Press Release on EBI Construction Activity Report Hungary Q1 2023

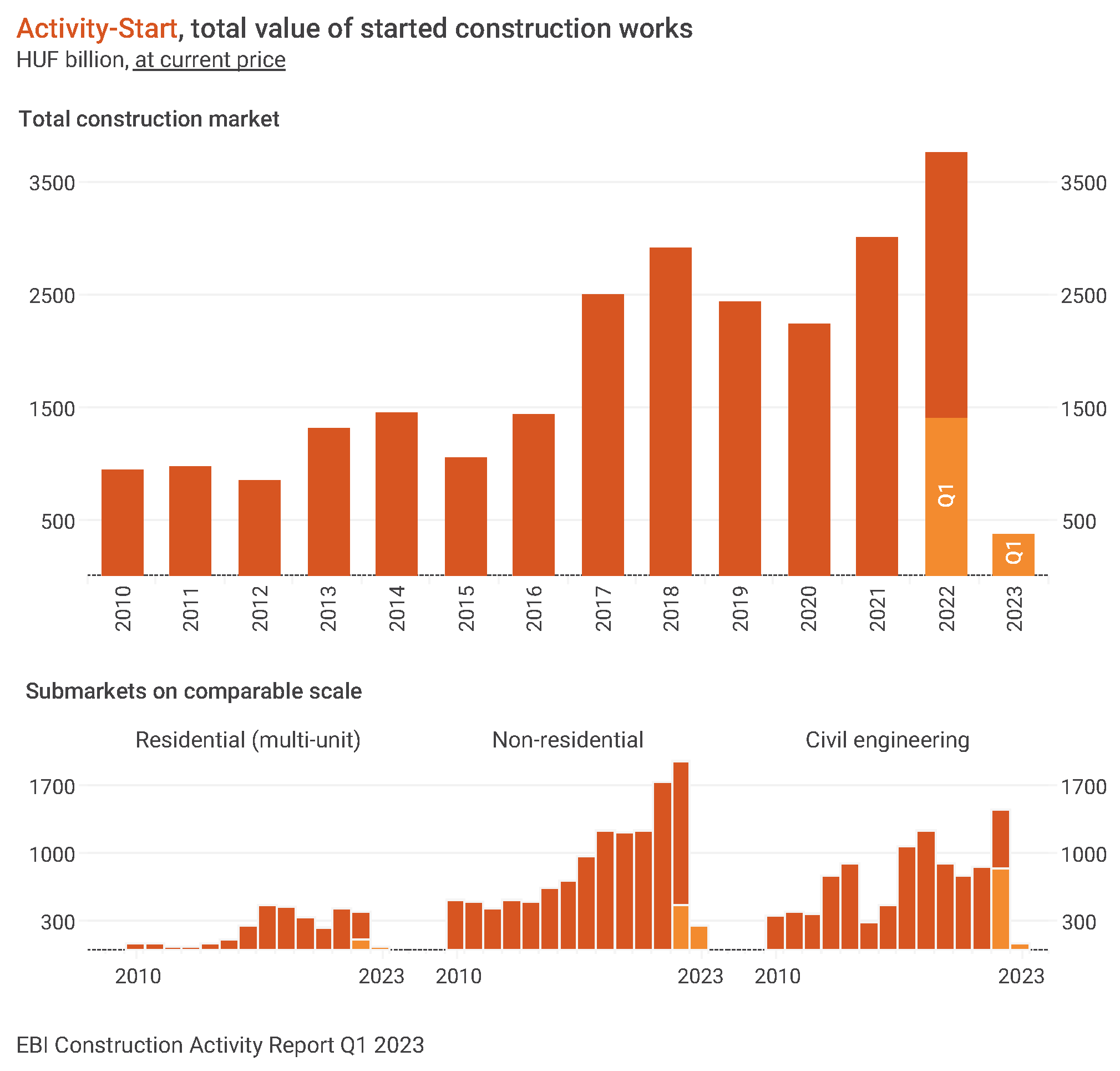

Q1 2023 saw very low Activity-Start in the Hungarian construction industry with only HUF 374 billion worth of construction works started, according to the latest EBI Construction Activity Report. Such a low value of construction start within three months has not been seen since 2016. Compared to the outlier Q1 2022, Activity-Start fell by almost a quarter, but compared to the first three months of 2021, the drop was more than 40%. The value of started works seems particularly modest and the extent of falloff particularly large if we consider that the sector has recently experienced massive price changes. At constant prices, it was only in 2012 when a lower volume of construction works started during three months, and the drop against Q1 2021 already surpasses 60% at constant prices.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Buildecon, Eltinga (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). EBI Construction Activity Report Q1 2023 has been published and can be purchased at ebi@ibuild.info.

Decline not sparing building construction work starts

The value of started building construction projects did not reach HUF 300 billion in the first three months of 2023. It has been one of the most modest quarters in recent years and last time Q2, Q3, and Q4 2020 registered construction starts of a similar value. The decrease in Activity-Start against the first quarters of 2021 and 2022 was 42%-48%. At constant prices, the drop is even more visible: such low numbers were last seen in the segment in 2013-2014.

Both residential and non-residential buildings recorded a decline in Activity-Start. In the former, the value of started construction works stayed below HUF 40 billion, while in the latter, Activity-Start was around HUF 260 billion. At constant prices, these numbers represented the 2014-2015 volumes.

Biggest building construction projects launched in Q1 2023 included several logistics centres like Robert Bosch Power Tool logistics centre in Miskolc, BMW logistics centre in Debrecen, Waberers centre in Ecser, or Blister-Labor-Telemedicina centre in Bicske. The construction of several factories and warehouses also started such as Schneider Electric’s Duna Smart Power System smart factory in Dunavecse, Phase 2 of the Mercedes-Benz body part production plant and Phase 2 of its assembly plant in Kecskemét; another phase of Nestlé Purina pet food production plant in Bük or Rheinmetail ammunition factory in Várpalota. Two large hotel construction projects also began: Sofitel Budapest Chain Bridge Hotel and Movenpick Palace Hotel Budapest.

Few civil engineering works began

Civil engineering Activity-Start continued to decrease after Q2, Q3 and Q4 2022. The total value of started civil engineering projects did not reach HUF 80 billion (the lowest value since 2016), and at constant prices the volume has never been so low in any quarter since 2012.

In road and railway construction, projects started in the value of only about HUF 20 billion, while non-road and non-railway constructions saw an Activity-Start of about HUF 60 billion, roughly the level of Q3-Q4 2021 and Q1 2022.

In Q1 2023 hardly any civil engineering project was among the largest ones. Major projects included the recultivation of the Oroszlány tailings site, the Budapest Freeport project, and the development of Hungaroring’s utility network.

Northern Great Plain ahead of Budapest

Looking at the last four quarters, the highest value of construction projects started in the Northern Great Plain region with a share of roughly 23%. Budapest saw the second highest value of construction starts, while Pest County came third. With this, around 37% of the national Activity-Start was realized in Central Hungary. About 40% of started construction works belonged to Eastern Hungary, while slightly more than 20% of the Activity-Start was connected to Western Hungary with 5% of Activity-Start in Southern Transdanubia.

Hardly any multi-unit housing project-start

The first three months of this year registered very few multi-unit housing project starts. The last time the value of Activity-Start was lower than the current one was in Q3 2020. Before that only the quarters of 2015 saw a similar amount. The drop is even more significant at constant prices: the Q1 2023 level recalls the 2014 volume. In the last quarter of last year several developers decided to launch a new phase of their projects because of which, despite unfavourable market conditions, Activity-Start increased compared to previous quarters. That is why it was expected that the following three months would not be the time for major construction starts. Yet, the two quarters together reported weak figures.

The market outlook is not favourable for the future either. Interest rates on loans are still very high, making financing expensive, and thus hitting on demand. Housing market transactions fell to a fraction in the last quarter of last year and in the first quarter of this year. And until there is a large reduction in loan interest rates, the market may continue to struggle, making developers cautious about starting projects. It is telling that in Q1 2023 no multi-unit housing project could be included in the list of the biggest projects.

In Q1 2023, the value of completed multi-unit housing construction works neared HUF 100 billion; an increase not only over the rather low Q1 2022, but also over Q3-Q4 2022. A significant number of completions are still expected during this year, but it is questionable whether these projects will actually be completed due to the large delays in construction.

Considering the last four quarters, around 64% of the total value of multi-unit residential buildings entering construction was in Central Hungary (61% in Budapest). In contrast, slightly less than 18% was in Eastern Hungary, while Western Hungary’s share was about 19%.

Southern Transdanubia in the limelight

Similarly to Hungary as a whole, construction Activity-Start declined in Southern Transdanubia. In Q1 2023 construction works started in the region on less than HUF 21 billion; a 45% drop like-for-like.

In case of building constructions, Activity-Start rose in the first quarter of this year compared to the third and fourth quarters of last year but stayed at a very low level. Apart from these two quarters, only in 2016 did building constructions start in the region in a smaller amount during three months. The increase in Activity experienced in case of buildings could be attributed to non-residential ones. The total value of projects entering implementation exceeded HUF 13 billion. For example, the construction of Harman electronics production hall and warehouse in Pécs started.

Very few multi-unit housing construction works started in the first three months of this year, though. Such starts amounted to only HUF 1.5 billion (the lowest since 2016). There were quarters in the last two years when Activity-Start in multi-unit housing was HUF 13 billion and, in several quarters, it exceeded HUF 8 billion. Larger project starts then comprised Phase 1 of Városkapu Residential Park in Szekszárd, Bora Residence in Balatonföldvár, or Fonyód Liget Residence.

The value of civil engineering works was also very low: Activity-Start here did not go up to HUF 6 billion in the region. It was in Q2-Q3 2021 when large-scale projects began in the region, including the Bóly-Ivándárda section of M6 highway, R67 expressway, and the section of highway 67 bypassing Kaposfüred.

Original article: Tünde Tancsics, ELTINGA

English version: Eszter Falucskai, Buildecon