Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Dr. Sebastian Sipos-Gug, EECFA’s Romanian analyst has looked at the trends that are worth monitoring in the residential market in Romania this year. Among them are the construction costs boomerang, the drop in wages and consumption, considerable interest in multi-family buildings, smaller homes and a greater dependence on mortgage loans.

What we saw in 2025

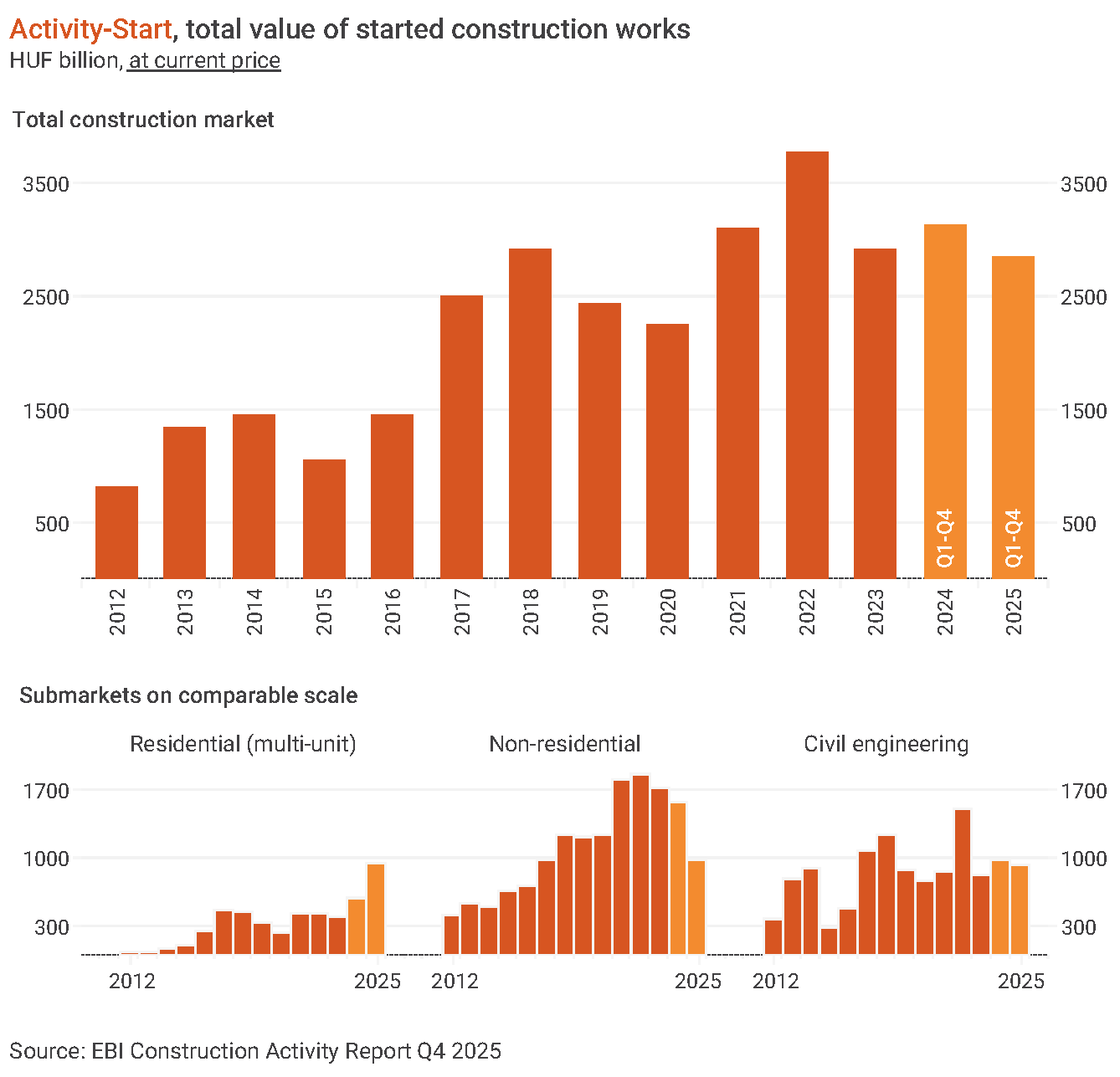

The construction market faced many challenges in the previous year, alongside the entire national economy. While there was a focus on civil engineering, especially when it comes to EU co-funded projects, the rest of the segments lagged behind.

In early 2025, the removal of fiscal facilities for construction employees led to the decline of their net incomes, and an increase in wage-related expenses for companies. Overall, the effect of this measure was an increase in construction costs.

Then came the multiple shocks of the liberalization of energy markets in July, and a VAT increase in August, which pushed inflation upwards significantly, with the CPI reaching 9.88% in September. In a snowball effect, this led to lower real wages and disposable income, which translated into a reduction in private consumption, and, ultimately, means lower demand for residential construction on the short and medium terms.

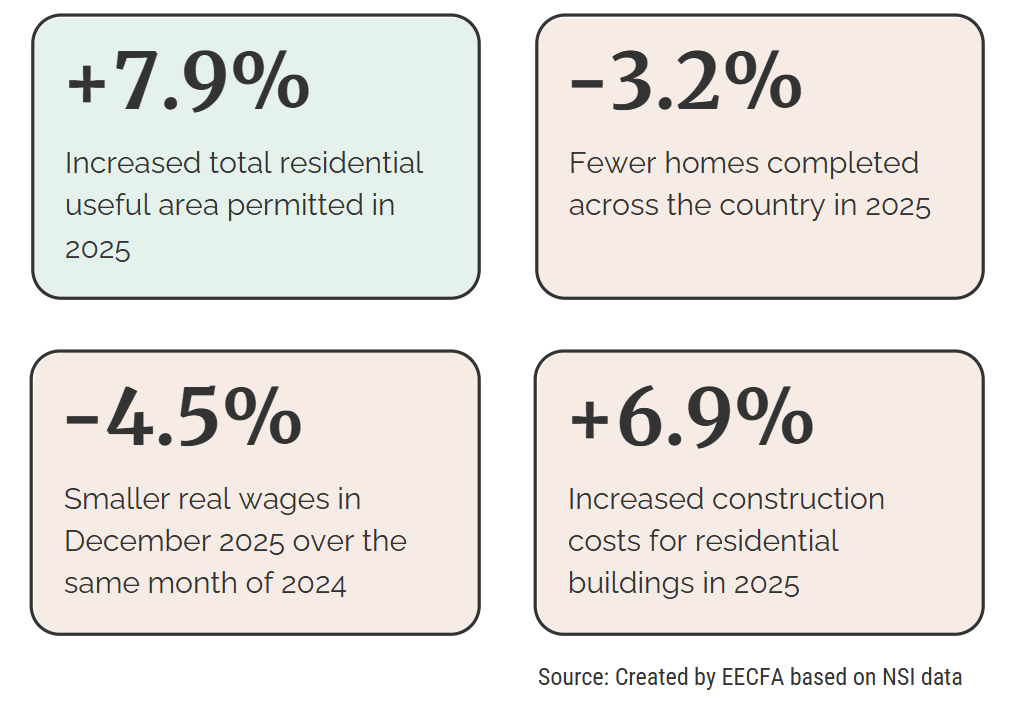

The optimism shown in the increased number of permits, and the useful building area in them, compared to 2024, is countered by the decline in the number of completed homes. Thus, while developers might be looking to the future, their actions in the present are lacking, also evidenced by a significant (-21%) annual decline in the value of started construction works in 2025 (source: EBI Construction Activity Report).

What to watch in 2026

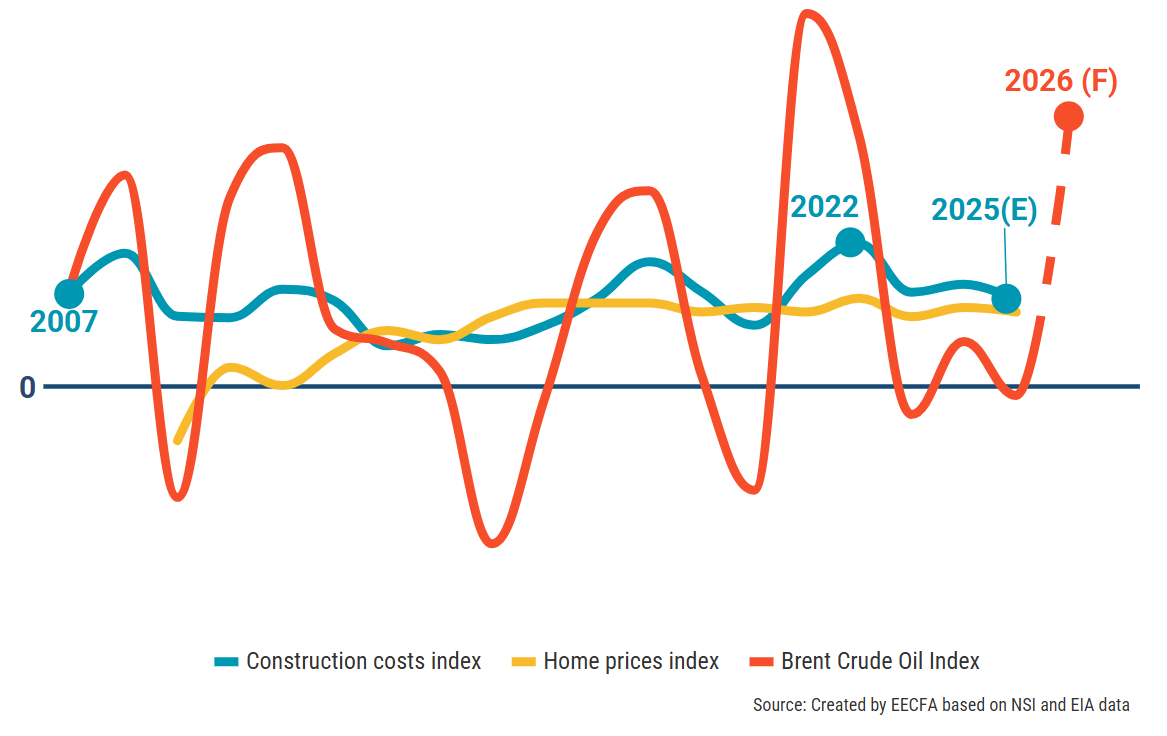

Construction costs boomerang. While previously the expectation was that construction costs would gradually decline in 2026, they proved quite resilient to changes in wages, and fuel and construction materials prices remained relatively stable in the past year. Thus, late 2025 forecasts placed construction costs on a small, descending trend.

The conflict in Iran and its repercussions on oil and gas prices might throw astray these predictions. As of March 2026, oil prices were approaching 2022 levels, and, if they are not reversed rapidly, might have a similar impact on world-wide inflation, energy prices and, eventually, construction costs. A reversal, however, seems rather unlikely at the moment as the damage to energy infrastructure could take years to undo.

To make matters worse, in the past few years home prices grew slower than construction costs, reducing potential profit margins for developers. Added to the decline in real wages, it remains quite unlikely that there will be room for prices to increase alongside construction costs, again similar to 2022, further eating into builders’ financial return potential.

Decline in wages and consumption. Wage growth for 2026 was already forecasted to remain low, underperforming inflation (source NFC – National Forecasting Commission Autumn 2025 Report). Add to that the further shocks now expected from increased energy costs (due to oil and gas prices rising considering the conflict in Iran) and food costs further rising due to increased fertilizer prices, the downwards pressure on real wages is likely to be worse than forecasted, with a slower recovery.

Real wage decline will make it harder to purchase and build new homes, with a negative impact on demand for residential construction. But it could provide a boost to renovation activity, especially when it comes to energy efficiency, as switching homes becomes harder.

High interest in multi-unit residential buildings. Looking at building permits trends for the past decade, single-home buildings have remained relatively stable, while the majority of growth was due to multi-unit buildings. Under price pressure, on the backdrop of restricted wage growth and a contractionary macro-economic outlook, it remains most likely that for the near future we’ll continue to see more interest in the latter. Another connected issue is that of internal mobility, with migration from rural to urban areas in search for education and economic opportunities, increasing demand for denser residential construction.

Smaller homes. While the mean area in permits remained relatively stable between 2017 and 2025, there is a historical precedent in economic downturns leading to smaller homes being built so as to increase accessibility. Since the economic outlook for the year seems to have worsened, this could be the case again in 2026.

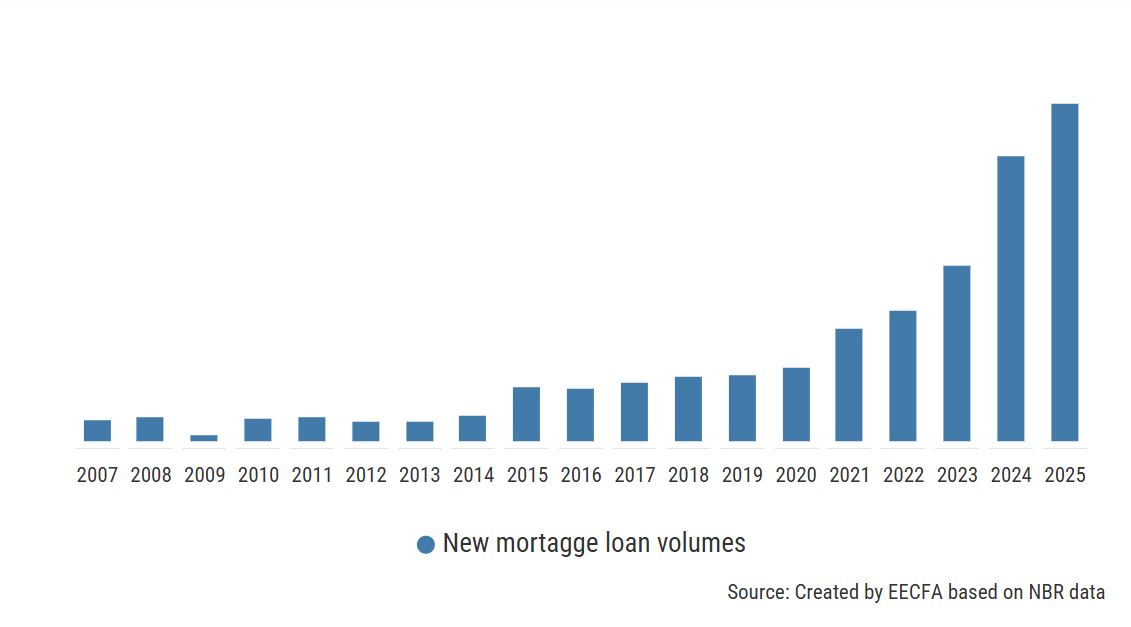

Increased reliance on mortgage loans. Despite the highest interest rates seen in a decade, the volume of new mortgage loans increased dramatically in 2024 and 2025. While some of this could be blamed on higher home prices, there remains a major portion that cannot be explained by price or transaction dynamics. Thus, it is quite likely that it reflects a reduced ability to buy homes without applying for a loan. This is also evidenced by the fact that the share of the population currently housed in a dwelling that was purchased with a mortgage loan grew steadily from a low of 0.5% in 2007, to 1.5% in 2024 (source: Eurostat). This could have been further boosted by the expected drop in interest rates as inflation seemed to be heading in the right direction. However, as of March 2026, this seems less likely, as the conflict in Iran would lead to another energy-led inflation event. Nonetheless, with real wages on the decline, mortgage loans will continue to be relied on for boosting home affordability.

Residential, non-residential and civil engineering forecasts up to 2027 can be found in the EECFA Romania Construction Forecast Report. Sample report and orders: https://eecfa.com/