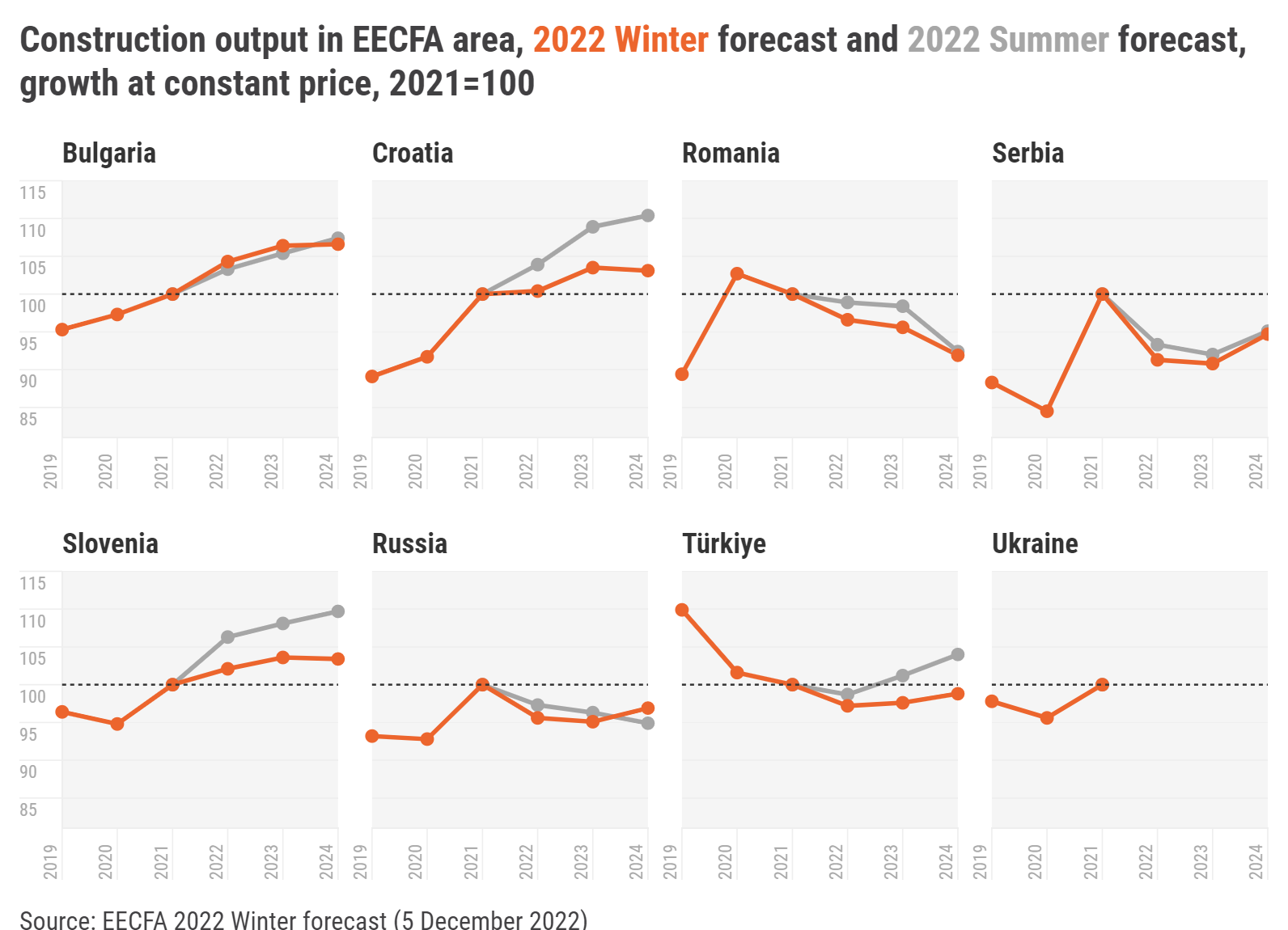

In Southeast Europe the forecast is mixed across the board. For this year, EECFA expects expansion in all but one of its five small countries’ construction markets (Romania). For next year, Serbia will also likely join by turning into negative territory, while in 2025 Croatia is forecasted to be the only country to register a drop, albeit a modest one.

In the Eastern European region of EECFA, construction forecast up to 2025 is positive for Türkiye and Ukraine, while in Russia it seems gloomy all the way. In Türkiye, the reconstruction after the February quakes is the key driver, while in Ukraine, a lot will depend on how fast and how soon the reconstruction of the damaged stock can be carried out. EECFA has attempted to make its first forecast for Ukrainian construction since the war began.

Construction up to 2025 in Southeast Europe

In Bulgaria, the new coalition government can mitigate the expected economic slowdown in 2023 by speeding the absorption of EU programs and the implementation of Bulgaria’s Recovery and Resilience Plan. Total construction output is estimated to achieve real growth in 2023. Factors in favor of this forecast are the strong tailwind in residential construction, a slight growth in non-residential and expectation for an improved performance in civil engineering.

Neither inflation nor population decline could stop Croatian construction output’s growth in 2022, and 2023 looks likely to follow suit. Figures for some Buildings sectors, e.g., Retail and wholesale and Residential, contain surprises. Performance of certain Civil engineering sectors was unexpectedly strong due to events that may be one-off or instead portend a trend.

High construction cost is a major factor behind the expected downturn in Romanian construction this year and next, but the market should recover by 2025. EU funding from the 2013-2020 programs has a spending deadline of 31 December 2023, and with the new 2021-2027 programs still in early phases of implementation, a gap is expected in output while the switch takes place. Also, 2024 is a quadruple election year for Romania (local, parliamentary, presidential, European parliament), bringing new challenges for construction as power transition can bring new priorities and strategies.

Serbia is feeling the consequences of the economic slowdown in the European Union, but so far it seems it will avoid recession in the short term. Construction outputs are also showing a mixed picture with building construction suffering contraction in volumes, while civil engineering will likely break new record highs in 2023. And even though there is a lot of uncertainty, the high level of investments is still maintaining positive economic growth and strong employment figures.

The Slovenian construction industry continues to exhibit resilience amidst a thriving economy. While challenges such as inflation and higher interest rates pose hurdles for the residential construction subsector, non-residential and civil engineering are benefiting from increased public investment. By capitalizing on these opportunities, the industry is well-positioned to contribute to the country’s ongoing economic growth and development.

Outlook in the Eastern European construction markets of EECFA

Last year the Russian economy showed relatively high resilience to the negative effects of sanctions. One growth point was construction that showed much better-than-expected dynamics. Russia’s ‘Turn to the East’ notion in the new external political-economic conditions requires intensive construction of infrastructure objects, which fueled growth in construction in 2022. Going forward, the market will likely show decline driven by negative trends in residential and some downturn in civil engineering on the back of a high base in 2022.

After the elections held on 14 and 28 May 2023 in Türkiye, the value of Lira has been falling, creating financing difficulties for contracted construction projects using imported materials. In Q1, the economy accelerated annually owing to strong domestic demand and low interest rates, while construction continued to regain senses. The two earthquakes in February in 11 provinces caused massive human casualties and damages to over 300 000 buildings and infrastructural facilities. As the Government must restore buildings and infrastructure, growth in construction will speed up in the years to come.

If hostilities end in 2023 and Ukraine’s territorial integrity is preserved, post-war reconstruction will cost several hundreds of billions of US dollars according to various recovery plans. About 3 million Ukrainians saw their homes destroyed and about a third of the infrastructure is damaged. The war caused widespread damage to the construction sector and full recovery is only expected after the war ends. Now there is a partial construction of destroyed or damaged residential, non-residential, and critical infrastructure facilities in relatively safe areas with the help of compensation programs at state and local levels and mortgage programs. A key challenge though is the acute shortage of building materials (glass, cement, asbestos, and gypsum, among others). Resumption in construction will improve the country’s post-war economy, provide jobs, increase the production of materials and open new enterprises.

The EECFA 2023 Summer Construction Forecast Reports up to 2025 have been released and can be purchased on eecfa.com where a sample report can also be viewed.