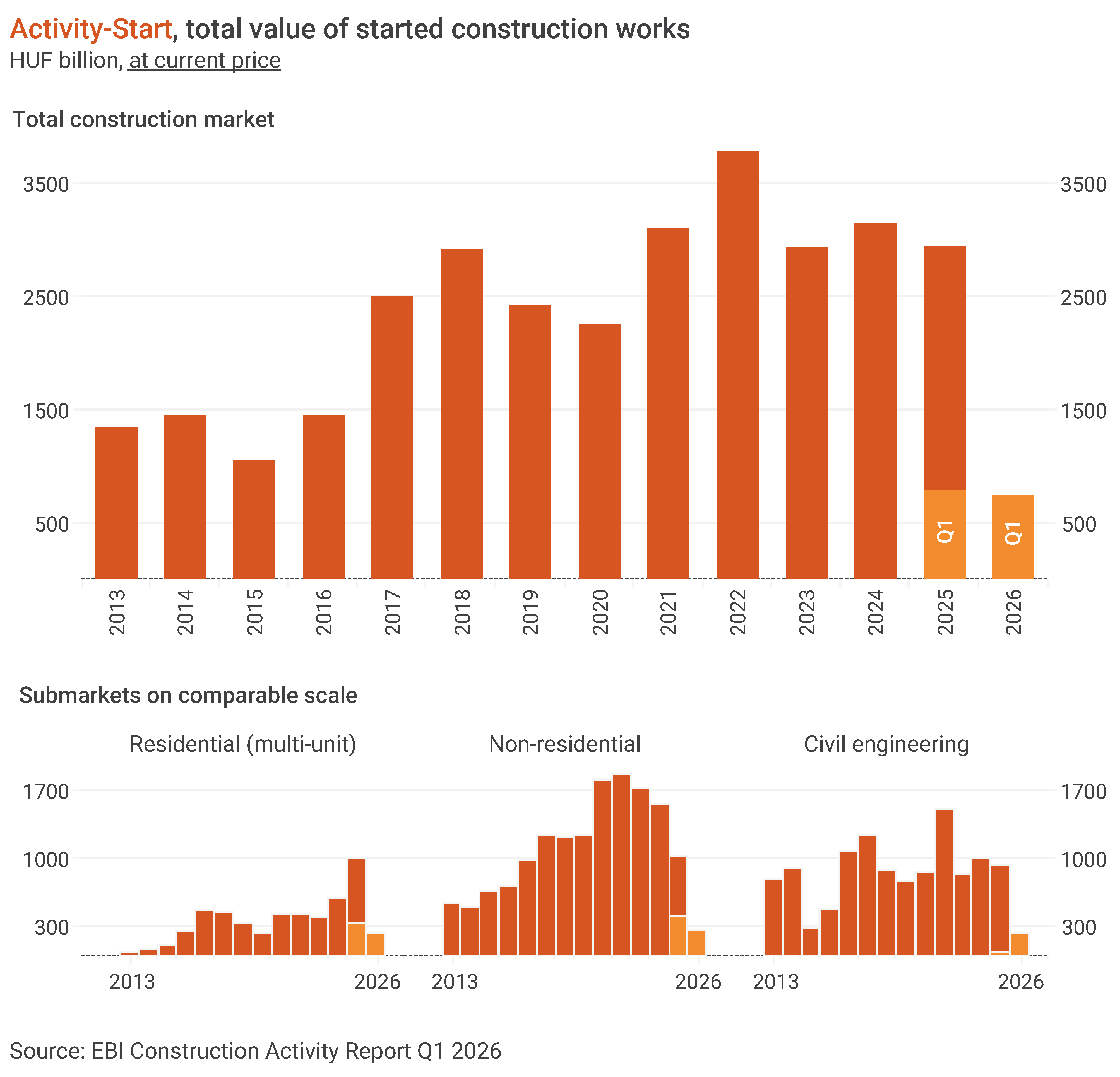

As per the latest EBI Construction Activity Report, 2026 did not start badly in Hungary for construction. Activity-Start in Q1 did not substantially lag behind Q1 2025 and Q1 2023, in fact, it slightly exceeded the average quarterly values of these years. At the same time, the start of foundation works of Block 5 of Paks 2 nuclear plant played a major role in higher numbers, adding a more nuanced picture. Projects worth around HUF 740 billion entered construction in Q1 2026. At constant price, Activity-Start did not lag greatly behind the same period of 2025 (-9%), but we have still seen the weakest first three months since 2016.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To obtain the report, please contact us.

Building construction returns to last year’s level

2026 started much weaker in building construction than last year, but the Activity-Start of around HUF 500 billion was roughly in line with the average quarterly level of 2025 and was only 6% below the average quarterly value of 2024. Hence, no major decline compared to the previous two years at current price. Even at constant price, the value of construction projects started in the first three months was close to the average quarterly level of last year, but it was double-digit below the average three-month Activity-Start between 2016 and 2024.

Multi-unit housing construction is still the segment keeping building construction at a higher level. Activity-Start for non-residential construction between January and March this year (HUF 263 billion) exceeded the average quarterly value of 2025, which was considered weak, but fell 33-44% short of the average values between 2021 and 2024. At constant price, this year’s first-quarter Activity-Start has been one of the weakest since 2015.

Biggest started non-residential projects in Q1 2026 comprised several logistics and office buildings such as Phase 3 of Láng-negyed V1 office building and Frontiers Campus office and research centre in Budapest, and the renovation of BorsodChem offices in Kazincbarcika, Phase 3 of CTP VCS5 Logistics Centre in Vecsés, building D of VGP Park Beta logistics centre in Győr, building B of Panattoni Logistics Park in Mosonmagyaróvár, and Phase 1 of Penny Market logistics centre cold storage in Alsónémedi.

Paks 2 boosted civil engineering figures

In Q1 2026, the value of started civil engineering works neared HUF 240 billion boosted by the start of foundation works of Block 5 of Paks 2 nuclear plant, while the Activity-Start in road and railway projects was only HUF 20 billion. Apart from Paks 2, only one civil engineering project got into the largest projects in Q1 2026: the construction of Phase 2 of the industrial park in Nyíregyháza.

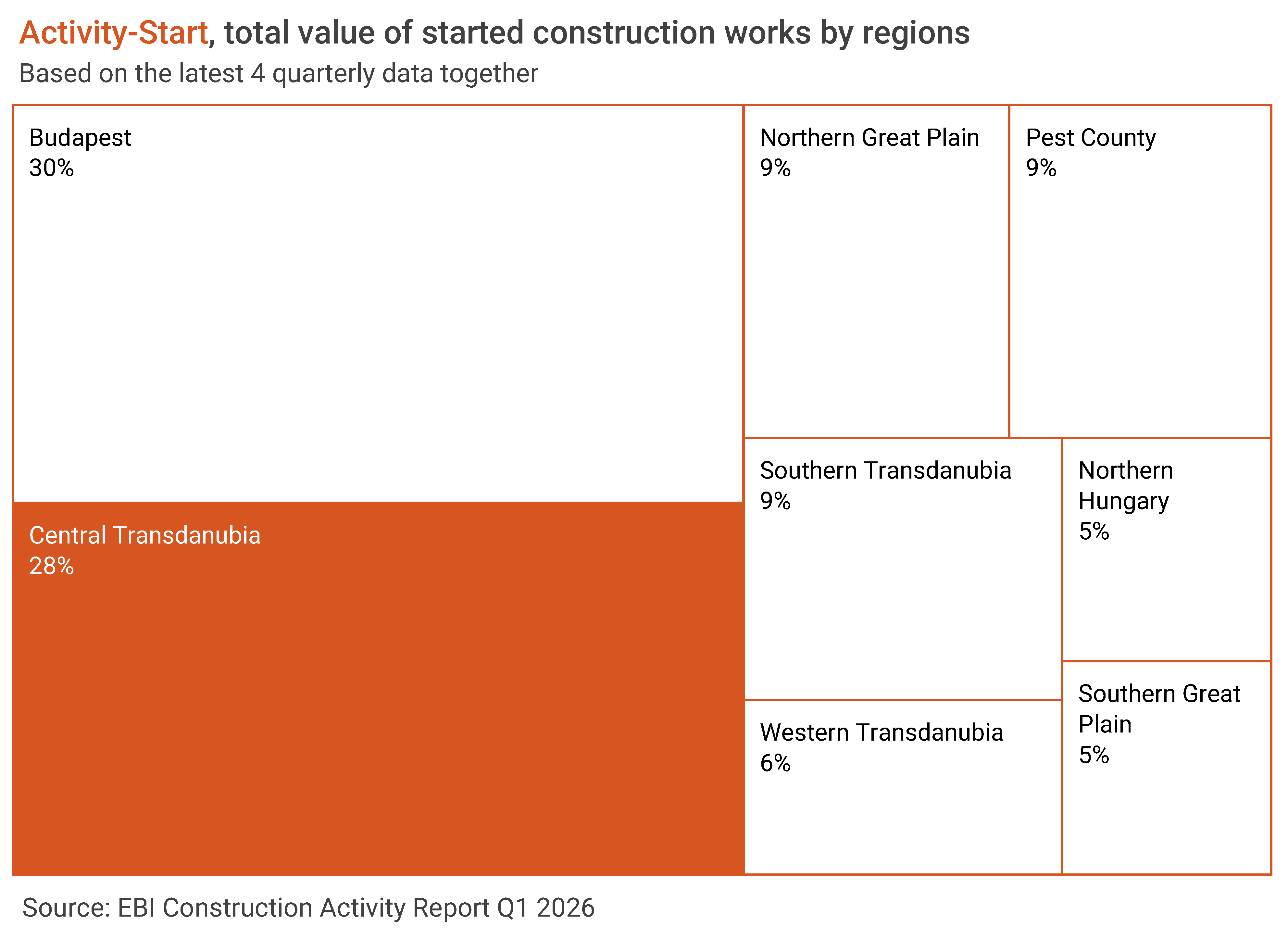

Budapest: regional heavyweight again

Budapest continued to be the region with the highest value of construction works started in Hungary with a share of 30% in total Activity-Start in Q1 2026. Based on the four-quarter moving averages, the share of Central Transdanubia was still considerably higher than in previous years thanks to the M1 motorway expansion launched in Q3 2025. Pest County, Southern Transdanubia and the Northern Great Plain accounted for about 9% of started constructions, while the share of other regions varied between 5% and 6%.

Multi-unit home construction still high

After a weaker final quarter last year, this year started with an extremely strong first three months for multi-unit housing. Between January and March, the value of started construction works exceeded HUF 240 billion at current price; the third highest quarterly Activity-Start since 2014. This value is significant even at constant price: only 2017-2018 and last year had stronger quarters.

The great increase in permits last year suggested strong activity at the beginning of this year. The latest EBI Construction Activity Report has found that many large projects have moved closer to planned start recently, also predicting a higher Q2 Activity-Start in the segment. However, there is a lot of uncertainty in the market now as projects within the Otthon Start Program are expected to be reviewed, which may change developers’ plans.

In Q1 2026 the value of completed multi-unit building was about HUF 83 billion, still considered a moderate level. At constant price, it is particularly low. But it comes as no surprise as previous years were characterized by restrained project launches, and the large-scale projects that started last year are set to be completed only later.

Looking at the past four quarters, about two-third of multi-unit building projects entering construction phase concentrated in Budapest, so the capital’s share remains exceptionally high. About 69% of projects started in Central Hungary, 13% of the Activity-Start was linked to Eastern Hungary, while Western Hungary’s share was 18%.

Non-residential construction: after a weaker last year, this year started slowly

Within the subsector, two segments accounted for the majority of the Activity-Start: offices and industry. Offices performed rather poorly in previous years but recovered somewhat in Q1 2026 with their share within non-residential construction going up to 34% compared to 9% in the previous two years. Industrial properties and warehouses continued to account for the other major part despite the decline (their share dropped to 36% against 44-54% in the previous four years). In the first three months of this year, about 9-10% of started non-residential projects were related to wholesale and retail and education.

In 2026, besides the previously mentioned office, industrial and logistics projects, the largest non-residential projects also included Cholnoky Jenő Student Camp in Révfülöp, Rheinmetall RDX explosives factory in Várpalota, Mixvill shopping center in Debrecen, and Phase 1 of MyRA Park M3 shopping park. In 2025, non-residential construction was also characterized by weaker Activity-Start, but several high-value projects were launched such as the special operations barracks in Szolnok, BYD’s assembly hall, logistics warehouse, press plant and lightweight construction plant in Szeged.

In the past three years, non-residential projects reached completion at an exceptionally high value, between HUF 1,600 and 1,700 billion. During this period, Phase 1 of eMAG logistics centre, certain elements of BMW and Mercedes-Benz projects and several logistics projects were completed, including Robert Bosch logistics hall in Miskolc. Activity-Completion indicator may remain at a high level this year as well. The Hungaroring paddock building has already been handed over and several elements of BYD projects, Samsung Göd expansion, and several CATL buildings in Debrecen may also be completed.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)