Written by Dr. Ales Pustovrh – Bogatin, EECFA Slovenia

Construction output in Slovenia decreased by two-thirds between 2008 and 2015 as the effects of the global financial crisis lingered and the Slovenian banking system needed restructuring. Early signs are showing that the pandemic will have much less impact and might even prove to be beneficial to the construction sector in 2021 and beyond.

Pod Pekrsko gorco project, Maribor, Slovenia – Source: https://ssrs.si

In 2008, the Slovenian construction reached levels it had never reached before since the country became independent. According to EECFA’s research, its total construction output exceeded EUR 4,6 billion in that year, which as we know now, was unsustainable. Construction output decreased for the next 8 years and embarked on a low of EUR 2,2 billion in 2016 before rebounding to an estimated EUR 3,4 billion in 2020.

Then Covid-19 struck and the whole economy entered another crisis. With lockdown measures and restrictions to the physical movement of people, including workers, it was possible that construction would once again feel the burden of a general economic crisis that might force it into a full depression. In practical terms – how can construction workers construct new projects if they are not even allowed to work in groups on site?

After some initial confusion, it quickly emerged that Covid-19 will not have the same effect on the industry. Construction was able to continue its operations unhindered. Unlike in the Great Recession, banks have kept crediting new construction projects and at very low interest rates. Disposable income of the population has not decreased due to generous anti-crisis measures supplementing the lost income. And the government was willing to run large budget deficits as it was able to borrow at virtually zero cost on international bond markets. A part of these financing was invested in different construction projects, including in health building constructions.

Additionally, a fragile coalition of centre-left parties under Prime Minister Sarec fell apart in Spring 2020 and was replaced by centre-right coalition under the new Prime Minister Jansa. His agenda is also based on implementing some long-stalled construction projects, including the new high-voltage electricity distribution network connection with Hungary and the start of the construction of the new hydroelectric power plant near Mokrice. Some previous large construction projects have been continued or even accelerated, including the start of the construction of the so-called 3rd national road axis, as well as the planned expansion of the Slovenian railroad network that would capitalize on the ongoing construction of the new railroad connection toward Port Koper.

With these big-league construction projects and numerous smaller, privately funded ones, initial data on construction output in 2020 show that instead of decreasing, it might have actually slightly increased even during the health emergency and the accompanying economic recession. Additionally, with strong economic rebound predicted for the time after the emergency, potentially as soon as in the second half of 2021, construction output might grow further.

EECFA’s Winter 2020 forecast is envisioning for Slovenian construction a 0,3% real growth in 2021 and 1,7% in 2022, but with an upside potential.

Segment-level construction forecast is available in the EECFA Winter 2020 Construction Forecast Report Slovenia that can be purchased on eecfa.com

The new government has presented an ambitious long-term plan for civil-engineering, health and nursing home construction for the next few years (although it implementation will greatly depend on the results of the next election in 2022).

It will also have plenty of financing available from the comprehensive EU Recovery Plan. In Slovenia’s national recovery and resilience plan, the European Commission has confirmed access to EUR 5.2 billion for the 2021-2027 period. All in all, it is becoming clear that unlike in the previous crisis, access to funding for construction will not be a problem this time.

Value of started construction projects on downward track in Hungary

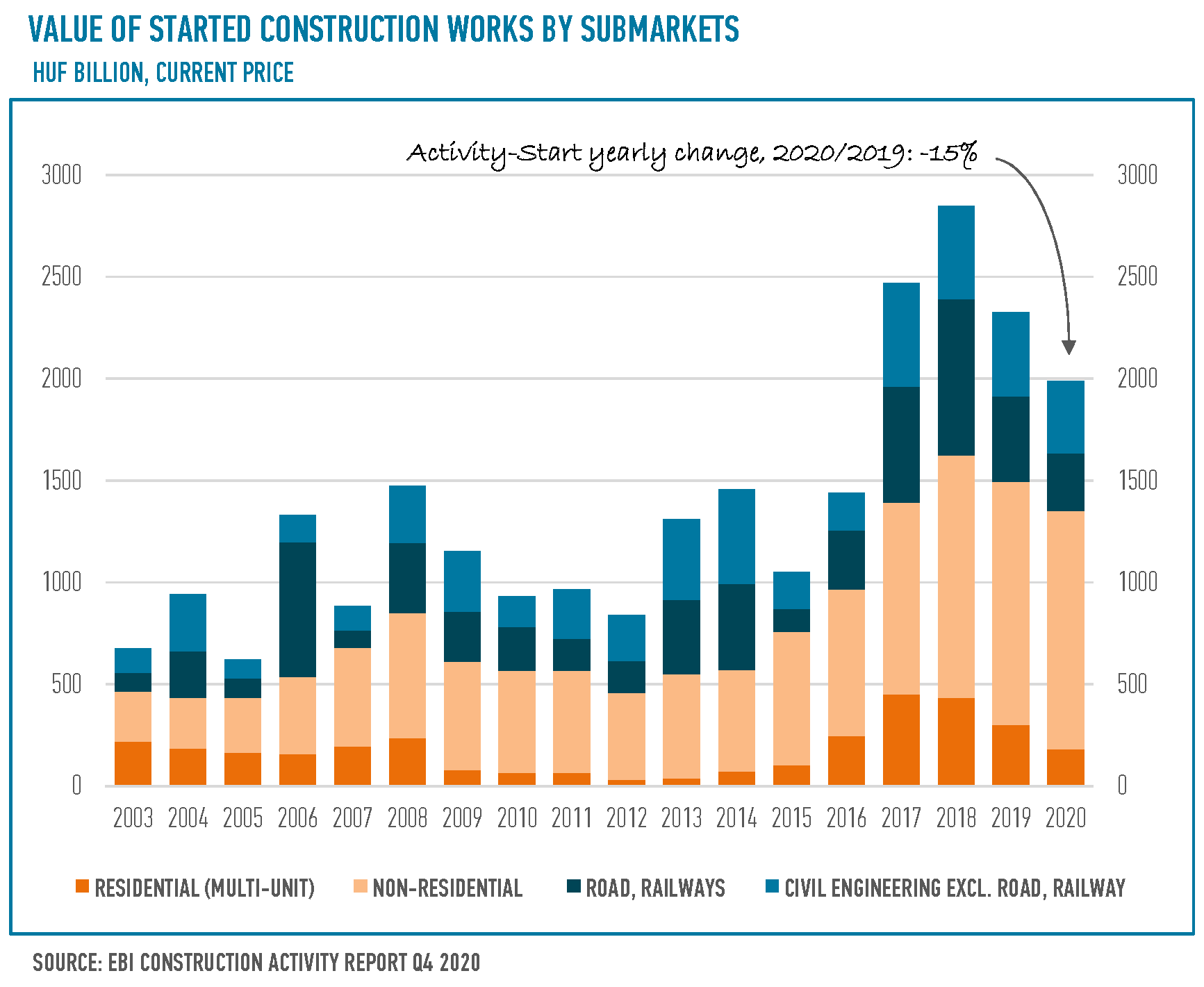

Due to the pandemic, construction industry in Hungary last year registered a significant fall and the last quarter couldn’t save the year either. The latest EBI Construction Activity Report has found that Q4 2020, similarly to the low-value Q4 2019, saw the start of construction works at a value of HUF 442bln. Owing to the massive drop in mid-2020, 15% less construction work started than in 2019 and 30% less than in 2018. In 2020 the Activity Start Indicator of EBI Construction Activity Report accounted for less than HUF 2000bln (HUF 1990bln). And the decline affected all major subsectors.

The EBI Construction Activity Report Hungary examines the situation of the Hungarian construction industry on a quarterly basis, including the volume of newly started construction works, and the value of projects completed in each quarter in aggregate and by sector as well. It is prepared by Buildecon, Eltinga (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). Full publications can be purchased at ebi@ibuild.info.

Building construction registering yet another decline in activity

Although 2020 saw quite a strong start in building construction, the momentum slowed down from Q2 on. As per the latest EBI Construction Activity Report, except for the first three months of 2020, construction works in building construction started at a lower value than in the previous period. In Q4 2020 the Activity Start of EBI Construction Activity Report amounted to only HUF 280bln. Overall, the value of building construction works started last year was HUF 1353bln, much lower than in 2019 and 2018, compared to which the difference was 10% and 17%, respectively.

The main reason for the decline is the great drop in the number of multi-unit buildings. The total value of such projects entering construction phase in Q1 2020 even exceeded the numbers of Q1 2019. Yet, the shrinkage in the following 9 months was so large that the value of projects started in 2020 fell to the level of 2015-2016 in the segment, showing a decline of almost 40% over 2019. In case of non-residential buildings, there was hardly any discrepancy in Activity Start between 2020 and 2019.

The biggest projects launched in Q4 2020 include the construction of Hotel Hévíz in Hévíz, the restoration and development of the Citadel in Budapest, and the construction of several rural industrial and factory buildings such as Nestlé Purina pet food factory in Bük or the ZalaZone military plant in Zalaegerszeg.

Q4 2020 no savior of civil engineering

2020 was a mixed year for civil engineering. In Q1 it managed to maintain the Activity Start value of the same period of the previous year, and Q4 was 70% higher than the end of 2019. In contrast, the middle of the year was well below the 2019 figures with the value of construction works started in Q2-Q3 dropping by 45% against mid-2019. Overall, the HUF 636bln Activity Start indicator for civil engineering in 2020 was almost 40% lower than the average of 2017-2019. But compared to the 2010-2016 average, this value is still 25% higher, so the period between 2017 and 2019 can still be considered outstanding.

Within civil engineering, the total value of started construction projects in road and rail segments decreased by 32% over 2019. In case of non-road and railway construction, the drop was also significant, but we could see a more modest (15%) decrease than previously presented in the Activity Start of EBI Construction Activity Report.

The highest-value civil engineering projects launched at end 2020 comprise for example, the start of construction of the Budapest Athletic Stadium and the ZalaZone automotive test track in Zalaegerszeg.

Central Hungary’s growing share

Looking at all started construction works, Central Hungary and the western regions of Hungary closed 2020 with almost the same Activity Start value as they did in 2019, with the indicator even slightly growing. But in the eastern regions, the total value of projects entering construction phase plunged (by 41%) with the decline occurring mostly in the second half of 2020. Thus, Central Hungary and the western regions increased their share in the value of started construction works, while the share of eastern regions went down to 25%, according to the latest EBI Construction Activity Report.

2021 might be a better year for the multi-unit segment

The pandemic-related economic downturn, combined with the resetting of the VAT rate to 27% as of early 2020, resulted in a remarkably low Activity Start in the multi-unit housing market last year. The last half of 2020 recorded such low numbers that can only be found in the years 2014-2015. However, the newly introduced 5% VAT rate from this year on could halt the plunge and even generate growth in the segment, which would allow the market to return to much higher Activity Start numbers this year.

When looking at Activity Completion indicators, we get a completely different picture as the total value of completed projects last year amounted to a record high of HUF 424bln. This is 40% higher than the previous peak in 2019 and it doubled compared to 2018. Preliminary data for 2021 are expected to have a similarly high value in completed projects.

The 40% countrywide decline in the Activity Start of multi-unit housing was uneven in the regions. In Budapest, the value of projects started in 2020 went down by only 9% against 2019. However, in all other regions the decrease was more than 40%, while in Pest county it was 85%. Due to these tendencies, regional shares have also changed. Because of the importance of Budapest, more than two thirds of the value of the started multi-unit construction works was concentrated in Central Hungary. The western and eastern regions remained well below their multi-year average.

Growing mood for hotel construction, stagnant Budapest

Last year also exceeded the record high value of 2019. In 2020 hotel construction works started on HUF 91bln, a 6% increase like-for-like. The last quarter of last year was outstanding with HUF 36bln of Activity Start registered, according to the latest EBI Construction Activity Report. However, this amount was distributed differently than in previous years between the capital city and rural areas. While there was a roughly 50%-50% share in 2019, in 2020 Budapest only had a 13% share and the rural Activity Start accounted for 87%. Such a low value has not been registered in the capital city since 2016. This is in sharp contrast to the 82% rural annual growth but even in this case, there are major regional differences. In 2020, the two regions pulling the segment were northern Hungary and the Lake Balaton area. For example, at the end of last year, the construction of Hotel Hévíz (Hévíz) and the Hampton by Hilton hotels (Budapest) started. Earlier last year the construction of Minaro Hotel Tokaj, Green Resort Balatonfüred and BalaLand Hotel began.

In 2020, the value of completed hotel construction works also continued to grow, with a total of HUF 48bln worth of hotel completions (a 33% increase). Regionally, the capital city had a higher share in the total value of completed projects (two-third) than in the case of started ones. This year is also expected to see a growth in completions and hotels could be completed at an even higher value.

Completed projects last year include Botaniq Castle (Tura) and Kozmo Hotel (Budapest), while works are expected to be completed in the first half of this year in Budapest for Matild Palace, InterCity Hotel and B&B Hotel. In the countryside Mária Valéria Hotel in Esztergom, Erzsébet camps in Fonyódliget and the youth sports accommodation in Felcsút can reach completion.

Soaring education-related projects

In 2020, construction works on educational buildings started at an outstanding value. Although the peak of HUF 140bln in 2018 was not achieved and fell short of the value of 2019 by a few percentages last year, it is the third most successful year with projects having started on HUF 120bln, far exceeding the average of HUF 44bln in 2000-2016. For example, 2020 saw the start of construction in EMC Measurement Lab server center in Budapest on HUF 16bln, the Semmelweis University Faculty of Medical Sciences, Department of Traditional Chinese Medicine and St. Angela Franciscan Primary School and Grammar School, and the University of Debrecen Innovation Center and Learning Center. The renovation and expansion of the Szeged Medical Sciences Training Block can start at the beginning of this year.

Education-related construction projects amounted to HUF 102bln in Hungary in 2020, and the outstanding trend of recent years can also be felt in completions. For example, the construction of the partly R&D center Univerzum Office Building in Budapest, the renovation of the campus of the Faculty of General Medicine of the University of Pécs and the reconstruction of the Ludovika Wing Building, as well as the construction of the Rózsakert Demjén István Reformed High School were also completed. In the short term, even more projects may reach completion with several of them being in Pest County. In Érd, the renovation of Batthyány Sports School and Primary School and the vocational training center of Kós Károly Vocational High School, as well as the construction of Fenyves-Parkváros Public Education Center and the construction of a primary school in Biatorbágy are planned.

In January 2020, the World Health Organization started issuing the first warning of a novel coronavirus emerging, and on 26 February the first case was confirmed in Romania. Measures taken to try and contain it led a state of emergency and a lockdown introduced on 16 March. One year later, we can look back at how the residential real estate market reacted to the pandemic and the economic crisis that accompanied it, and we can make an attempt to understand where the market might go next.

To start with, prices on the residential real estate market in Q1 2020 reached their highest value in the past decade and an unease started to permeate the market with flashbacks to the 2008 credit crunch and the massive drop in prices and transactions that followed. This made many developers rush to complete projects before the market collapse, a trend we described in a previous blog post.

Prices did indeed start to drop slightly by Q3 2020, but they remained at a level higher than that of the previous year and by the end of the year the early indicators pointed to a return to growth. This has been pointed out in other markets as well and seems to have impacted a large number of developed and developing economies. However, each country is different, and in the case of Romania, albeit some of the causes of this phenomenon are shared, the outcome and forecast might be different.

Residential forecast is available in the latest EECFA Construction Forecast Report Romania that can be purchased on eecfa.com

Everything is relative and so are prices.

One can wonder if these prices are too high, and if they might grow further or if we’re looking at a potential bubble that will burst in the near future. We previously addressed some of these questions in (yet) another blog post.

Since then, the main factors have changed in light of the pandemic, but it might still be useful to look at the same ratio between income and home prices that we analyzed then and bring it up to date. In 2007, the average net monthly income could buy you approximately 0.20sqm of an average located two-room apartment. By 2017, when we last ran this test, one could buy 0.46sqm with the average wage. For 2019 and 2020 alike, our estimates place this indicator at 0.50sqm and so home prices relative to income actually seemed to be relatively stable.

Why some prices were expected to fall and why they haven’t.

While in general there might be a plethora of reasons for residential prices to drop, in the case of the pandemic-related economic downturn we were initially looking at several factors, somewhat similar to those we saw in 2008, such as unemployment, lower income, higher mortgage default rates, stricter lending criteria, higher interest rates and/or a rush to sell off properties by underfunded developers. In the case of the pandemic, some of these did indeed happen:

Employment did indeed decline between March and November 2020, but only by 2%-3% compared to the same months of the previous year (source: NSI). This was largely due to the employment protection measures taken by the government, which provided incentives to furlough personnel rather than firing them.

Average income rose during the pandemic. Even in April and May, the months worse hit by the lockdown, net wages actually grew by 2% over the same months of 2019 (source: NSI). This was also maintained by the furlough scheme that provided payments of up to 75% of wages for the employees of companies affected by the pandemic.

Loans past due declined. By November 2020, the share of loans past due in total loans was 4.83%, down from 5.46% in November 2019 (source: NBR). Granted, this is still far from the 1.24% average we saw in 2008 but is well within the general descending trend of the previous three years. There was some government support in this segment as well, with the possibility of postponing loan repayments for those negatively impacted by the pandemic, and some banks also took their own measures in this direction.

Lending criteria and interest rates. Lending conditions remained relatively stable while interest rates for mortgage loans declined slightly by November 2020 over November 2019 (-0.5pp, source: NBR). This was partly due to the impact of the tax change in late 2018 that raised interest rates in 2019 over their trend and was later reversed.

Developers had a more secure line of financing. While during the previous recession in 2008 a lot of development was carried out through credit, by early 2020 many properties under construction were pre-sold, and down payments on these provided the necessary cashflow to continue building and even wait longer to find buyers in order to sell at a better price.

Furthermore, due to the reduced spending possibilities with the shutdown of non-essential travel, in-restaurant dining and entertainment venues, spending habits changed. Despite income slightly growing (on average), the saving rate went up and thus by end 2020 the population had a lot more money saved on their accounts, even if the term deposits didn’t go up as much. This high level of very liquid capital can be used to fund residential investments, be it renovation, construction or purchasing a new home.

Where the market is heading.

The longer-term trend of price increases on the residential market continues to be the most likely scenario as demand continues to outpace supply in many of the larger cities like Bucharest or Cluj Napoca. Some potential events would bring merit to a more pessimistic outlook:

Changes in employment and income might be ’ticking bombs’. As said, a lot of the market stability is due to government intervention in preventing mass unemployment and ensuring a minimum income. Once these braces come off, there are genuine concerns that the labor market might see a correction, which would have a negative impact on the residential real estate market. The risk of this is somewhat low, though, since a large portion of those furloughed have returned to work (with some notable exceptions in the hospitality industry), but a small correction could still happen.

Medium- and long-term changes in work trends. With the surge in remote work due to the pandemic measures, one can wonder if this would lead to more structural changes in the way people work in the future. If remote work becomes more common for a significant proportion of people, this will have a massive impact on the residential market. It would lower demand in large cities and increase it in metropolitan areas and smaller cities. This would be somewhat limited in the case of Romania, though, as the country still has relatively large economic segments being less prone to remote work such as manufacturing and construction.

We are already noticing some changes in home buyer preferences. After spending more time at home, either in lockdown or from working at home, home buyers now focus on larger homes, preferably with a yard or at least a large balcony.

Case in point: Cluj Napoca.

Taking Cluj Napoca as an example, the local real estate market is seeing massive demand increases as young people, mainly in the IT field, move to the city to study and take up work. They enjoy higher-than-average income and living in the city gives them proximity to various entertainment and services options, access to a booming labor market, entrepreneurship, and business opportunities. But they also have some major downsides: high rents and residential prices that chip away at their income, gridlocks, light and noise pollution and many other disadvantages of living in a city. With the advent of the work-at-home scheme, they might be more interested in relocating to homes in the neighboring rural area (even more so than they are now) and thus retain a higher share of their wages without the downside of commuting. This would put less pressure on the residential market in the city itself, and lead to lower rents and prices. The city thus becomes less interesting for developers and construction might slow down.

The conclusion.

Despite the pandemic, home prices are seemingly growing. While this might seem strange at first, the actual impact of the current recession on home purchases is limited since the average individual still has their job with a similar or even higher income and is actually spending less of their income on goods and services and thus can afford to save for a down payment.

In the shorter run, the market shows some signs of overheating, but is far from brittle. If the pandemic recovery turns out to be lengthy and there are major changes in the way work is done, it could limit prices and drive them down temporarily. However, if you are holding out in buying a home waiting for prices to collapse, you might be in for a bit of a disappointment.