EECFA’s 2026 Summer construction forecast up to 2028 was released on 22 June. Sample report can be viewed at eecfa.com. To obtain the new reports, please contact us

Southeast European construction markets up to 2028

Bulgaria stepped into this year as the 21st member state of the eurozone in the middle of an evolving political turbulence that inevitably impacted the construction sector, most notably, projects that rely on public funding. Nevertheless, according to Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian member institute, Bulgaria’s total construction output is anticipated to increase by approximately 2% on average in the forecast period of 2026-2028. He also notes that “Last year Bulgaria’s construction sector excelled with a strong performance, largely thanks to the residential and non-residential submarkets which fared better than previously predicted. In 2026-2028, however, the country’s total construction output could see a heterogeneous performance.”

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s members for Croatia, point to funding from the EU’s Military Mobility Package (MMP) as a promising source of finance for a wide variety of Croatian construction projects. Transportation ones, both straightforwardly military and dual use, are obvious contenders, so the availability of MMP money should lift output in those civil engineering segments. MMP will likely boost some non-residential segments, too, since it can finance, e.g., factories and logistics centers (perhaps even flight schools?) that have a military or dual-use purpose. This will help sustain total construction output despite rapidly declining levels of finance under the EU’s post-2022-earthquake rebuilding programs and RRF. In non-residential generally, while some developments will affect all segments, specific factors will ensure that output growth varies greatly from segment to segment. The picture for energy construction is also confused, with solid, well-known technologies competing with much-hyped, as-yet-unproven, “hi-tech” alternatives. Residential is buffeted by the conflicting influences of rising prices, declining GDP growth and interventions by the central bank and the government.

Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild, notes that Romania’s construction market is still in a tight spot. “Growth potential is limited with global and national factors conspiring against it. Recent economic forecasts are more pessimistic; 2026 might see a stagnant GDP, declining real wages and the highest inflation in the EU. This is coupled with the looming specter of national deficit causing high taxation and austerity measures: lower public spending, and wage and hiring freezes for public employees. Not to mention that construction costs, which started evening out in 2025 after the 2022 shock, are now again on the rise due to climbing energy prices and labor costs. The saving grace of construction is the EU programs funding infrastructure projects. Yet, with the NRRP running out in mid-2026, and other programs having an inconsistent performance, the boost they can provide is limited. Adding to all this is a political crisis that could lead to a government change at a critical moment (the end of NRRP absorption, projects phased into other funding sources). But the silver lining: most of these issues should be transitory. By 2028 Romania’s construction might return to growth on the back of improved economic indicators, inflation levels within the target range, a more efficient energy sector, and hopefully, a more stable political situation.”

“Serbia’s overall construction output is still consolidating in 2026 led by the correction in civil engineering, while buildings continue to grow in this forecast” – according to Dejan Krajinović, EECFA’s Serbian researcher at Beobuild. He adds that the performance in the residential submarket remains stable and is predicted to continue to grow with moderate growth rates. Non-residential, on the other hand, is booming, driven by massive investments related to the EXPO 2027, with another year of double-digit growth expected in 2026. Main segments benefiting from ongoing developments are office, commercial and hotel, but health-related construction is also breaking records in 2026. The consolidation in civil engineering is anticipated to end in 2027, with new growth on the horizon in 2028 and onwards. The large-scale infrastructure projects in the pipeline should launch a next big growth cycle in overall outputs. However, the war in the Middle East is already pushing construction costs up and the economic uncertainty and fragmentation are still risks that continue to linger in the coming period.”

“Slovenia’s construction sector’s output was holding steady at just under €6bn in 2024 and 2025 but is set to edge higher in the forecast period, supported mainly by public spending” – says Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia. “Growth is increasingly uneven: residential construction remains constrained by limited supply and rising costs despite strong demand, while private non-residential segments such as offices, retail and industry face cautious investors and only modest expansion. By contrast, publicly financed segments, notably education, health and civil engineering renovation, are providing stability, with infrastructure upgrades, railway investment and energy-transition projects sustaining activity. Transport and utility constructions are shifting from large expansions to maintenance and modernisation, and investment in electricity networks and pipelines is set to rise further due to the energy transition. Overall, the sector is moving into a more stable but slower phase where public policy and infrastructure spending play a decisive role in keeping output on track – as long as public financing remains available.”

Eastern European construction markets up to 2028

According to Andrey Vakulenko at Macon, EECFA’s Russian research institute, the downward trend in Russia’s construction market, which began in 2025, is likely to continue and intensify in 2026–2027. The main reason behind is the combination of a decelerating economy and a prolonged period of high interest rates, which negatively impacts demand, limits the availability of financing and restrains investment activity. Residential construction is experiencing the strongest pressure as the market struggles to find a new balance amid reduced mortgage availability, declining demand and decrease in new construction. Most non-residential segments may also show negative dynamics in the coming years impacted by the slowdown in consumption volumes and business activity, weak household income growth and changes in the direction and scope of government funding in certain segments. Civil engineering will likely stay the most resilient subsector due to the implementation of major transport and energy projects. The planned acceleration of infrastructure construction, the expected growth in the residential submarket and the easing of monetary policy are the conditions for the construction market to return to a growth trajectory in 2028.

“In Türkiye, state involvement in housing development has grown in recent years” – say Prof. Ali Türel and Prof. Leyla Alkan Gökler, EECFA’s Turkish researchers. “Policies to curb inflation have depressed households’ disposable income, creating a serious housing affordability issue for both ownership and renting as home prices and rents have spiked. As moderate-to lower-income households have found it increasingly difficult to accumulate sufficient equity for home purchases, the government has intervened. It launched a large number of residential projects for dwellings that can be bought on affordable terms by households not owning a house in Türkiye. Dwellings will be built by the Housing Development Administration (HDA), the key state actor in housing production in Türkiye. Since HDA has also been involved in rebuilding the about 550,000 dwellings damaged in the February 2023 quake, the share of housing built by the public sector has greatly risen in recent years, while the share of the private sector has been declining from its former share of about 90%. Our latest forecast indicates that total construction output in Türkiye may reach nearly 8 trillion TL (nearly EUR 180 billion) in 2028, at 2025 prices.”

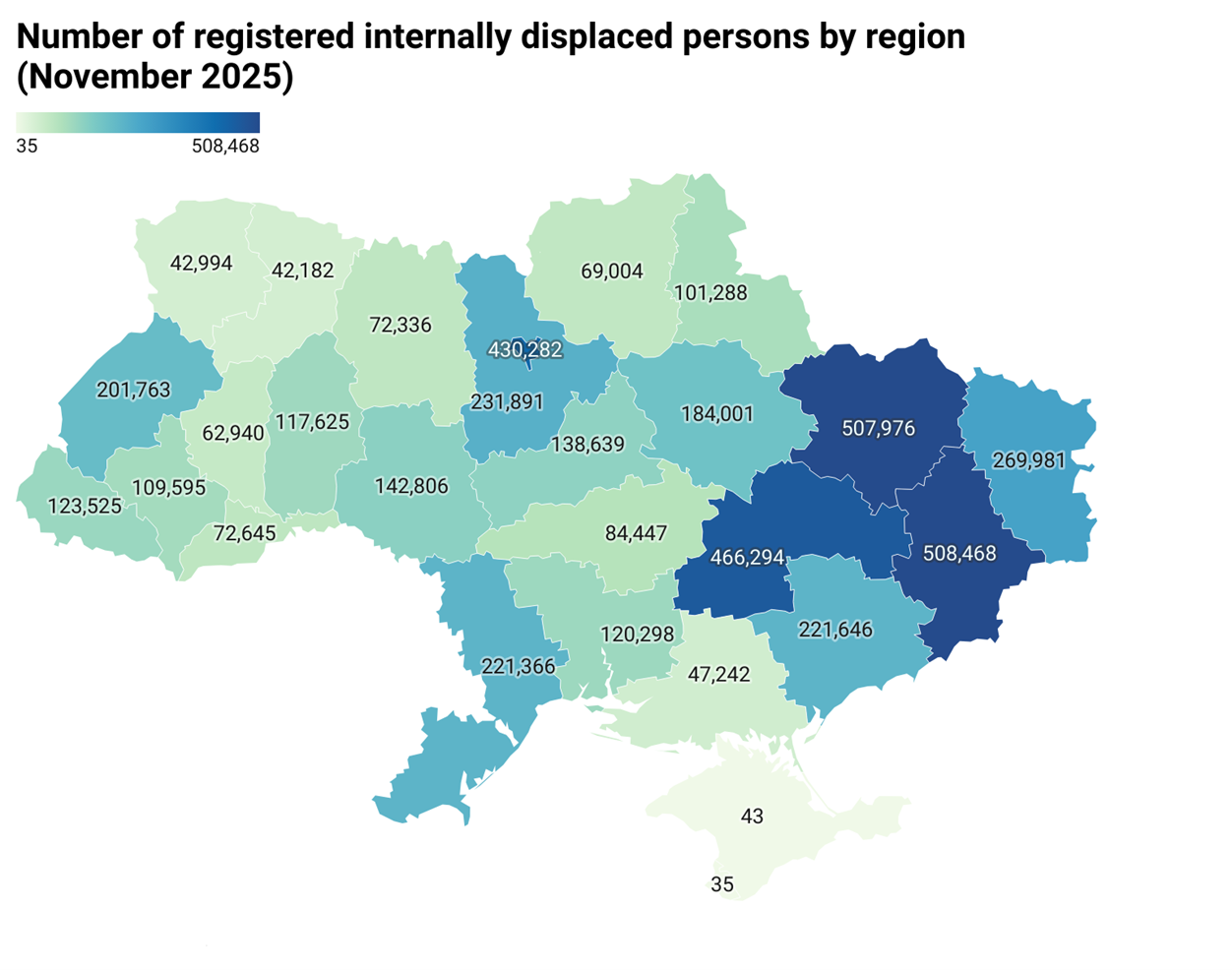

“Ukraine’s construction market exhibited high resilience in 2025 despite the ongoing war and challenging security conditions. While it is recovering and it nominally returned to pre-war levels last year, it was still 40% below the 2021 output at comparable prices.” – notes Professor Sergii Zapototskyi at Uvecon, EECFA Ukraine. “Key growth drivers were commercial, industrial, warehouse, and logistics developments, an uptick in residential construction in relatively safe regions, and large-scale projects aimed to restore public and transport infrastructure. In the coming years, the construction market is expected to continue to grow, supported by post-war reconstruction needs, government housing support programs, and an increase in international funding for Ukraine’s recovery. The greatest growth potential will remain in residential, commercial, as well as industrial and warehousing construction. At the same time, the future performance of the market will largely depend on the security situation, the availability of investment resources, the ability to address labour shortages, and the effectiveness of government reconstruction policies.”