estimation for it.

This poster is a summary of our monthly findings. It shows how the total value of started construction works have changed over the same period last year. Besides, it presents which segments have the biggest start value in the current year. We call this indicator Activity-Start. And they are computed every month for 18 construction segments by aggregating data of construction projects. The projects are from the iBuild database and ELTINGA and Buildecon found the way of creating indicators out of them.

If you need short-term foresight, you will like it.

Brief comment from Janos Gaspar, head of Buildecon:

Building construction Activity-Start is still weak. And office construction remained the only bright spot due to the commencement of the Queens District, a large mixed used project in Bucharest. Most other segments, including the multi-unit residential, are looking bad at this phase of data collection. Despite the drop, civil engineering has a strong Q1 mostly because works started on the A8 highway.

Every month this poster will be available here on our blog. If your interest is deeper, we have the EBI data visualization (with indicators for all the 18 segments of the construction market), updated monthly and we have the EBI Construction Activity Report Romania (with data and explanations), published quarterly in English and in Romanian. All these are packed into a yearly subscription. For the specifics, please contact us.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Dr. Sebastian Sipos-Gug, EECFA’s Romanian analyst has looked at the trends that are worth monitoring in the residential market in Romania this year. Among them are the construction costs boomerang, the drop in wages and consumption, considerable interest in multi-family buildings, smaller homes and a greater dependence on mortgage loans.

What we saw in 2025

The construction market faced many challenges in the previous year, alongside the entire national economy. While there was a focus on civil engineering, especially when it comes to EU co-funded projects, the rest of the segments lagged behind.

In early 2025, the removal of fiscal facilities for construction employees led to the decline of their net incomes, and an increase in wage-related expenses for companies. Overall, the effect of this measure was an increase in construction costs.

Then came the multiple shocks of the liberalization of energy markets in July, and a VAT increase in August, which pushed inflation upwards significantly, with the CPI reaching 9.88% in September. In a snowball effect, this led to lower real wages and disposable income, which translated into a reduction in private consumption, and, ultimately, means lower demand for residential construction on the short and medium terms.

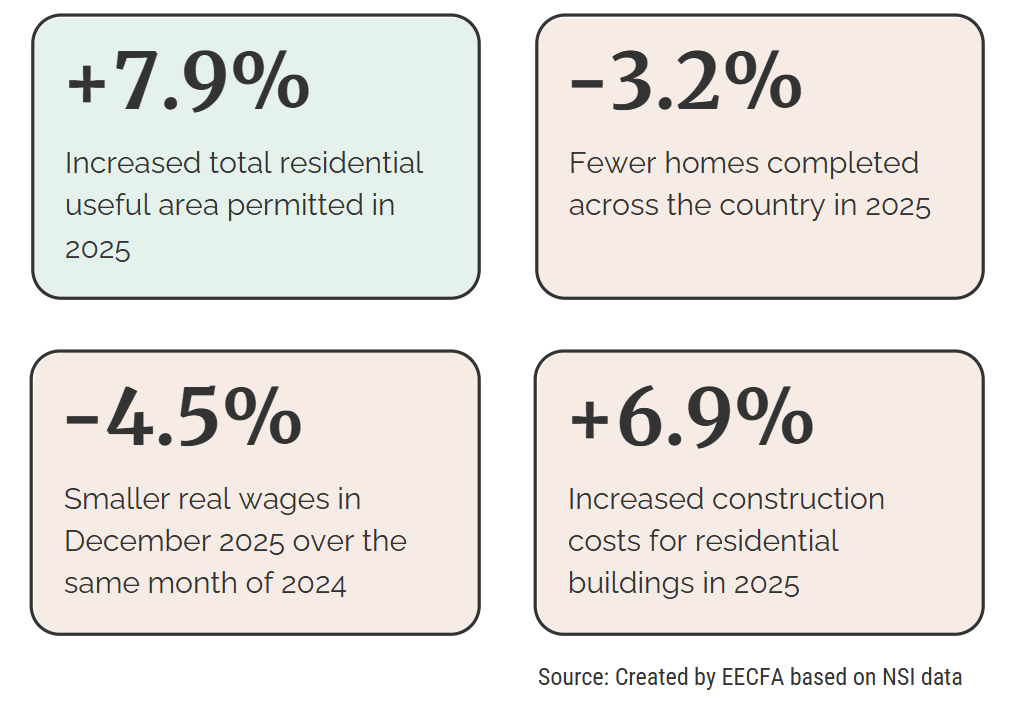

The optimism shown in the increased number of permits, and the useful building area in them, compared to 2024, is countered by the decline in the number of completed homes. Thus, while developers might be looking to the future, their actions in the present are lacking, also evidenced by a significant (-21%) annual decline in the value of started construction works in 2025 (source: EBI Construction Activity Report).

What to watch in 2026

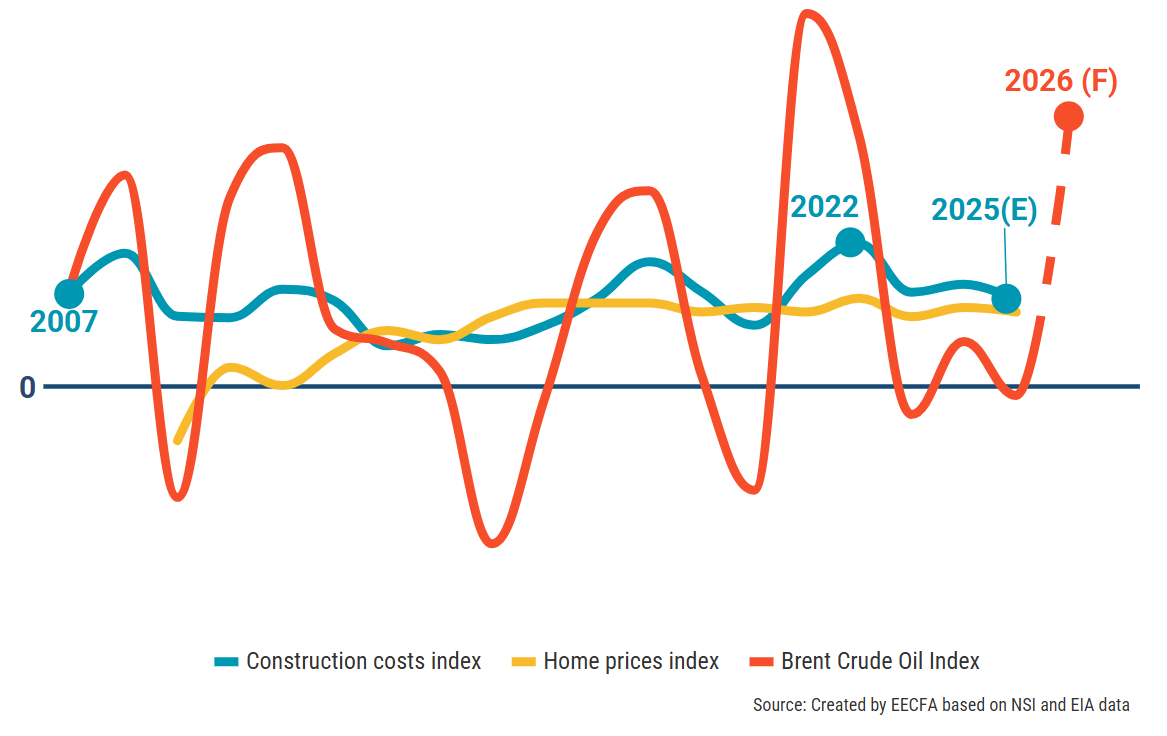

Construction costs boomerang. While previously the expectation was that construction costs would gradually decline in 2026, they proved quite resilient to changes in wages, and fuel and construction materials prices remained relatively stable in the past year. Thus, late 2025 forecasts placed construction costs on a small, descending trend.

The conflict in Iran and its repercussions on oil and gas prices might throw astray these predictions. As of March 2026, oil prices were approaching 2022 levels, and, if they are not reversed rapidly, might have a similar impact on world-wide inflation, energy prices and, eventually, construction costs. A reversal, however, seems rather unlikely at the moment as the damage to energy infrastructure could take years to undo.

To make matters worse, in the past few years home prices grew slower than construction costs, reducing potential profit margins for developers. Added to the decline in real wages, it remains quite unlikely that there will be room for prices to increase alongside construction costs, again similar to 2022, further eating into builders’ financial return potential.

Decline in wages and consumption. Wage growth for 2026 was already forecasted to remain low, underperforming inflation (source NFC – National Forecasting Commission Autumn 2025 Report). Add to that the further shocks now expected from increased energy costs (due to oil and gas prices rising considering the conflict in Iran) and food costs further rising due to increased fertilizer prices, the downwards pressure on real wages is likely to be worse than forecasted, with a slower recovery.

Real wage decline will make it harder to purchase and build new homes, with a negative impact on demand for residential construction. But it could provide a boost to renovation activity, especially when it comes to energy efficiency, as switching homes becomes harder.

High interest in multi-unit residential buildings. Looking at building permits trends for the past decade, single-home buildings have remained relatively stable, while the majority of growth was due to multi-unit buildings. Under price pressure, on the backdrop of restricted wage growth and a contractionary macro-economic outlook, it remains most likely that for the near future we’ll continue to see more interest in the latter. Another connected issue is that of internal mobility, with migration from rural to urban areas in search for education and economic opportunities, increasing demand for denser residential construction.

Smaller homes. While the mean area in permits remained relatively stable between 2017 and 2025, there is a historical precedent in economic downturns leading to smaller homes being built so as to increase accessibility. Since the economic outlook for the year seems to have worsened, this could be the case again in 2026.

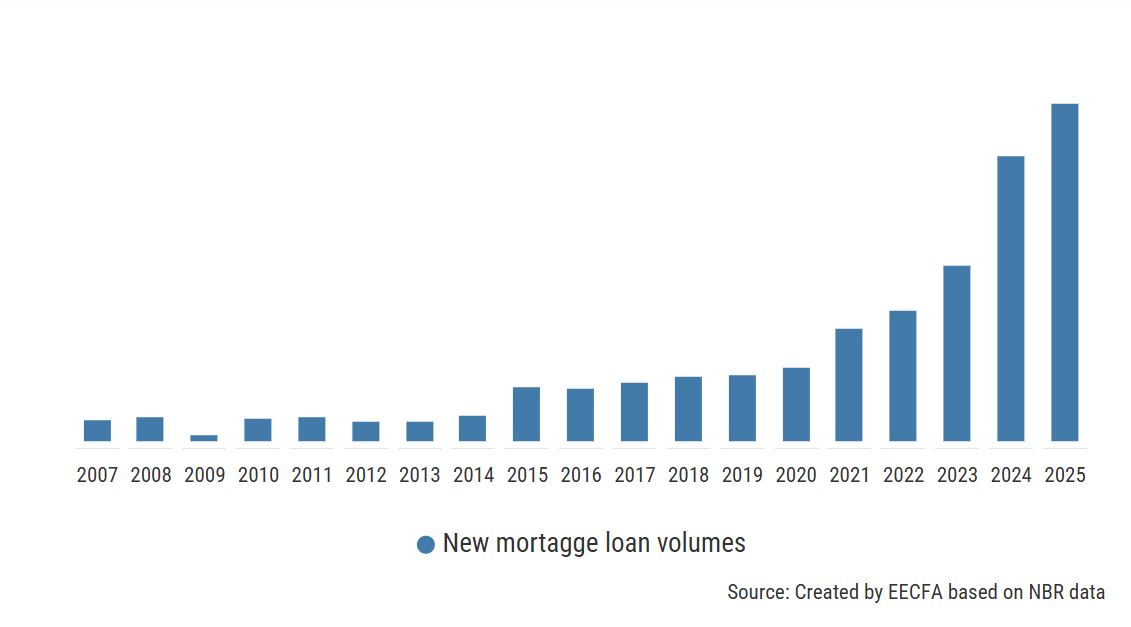

Increased reliance on mortgage loans. Despite the highest interest rates seen in a decade, the volume of new mortgage loans increased dramatically in 2024 and 2025. While some of this could be blamed on higher home prices, there remains a major portion that cannot be explained by price or transaction dynamics. Thus, it is quite likely that it reflects a reduced ability to buy homes without applying for a loan. This is also evidenced by the fact that the share of the population currently housed in a dwelling that was purchased with a mortgage loan grew steadily from a low of 0.5% in 2007, to 1.5% in 2024 (source: Eurostat). This could have been further boosted by the expected drop in interest rates as inflation seemed to be heading in the right direction. However, as of March 2026, this seems less likely, as the conflict in Iran would lead to another energy-led inflation event. Nonetheless, with real wages on the decline, mortgage loans will continue to be relied on for boosting home affordability.

Residential, non-residential and civil engineering forecasts up to 2027 can be found in the EECFA Romania Construction Forecast Report. Sample report and orders: https://eecfa.com/

The latest EBI Construction Activity Report has found that although the expansion of M1 motorway caused a considerable surge in the value of started construction projects in Q3 2025, Q4 brought very low Activity-Start. Even at current price, such a low number of construction projects did not start in a quarter in the past 9 years. However, thanks to the high numbers in Q3, annual Activity-Start only slightly sank against 2024. In total, projects worth nearly HUF 2,900 billion entered construction phase in 2025.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To obtain the report, please contact us.

Declining Activity-Start in building construction in Q4 2025

In Q4 2025, Activity-Start in building construction decreased significantly compared to previous quarters. However, due to the higher first quarter value, the full-year decline remained 10% compared to 2024, while the decrease was 8% over 2023.

Overall, construction works started in the segment last year were worth slightly less than HUF 2,000 billion, the lowest level between 2021 and 2025. Due to the significant increase in multi-unit residential construction in 2025 and the few construction starts in non-residential buildings, multi-unit residential construction accounted for almost half of building construction Activity-Start, which has not been the case since the first half of the 2000s.

Non-residential construction was characterized by a decline in Q4, and the value of started construction works was roughly at the same level as in Q2, which was also modest. For the year as a whole, non-residential Activity-Start was around HUF 1,000 billion, the lowest value in the period between 2018 and 2025. It also shows a 37.5% decline compared to 2024 at current price, and a 43% drop over 2023.

The largest non-residential projects entering construction phase in Q4 2025 included the construction of several logistics centres, such as CATL warehouse in Debrecen, Porsche Parts Center logistics-warehouse centre in Budaörs, and Building C of VGP Park Budapest Aerozone. Several hotel projects began, too, including the construction of Mama Shelter Hotel and Ruby Hotel in Budapest, and Danubius Hotel Annabella ***Superior in Balatonfüred.

M1 highway expansion boosting civil engineering Activity-Start in 2025

Following Q3 2025, which registered high Activity-Start due to the expansion of M1 motorway (M0-Concó rest area), Q4 2025 saw a very low value of started civil engineering works in Hungary. Few projects started not only in value, but also in number.

Thanks to the motorway project, annual figures tell a nicer story with projects starting in the value of nearly HUF 1,000 billion in 2025. It did not differ much from 2024, although the figures then were also boosted by the start of one large project, the construction of the Mohács Danube Bridge and related road network. Overall, in 2024-2025, apart from these two large projects, the value of civil engineering projects entering construction phase would have been very moderate. In Q4 2025 not a single project made it to the list of biggest started ones, indicating the reduction in civil engineering in that quarter.

Budapest continues to lead Activity-Start

Budapest had the highest share, 31%, within total Activity-Start in the last four quarters. Central Transdanubia also had a high proportion, more than 27%, primarily due to the M1 highway expansion. Together, more than 40% of works started in Central Hungary, 36.4% were related to Western Transdanubia, while the share of Eastern Hungary was 23%.

Sluggish multi-unit residential developer activity in Q4 2025

Q4 2025 saw another decrease in the value of started multi-unit residential constructions, with the cost value of started works falling below the level of Q2-Q3 2024, the second lowest value in the past two years.

However, 2025 overall was still a record year thanks to the high activity in the first 3 quarters of the year. Works worth nearly HUF 1,000 billion started, exceeding the Activity-Start of the previous year by 60% even at current price. At constant price, it was roughly equivalent to the record holder years of 2017-2018.

2026 may also register strong multi-unit residential construction as last year’s preliminary data shows surge in building permits. Further boost may come from the Otthon Start Program which was launched in September 2025 (subsidy helping first-time homebuyers secure up to HUF 50 million in mortgage financing with a fixed 3% interest rate and a maximum 25-year term) and the Capital Program, which was also started last year. In connection with the former, the construction of several thousand units has been announced in priority projects, and applications for several thousand more may be given green light. Since sales deadlines must also be met in priority projects, their start is expected soon with many construction works beginning this year.

The weaker project start in recent years was also visible in the Activity-Completion indicator in 2025. Multi-unit homes worth a total of HUF 370 billion were completed last year, roughly 8% below the 2024 value.

Regionally, in the past 4 quarters, most multi-unit residential Activity-Start was related to Budapest with 68% of works starting here in 2025. Central Hungary, including the capital city, accounted for 70%. 16% of works started in Western Hungary and 14% in Eastern Hungary.

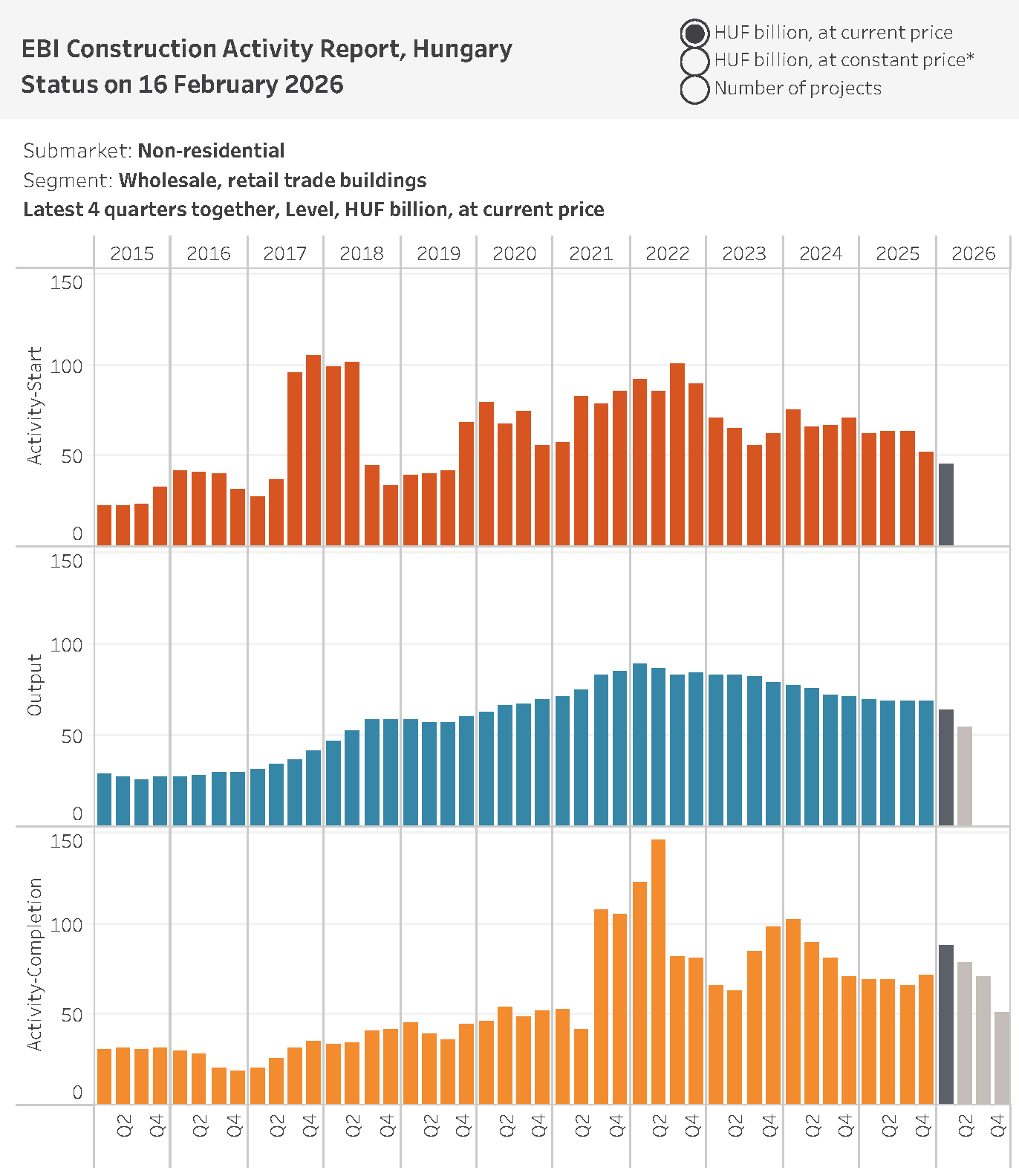

Moderate wholesale and retail Activity-Start in Q4 2025

The last time an outstanding Activity-Start was registered in wholesale and retail was in 2017 and 2021-2022. In 2017 the start of construction of Etele Plaza contributed with the highest value, while in 2022 two big project starts played a major role in higher numbers (ActiCity Event Center in Veszprém and Phase II of Zenit Corso shopping centre in Zugló).

2025 brought a rather modest Activity-Start in wholesale and retail, works started by a 27% lower value than in 2024. The decline compared to 2023 was also 16%, roughly at the level of 2020, and the shrinkage compared to the peak years (2017 and 2021-2022) was 39-50%. Despite the drop, larger projects began last year, such as OBI DIY store and Drive-in in Kistarcsa and Stop Shop in Salgótarján.

In 2025, a total of HUF 71 billion worth of wholesale and retail properties were completed, the same as in 2024, for example, the shopping court in Táncsics Mihály Street in Komárom, Phase I of Time Out Market in Budapest, Mömax home improvement store in Székesfehérvár, and Spar store and Dera Park shopping park in Szentendre.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

The latest EBI Construction Activity Report Hungary has found that it was mainly due to the ongoing M1 motorway expansion that the value of started construction projects rose significantly in the third quarter of this year. The value of projects entering construction in July-September 2025 exceeded HUF 1,000 billion at current price – the second highest level in the past ten years. Without this motorway expansion, accounting for around 60% of Activity-Start, the figures would have been much more modest, though.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database).

Building Construction Activity-Start

In Q3 2025 the value of started building construction projects was HUF 400 billion, around the same value as between April and June. Thanks to the outstanding figures between January and March, the value of building construction projects entering construction phase exceeded HUF 1,500 billion, only 4 points short of the same period in 2023 and 2024. At constant price, Activity-Start between January and September of this year was the lowest in the past 9 years.

Activity-Start of EBI Construction Activity Report in multi-unit housing construction, although greatly sank, stayed at a high level, with the total value of projects started in Q3 2025 exceeding HUF 170 billion. The situation was the opposite in non-residential construction. The segment recovered somewhat between July and September from the previous quarter’s low point, but projects still entered construction at a low value: Activity-Start was around HUF 230 billion. Since 2017 non-residential construction projects haven’t started at a lower value than in the first 9 months of this year.

The largest non-residential projects entering construction in Q3 2025 included MCC’s talent centre in Miskolc, BYD’s electric bus assembly plant in Komárom, Panattoni Logistics Park Building A in Mosonmagyaróvár, IGPark automotive parts manufacturing hall in Nyíregyháza, Phase 2 of Weerts Ebes logistics centre, and MVM Neuron headquarters office building in the 3rd district of Budapest.

Civil engineering Activity-Start

Civil Engineering Activity-Start of EBI Construction Activity Report registered a surge in Q3 2025 due to M1 motorway expansion (M0-Concó rest area). Outside road construction, the value of construction projects started in other civil engineering segments was moderate. While total Civil Engineering Activity-Start exceeded HUF 760 billion, the value of non-road and railway projects started was only around HUF 50 billion in Q3. In addition to the two phases of M1 motorway expansion, only Phase 7 of the closure of the Gyöngyösoroszi ore mine could make it to the list of the biggest started civil engineering projects.

Budapest on top among regions

In the past four quarters, the highest value of construction projects in Hungary started in Budapest and its share in total Activity-Start was 28%. Central Transdanubia also had a large share of 23%. 39% of projects started in Western Hungary, 38% in Central Hungary, while Eastern Hungary’s share was 23%.

Still high multi-unit housing Activity-Start

Although Q3 2025 was the second consecutive year to see a significant drop in the value of started multi-unit housing construction works, Activity-Start stayed high, far exceeding the average of recent years. At current price, multi-unit housing construction works started at an over HUF 170 billion, the fourth highest value after the first two quarters of 2025 and the last quarter of 2024. Overall, the successful first 9 months of this year brought a huge jump in multi-unit housing Activity-Start at current price, but it was also outstanding at constant price, only surpassed by the same period in 2017 in the last 10 years.

Multi-unit housing construction is likely to remain strong. There was a high number of building permits issued in the first three quarters of this year, meaning plenty of projects to get started. In Q3 2025 permitting was boosted by the preferential loan program dubbed Otthon Start available since September which could continue to have a positive impact on the number of homes under construction.

In Q3 this year, multi-unit homes worth around HUF 80 billion were completed at current price, while in the first 9 months, multi-unit housing Activity-Completion was well over HUF 200 billion, only slightly lower than in the same period in 2023-2024.

Looking at the past 4 quarters, Budapest continued to have a major share in multi-unit constructions entering construction (73%). Central Hungary had a 76%, while Western Hungary and Eastern Hungary had a share of 12% each.

Still weak Activity-Start in industrial buildings and warehouses

Industrial buildings and warehouses thrived between 2022 and 2024 when construction works worth between HUF 700 billion and 1,000 billion started annually. For example, construction started on several BMW plants around Debrecen, on Mercedes-Benz projects in Kecskemét, and on several battery factories. This year has seen a decline so far and the value of projects started during three months in Q2-Q3 2025 has been the lowest since 2021. Overall, in the first 9 months of 2025, Activity-Start in industrial buildings and warehouses was around HUF 400 billion, 37% lower than in the same period of 2024, and 29%-39% lower than the 2022-2023 values. Trends are similar at constant price: the period of 2021-2023 was exceptionally good for industrial buildings and warehouses, while there was a strong decline in 2025. In the last 10 years, Activity-Start at constant price in the first 9 months has not been so low as now.

The biggest projects started between January and September 2025 were CTP’s logistics halls in Biatorbágy and Vecsés, HelloParks’ logistics hall in Fót and BYD’s projects in Szeged and Komárom. Construction of Phase 1 of Halms automotive parts manufacturing plant in Miskolc and Panattoni Logistics Park Building A in Mosonmagyaróvár also started.

Activity-Completion was relatively high in all three quarters of 2025 as several projects that started in 2022-2024 reached completion. The value of projects completed since the beginning of 2025 neared HUF 700 billion. For example, this year saw the completion of CATL warehouse and metalworking plant in Debrecen and its surroundings, two BMW factories, and the hangar complex of the Helicopter Base in Szolnok. And Activity-Completion may also remain high in the last quarter of this year.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

On a quarterly level, the value of started construction projects in the second quarter of this year has been the second lowest since 2020 and the Activity-Start of EBI Construction Activity Report Hungary at current price did not reach HUF 470 billion. In the first half of the year, projects entering construction phase were worth around HUF 1,200 billion, far below the previous years and close to H1 2020 when the pandemic hit.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). Inquiry and price offer for the report.

Building construction performed poorly in Q2 2025

In Q2 2025 the value of building construction starts fell below HUF 400 billion, barely reaching half of the Activity-Start of Q1. After 2020 it was only in Q3 2024 when the value of construction starts was at a similarly low level. The decline in building construction was even more pronounced at constant price: Activity-Start of EBI Construction Activity Report at constant price was last lower in Q1 2015 than in Q2 this year.

Such a poor performance in building construction occurred despite the extremely successful quarter in multi-unit housing construction. The Activity-Start for non-residential construction fell to a critically low level not seen since Q1 2015, below HUF 120 billion. At constant price, the decline is even more drastic, the value in Q2 2025 was less than half of the previous negative record.

The largest building construction projects during Q2 2025 were mostly multi-unit housing ones. Only one non-residential project made it to the list of the biggest projects, Phase 1 of Halms automotive parts manufacturing plant in Miskolc.

Better Civil Engineering Activity-Start, but still at a low level

Q2 2025 saw an improvement over Q1 in Civil Engineering Activity-Start of EBI Construction Activity Report, but projects started only at a value of around HUF 100 billion. In the road and railway construction segment, there was an increase in Q2 2025 against Q1 with projects entering construction phase on HUF 50 billion, a level not considered high.

The biggest civil engineering projects launched in Q2 2025 include the railway infrastructure of the Ivancsa industrial-innovation development area, the XIV/A water shaft in Tatabánya, and the development of the drinking water networks in Ács, Bábolna and Koppánymonostor.

The capital city has the highest share in total Activity-Start

Looking at construction projects launched in the past four quarters, Budapest had the highest value with a share of 34% in total Activity-Start. It still exceeds the 20%-30% typical of the period between 2021 and 2023.

In the previously leading Northern Great Plain, 16% of projects started. The share of Southern Transdanubia was 15%, and that of the Southern Great Plain was 11%. The lowest values were registered in Northern Hungary and Western Transdanubia during the period, with a share of 4% each. In Central Transdanubia and the Pest region, a respective 8% of projects were launched.

Favourable trend continuing in multi-unit housing construction

Q2 2025 far exceeded the average of recent years in terms of the value of construction starts: multi-unit housing constructions started at HUF 250 billion at current price. This is an absolute record, the second highest value after Q1 2025 registered since 2014. Activity-Start of EBI Construction Activity Report in the segment exceeded HUF 200 billion for the third consecutive quarter, way more than the previous highest HUF 144 billion until H1 2024. The expansion was also significant compared to previous years, even when calculated at constant price.

The momentum fuelled so far by maturing government bonds and interest payments may continue this autumn with the launch of the Home Start Program (providing first-time home buyers with a fixed-rate loan of up to HUF 50 million at a 3% interest rate). Also, this autumn, projects financed by the Housing Capital Program this year (a government initiative to help the supply side) may also appear among sold homes. As a result of these, a pick-up in both demand and supply is expected for the rest of the year. In Budapest, the projects of the Housing Capital Program may be the source of a further high level of Activity-Start. In the countryside, more multi-unit housing projects may start due to the livelier demand thanks to the launch of the Home Start Program. In the capital city, the number of available new homes is already at one of the highest levels in recent years because of the previous significant construction starts. This, in addition to the new supply, may make developers more cautious with project launches as the end of the year approaches.

The value of completed multi-unit homes in Q2 2025 was around HUF 90 billion, a slight increase compared to Q1. Overall, Activity-Completion of multi-unit housing constructions slightly dropped in the first half of the year compared to the previous year, remaining roughly at the 2023 level.

Looking at the past four quarters, Budapest has had a massive share in multi-unit housing constructions entering construction phase (75%), while none of the other regions reached 10%. In Central Hungary 77% of such projects started and in Western Hungary 14%, while only 9% of the Activity-Start was registered in Eastern Hungary.

Hotels in focus: the year started off sluggishly for projects, but growth is visible

Hotel construction works boomed in 2019-2020 most, but projects also commenced in 2021 and 2023 at relatively high values. 2024 saw a slight decline, and this year also started rather sluggishly. The second quarter brought some expansion, though; between April and June 2025, the total value of construction starts in the segment was over HUF 20 billion, a major improvement compared to the previous, very weak quarter, and roughly the same as the median for the period between 2023 and 2025. At constant price, we also see that Activity-Start of EBI Construction Activity Report in Q2 2025 does not differ much from previous quarters but is far behind the high values between the end of 2019 and the beginning of 2021. The largest started hotel projects in H1 2025 included Phase 1 of Staybridge Suites Hotel in Budapest and the MCC Talent Development Center project in Miskolc.

Several hotel projects that were launched in previous years have now reached completion. In Q2 2025, Activity-Completion in the segment set a record, approaching HUF 90 billion at current price and exceeding HUF 160 billion at constant price. For example, the 4-star hotel next to the Balaton Park Circuit racetrack and Le Primore Hotel in Hévíz have been completed.

Also, many hotel projects are currently underway which are due for delivery next year, such as the renovation of the Grandhotel Galya in the countryside, and a number of hotels under construction or under renovation in Budapest: Sofitel Budapest Chain Bridge, hotel in Kígyó street, VP36 Boutique Hotel, Paulay Opera Hotel, Hotel Paulay (Puro), Moxy Budapest Downtown by Marriott, and Hilton Garden Inn. Hotel Gellért in the capital city is also undergoing renovation and may be completed in 2027. Klotild Palace St. Regis Hotel and K36 Hotel and Student Hostel are also nearing completion and could open this year.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

2025 started off weak in Hungarian construction despite the much higher Activity-Start at the end of 2024 fuelled by launched major projects then. In Q1 2025 the value of started construction works greatly dropped compared to both the previous quarter and the same period of the previous year. The Activity-Start of EBI Construction Activity Report at current price was around HUF 570 billion in Q1 2025; the second lowest quarterly value since July 2020. At constant price, and if adjusted with price changes, it has been the second worst three-month Activity-Start since 2015.

Value of started building construction works fuelled by multi-unit residential projects

Building construction has slightly improved compared to the previous two weaker quarters: the value of started works was well over HUF 500 billion, 18% up from Q4 2024. The improvement, which was also evident at constant price compared to H2 2024, was attributable to the surge in multi-unit residential works. At the same time, Non-Residential Activity-Start continued to see the low levels of the last two quarters of 2024. In the first three months of this year, non-residential construction works of slightly more than HUF 240 billion started, the lowest quarterly figure since 2017. At constant price, no building construction works have started in such a low quarterly value in the past 10 years.

Among biggest building projects launched in Q1 2025 were mainly logistics buildings: CTP logistics halls in Vecsés (Phase 2) and Biatorbágy, and HelloParks logistics hall in Fót. Construction also began on Phase 2 of Building A of H2Offices in Budapest, and the Hungerit poultry processing plant in Szentes.

Critically low value of started civil engineering projects

Civil Engineering Activity-Start was extremely low in Q1 2025 with started construction works worth only HUF 31 billion. This has by no means been the lowest value recorded in the subsector since 2014, both at current and constant prices. Activity-Start in road and railways and in non-road and non-railways amounted to around HUF 16 billion, respectively. Sadly, not a single civil engineering project made it into the largest projects entering construction phase in the quarter.

Regional comparison: Budapest on the lead

According to EBI Construction Activity Report, Budapest had the highest value of construction projects started in Hungary in the last four quarters. And although its share in total Activity-Start slightly dropped, it still stood at 32%, exceeding the 20%-30% typical in the period between 2021 and 2023.

In Northern Great Plain, the region that previously was on the lead, 14% of projects started in Q1 2025. The share of Southern Transdanubia was 16%, while that of Southern Great Plain 11%. Western Transdanubia and Northern Hungary registered the lowest value at 5%, respectively. In Central Transdanubia, 7% of projects started, whereas in the Pest region, 10%.

Multi-unit residential projects shooting up

The latest EBI Construction Activity Report Hungary has found that 2025 started off greatly in the multi-unit residential segment as in the first three months the value of construction starts was almost HUF 300 billion at current price. It has been a record since 2014 and exceeds the previous quarter’s highest value (HUF 209 billion). Even at constant price, the growth in Activity-Start is a 39% rise over the previous quarter.

This increased activity comes as no surprise: the last quarter of last year already witnessed recovery with developers responding to growing demand and preparing for increased interest at the beginning of this year.

The market has confirmed these expectations, and as per ELTINGA’s Housing Market Report, the latest two quarters saw a record in Budapest in the number of sold new multi-unit dwellings. Although a major part of demand came from investors, the question is how long this can last. Developers might become more cautious with project starts towards the end of the year as demand might decrease following interest payments and maturing government bonds.

When it comes to completions, the value of completed multi-unit residential projects in Q1 2025 was around HUF 76 billion, a drop compared to both the previous quarter and the same period last year. At constant price, Activity-Completion in Q1 2025 has been the third worst value since 2019.

Regionally, looking at the past four quarters, Budapest accounted for 70% of multi-unit projects entering construction, while Central Hungary recorded slightly more than 72% of the value of such projects. Eastern Hungary had a 13%, while Western Hungary had a 16% share in Activity-Start.

Better Q1 2025 in industrial buildings and warehouses than in the construction industry as a whole

In Q1 2025 the total value of construction starts of industrial buildings and warehouseswithover HUF 150 billion was slightly higher than in the previous two quarters. True, if we look at the period between 2022 and H1 2024, it was the second lowest value. Last year, in addition to automotive industry projects, several food industry projects started such as Pick’s plant in Szeged, Master Good-Sága plant in Sárvár, or Félegyházi Bakery plant and warehouse in Kiskunfélegyháza.

In the first quarter of this year, as previously mentioned, the largest projects entering construction phase included several logistics projects such as CTP’s logistics halls in Biatorbágy and Vecsés, and HelloParks’ project in Fót. Besides, the construction of several plants began: Unilever’s deodorant factory in Nyírbátor, Phase 2 of Scheider Electric’s Duna Smart Power Systems smart factory in Dunavecse, or Kométa’s packaging plant in Kaposvár.

As for completions in the segment, industrial buildings and warehouses were completed at a value of HUF 250 billion in the first quarter of this year – the third highest value since 2014. Biggest completed industrial projects include CATL warehouse and metalworking plant in Debrecen and HelloParks AN1 logistics hall in Alsónémedi. And we expect to see further major completions this year.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To purchase the report, ask for a quote

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

The Activity-Start of the latest EBI Construction Activity Report surpassed HUF 830 billion, a value considered to be exceptionally high. It should be added though, that these outstanding numbers were mostly thanks to the start of the construction works of the Mohács Danube Bridge project.

Despite the weaker Q2 and Q3, thanks to the good Q4, in the whole 2024 started construction works totalled about HUF 2800 billion, almost the same level as in 2023. Yet, it was a significant lag compared to the 2021-2022 figures, and at constant price it was still the lowest Activity-Start of recent years. Last time we saw a lower value of construction start than the 2024 level was in 2016.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). For purchasing the full report, please write to us.

Multi-unit residential projects boosting building construction

Building construction projects worth a total of around HUF 500 billion were launched between October and December last year. For the whole of 2024, the value of building projects entering construction phase was nearly HUF 2000 billion. Yet, last year’s Activity-Start fell short of the yearly figures for 2021-2023; the difference compared to 2023 was 5.9%, while compared to 2022 and 2021 it was 15% and 13%, respectively. At constant price, the last time a value lower than in 2024 was recorded was in 2015.

The reason for the better Building Construction Activity-Start in Q4 was clearly the multi-unit residential segment that posted a record growth over previous quarters. Activity-Start in the non-residential segment was low in Q4, though, almost the same as in Q3 (just over HUF 200 billion), still a very modest level compared to the quarterly figures of previous years. At constant price, Non-residential Activity-Start has not been as low in the past 11 years as in Q4 2024. Looking at the whole of 2024, construction works started here on slightly more than HUF 1,300 billion at current price, the lowest value since 2021. At constant price, the last time Non-residential Activity-Start was lower than last year was in 2014.

The biggest building construction projects that started in Q1 2024 included many multi-unit residential ones such as several phases of Kincsem by Bayer, the next phases of Park West and City Pearl. Also, the highest-value projects comprised the start of construction of several industrial and logistics buildings (Waberer’s logistics centre in Ecser, Phoenix Pharma logistics warehouse and office in Győr, the production facility of Félegyházi Bakery in Kiskunfélegyháza, Fémalk’s industrial plant in Dunavarsány and Phase 4 of Hankook tire factory in Rácalmás).

Civil engineering posted a good last quarter last year

In Q4 2024 civil engineering works worth more than HUF 330 billion started, approaching the exceptionally high value registered in Q1. Thus, overall, the level of Civil Engineering Activity-Start of EBI Construction Activity Report in 2024 exceeded HUF 800 billion, more than the 2023 figure and nearing the 2021 value. True, almost the entire Q4 Civil Engineering Activity-Start was due to the start of the Mohács Danube Bridge project.

Around half of the Activity-Start in Q4 2024 was related to road and railway projects with their level roughly being the same as in Q1. The situation was similar in case of non-road and non-railway construction works. The weak numbers in the middle of the year were followed by a larger number of construction starts in the last three months of the year. Yet, looking at the whole of 2024, projects worth less than HUF 400 billion entered construction in roads and railways, not even reaching the level recorded in 2023. At constant price, the last time Activity-Start was lower than last year was in 2015.

Most projects started in Central Hungary

Looking at the past 4 quarters, roughly half of the projects started in Central Hungary. Within, nearly 40% of the works started in Budapest. Eastern Hungary had a 23%, while Western Hungary had a 26% share in Activity-Start. Among the regions, thanks to the Mohács Danube Bridge project, the share of Southern Transdanubia spiked (14% after the previous 5%). The share of Northern Great Plain dropped; it was only 9% against the previous double-digit rates.

Multi-unit housing construction has picked up

In Q4 2024 multi-unit housing construction works practically exploded. The value of started works reached nearly HUF 300 billion, almost doubling the previous record of Activity-Start of EBI Construction Activity Report. Thanks to the outstanding last three months, 2024 was ultimately a record year with the value of started multi-unit construction works surpassing HUF 600 billion. It outnumbered the Activity-Start of 2023 by 66% and represented a growth of about 45% at current price over 2021 and 2022. At constant price, the value of multi-unit construction starts in 2024 was higher than in 2023 and 2022, roughly the same as in 2019 and 2021.

The acceleration in multi-unit housing constructions in Q4 2024 comes as no surprise. Developers may have responded to the pick-up in demand already noticeable last year, plus, they may have prepared for an even greater increase in demand this year – in line with market expectations. Subsidies in 2025 (maturing government bonds and interest payments, private pension fund savings that can only be used for housing purposes this year) may considerably spur the willingness to buy a home this year.

As for completions in the multi-unit segment, construction works of about HUF 400 billion were completed in 2024, exceeding the Activity-Completion indicator of EBI Construction Activity Report of the previous three years. Last year’s multi-unit residential completions were the second highest value registered after 2020.

Regionally, most multi-unit residential projects still started in Budapest, accounting for more than 70% of the value of construction starts in 2024, compared to the previous figure of under 60%. However, Eastern and Western Hungary posted a major decrease and had shares of 10% and 18%, respectively.

Weak H2 2024 in the value of started office construction projects

Activity-Start in office constructions fell sharply between July and December last year with works worth less than HUF 20 billion. Although H1 2024 managed to reach the figures of H1 2022 and H1 2023, overall, there was a large drop in 2024. The value of Activity-Start of EBI Construction Activity Report did not reach HUF 130 billion in 2024. This was a 24% decline compared to 2022, while a 68% and 66% lag behind the outstandingly successful years of 2023 and 2021. After 2015, even at current price, only in 2020 did office projects start in a lower value than last year. At constant price, the office market had not registered such a low Activity-Start as in 2024 in the past 11 years.

The start of MBH Bankholding HQ and the central office next to Rossmann warehouse was the two office construction projects with the biggest value last year. The decline in market-based office projects has not started now. Rather, in recent years, state orders have been able to enable growth in the segment. For instance, the fact that the overhaul of the former Ministry of Finance building in the Buda Castle, the historic reconstruction of the Hungarian National Bank HQ and Phases 1-3 of the reconstruction of the former Palace of Archduke Joseph all started at the same time in 2021 boosted Activity-Start that year. Or, in 2023, the start of renovation works on the Ministry of Agriculture building and on the Palace of Justice building, as well as the start of construction of the BudaPart and Zugló City Centre offices all contributed to high Activity-Start that year. A large part of these will also house state agencies and companies.

When it comes to office completions in 2024, the Activity-Completion indicator was nearing HUF 300 billion, the highest value ever measured in the market. For example, the Hungarian National Bank HQ and the reconstruction of the Ministry of Finance building both reached completion. 2025 may be another record-breaking year in terms of office completions as several office buildings in BudaPart and Zugló City Centre may also be completed.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

According to the Q3 2024 EBI Construction Activity Report Hungary, after Q2 brought a decline in the value of started construction projects, in Q3 a further decrease followed. Since 2016, the Activity-Start of less than HUF 360bln between July and September has been a new negative record, even at current price.These weak numbers were not even offset by the better Q1 and Activity-Start accounted for slightly more than HUF 1800bln. The value of projects entering construction between January and September 2024 was nearly 17% lower than in the same period of 2023.

Photo by Hajnalka Hurta

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). For purchasing the full report, please write to us.

Shrinking Building Construction Activity-Start

Q3 saw a continued decline in Building Construction Activity-Start with only HUF 310bln worth of started works. Except for the pandemic year of 2020, only 2017 and earlier years saw lower quarterly numbers. Looking at the first 9 months of this year, the value of started construction works was slightly less than HUF 1360bln, 15%-22% lower than in the same period of 2021-2023. At constant price, the drop was even more considerable: since 2014 there has not been a lower Activity-Start in the first three quarters than this year.

Multi-unit housing constructions posted a slight decrease in Activity-Start in Q3, but non-residential projects registered a larger drop with only HUF 200bln worth of projects entering construction phase between July and September. In the first 9 months, the Activity-Start of non-residential constructions was around HUF 1000bln, 21%-27% lower at current price than in the same period of 2021-2023. At constant price, the last time the number for the first three quarters was lower than this year’s was in 2014.

The largest construction projects launched between July and September 2024 included Lidl’s logistics center in Kiskunfélegyháza, HelloParks Páty PT5 logistics hall, Pick’s production plant in Szeged, Intretech’s plant in Kapuvár, Rheinmetall’s hydrogen and e-mobility parts production plant in Szeged and IGPark’s logistics hall in Debrecen. The construction of the hotel in Kígyó street in Budapest also started. Out of the 10 biggest projects in the quarter, 5 were multi-unit residential buildings or dormitories.

Civil engineering Activity-Start hits rock bottom

There was a further decline in civil engineering after Q2, Activity-Start in Q3 was only less than HUF 50bln – a new negative record of the last 8 years. But in terms of Activity-Start in the first 9 months, the 2024 result is not much better either. The value of construction works started in the first three quarters at current price has not been lower than this year since 2016, while at constant price it was the negative peak of the last 10 years.

Compared to the same period in 2021 and 2023, Activity-Start between January and September this year was 22%-24% lower, while it was only a little more than a third of the exceptionally high 2022.

Within civil engineering, only a negligible railway construction project started in Q3, and the value of road construction projects was also very low. In the first three quarters, road and railway construction accounted for roughly 45% in Activity-Start, their value slightly exceeding HUF 200bln.

Due to the rather low civil engineering activity, hardly any civil engineering project could get into the list of biggest projects. Only the wastewater projects in Dejtár agglomeration and the Rétság agglomeration are worth mentioning.

Budapest leads still

Looking at the last 4 quarters, 39% of all started construction works were in Budapest. The second largest Activity-Start was characterized by the Northern Great Plain (14%), followed by the Southern Great Plain and Pest County (12%). Northern Hungary and Southern Transdanubia recorded the lowest value of started construction works with their respective share of around 5%.

Multi-unit construction works are keeping up

Even though somewhat fewer multi-unit housing constructions started in Q3 than in Q2, Activity-Start significantly exceeded Q1. Construction works started in the segment on slightly more than HUF 100bln. Looking at the first 9 months of the year, there was an overall higher Activity-Start at current price than in the same period of 2019-2023. The value of projects entering construction was roughly the same as in the same period of 2022. At constant price, the Activity-Start for the first 9 months of this year outstripped the first three quarters of 2023; yet it was the second lowest since 2016.

This suggests that developers are still cautious with project starts even though this year’s demand for new homes increased compared to last year’s. Based on housing market trends, supply is expected to grow. A strengthening demand and rising prices may encourage more investors to start projects, and thus Activity-Start in multi-unit construction works may also increase in the future.

In Q3 the value of completed multi-unit housing buildings continued to drop, barely surpassing HUF 60bln. At the same time, in the first 9 months, approximately HUF 265bln worth of such buildings were completed, a slight rise over the same period last year. For the time being, a larger volume of homes is expected to reach completion in the last quarter, however, due to project delays, some may only be completed next year.

The biggest share of multi-unit residential constructions still started in Budapest. Based on the data of the last 4 quarters, the share of the capital city was around 60%. Eastern Hungary accounted for 14% of the Activity-Start, while Western Hungary for 24.5%, up from the previous quarters.

Central Transdanubia

Activity-Start in Central Transdanubia was roughly HUF 40bln in all three quarters this year. Thus, in the first 9 months, construction projects started at a total of HUF 123bln, a major drop compared to the same period of previous years. In the first 3 quarters of 2023, Activity-Start in the region was almost HUF 200bln, while in the first 3 quarters of 2022, it reached around HUF 300bln.

After the weaker Q1, Activity-Start for building constructions in Central Transdanubia in Q2-Q3 was roughly at last year’s levels. Thus, overall, the value of projects entering construction was around HUF 100bln in the first 9 months of this year, lower than in the corresponding period in 2023, and particularly lower than in the same period of 2021-2022.

The outstanding building construction Activity of 2021-2022 was boosted by the start of several big-league projects in 2021 (SK On’s battery factory in Iváncsa, Alba Aréna multifunctional hall in Székesfehérvár) and in 2022 (Kovács Katalin National Kayak-Canoe Sports Academy, the renovation of the church buildings in the castle quarter of Veszprém).

Projects entering construction phase between January and September 2024 in the region included the Huayou Cobalt-Bamo cathode factory in Ács and Phase 3 of Campus Lane Condo in Székesfehérvár.

In the first 9 months of 2024, hardly any civil engineering projects started in Central Transdanubia and the value of started works only reached a bit more than HUF 20bln. Among major civil engineering projects this year only Phase 1 of the dam between Mária-Valéria Bridge and Prímás island ramp can be mentioned. Last year bigger-value civil engineering projects started in the region in Q3 and Q4, for example, several water utility or wastewater projects, and the Biatorbágy-Szárliget railway line.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)