Rebuilding permits, previously excluded from TurkStat’s statistics, were published on 22 August this year. The addition of statistics on rebuilding damaged housing in earthquake-hit regions raised building permits and completions in Q2 2025.

Video by TOKI (Housing Development Administration): Construction projects implemented by TOKI in the earthquake zone in Türkiye.

This May and June saw high construction production in Türkiye

The Calendar Adjusted Index of Construction Production increased by a respective 20,4% and 24,9% in May 2025 and June 2025 compared to the same months of 2024, after declining in the previous three months. Building construction went up by slightly higher rates, 23,5% and 16,9%, while civil engineering grew less, by 9,9% and 16,7% in May and June 2025.

Construction also had high shares in the Turkish GDP. The Seasonal and Calendar-Adjusted Gross Domestic Product in the chain-linked volume index for construction in Q1 2025 expanded by 7.4% annually, while the national average GDP growth was 2,7%. The rise in construction within GDP began after the destructive earthquakes in February 2023. The rebuilding of approximately 870,000 independent units, including 650,000 dwelling units and infrastructure, started in the following months, and the growth rate of construction in GDP increased to 7,2% in 2023 and 9,3% in 2024.

In Q2 2025 we may expect a higher growth rate for construction than in the previous quarter since the completion of 250 thousand dwelling units has been reported until June 2025. Also, a total of 453 thousand urban and rural housing and workplaces will be handed over to legal beneficiaries by the end of 2025 (Source: Anatolian News Agency).

However, building start and completion statistics did not show the same trend in Q1 2025; the total floor area of construction and occupancy permits fell by 20% and 24,9%, respectively, compared to Q1 2024.

Rebuilding statistics in earthquake-hit regions added on 22 August 2025

Q2 2025 saw a sharp reversal of this trend with the addition of rebuilding statistics of damaged housing in earthquake-hit regions. We have been following the process of inclusion of the rebuilding statistics into TurkStat’s published statistics, and we are happy to see that it was published on 22 August 2025.

The delay of including rebuilding statistics can be linked to the effects of law 7471 which aims to speed up rebuilding damaged structures in earthquake-hit regions. The responsibility of the Ministry of Environment, Urbanization, and Climate Change in rebuilding damaged housing caused by natural disasters is further supported by this law. The Housing Development Administration (known as TOKI in Turkish), affiliated with that Ministry, handles the implementation and financing of rebuilding projects. The Ministry’s local branches have been issuing construction and occupancy permits in earthquake-affected regions as outlined in the same law. TurkStat collects and publishes building permit statistics issued by municipalities and transmitted online to them. Since the local branches of the Ministry were not part of this network, rebuilding permits were not included in TurkStat’s previously published statistics. The table is based on the revised statistics and there may still be further revisions in future publications if there is missing data in current rebuilding statistics.

Building permit floor area,mln m2

Building permit annual change,%

Occupancy permit floor area,mln m2

Occupancy permit annual change,%

2023

197,56

16,7

118,80

-15,6

2024

180,27

-8,7

138,21

16,4

Q1 2025

35,24

-20,0

31, 25

-24,9

Q2 2025

54,36

61,8

27,20

30,2

Rebuilding permits in earthquake-hit regions. TurkStat has revised the data by including permits of all authorized administrations to issue building certificates.

Less building construction activity without rebuilding works can be related to the high-interest rate policy to curb inflation, currently at a 43% level. Both producers and credit users have problems in production and purchasing produced goods without relying on bank credits. Lowering inflation and interest rates would lead to the stimulation of building construction.

Forecast up to 2027 for the Turkish construction market is available in the 2025 Summer EECFA Forecast Report Türkiye. To order it or to request a sample report, please contact us.

This summer ELTINGA at EECFA Research has again looked at how the European Commission sees the EECFA countries. Here is what has changed in the prospects between Autumn 2024 and Spring 2025.

Compared to Autumn 2024, economic outlook has deteriorated in all countries covered, although the projected growth remains positive across the board. The most significant downward revisions have occurred in Romania, Bulgaria, and Hungary, while countries like Croatia, Slovenia, and Russia have seen more moderate adjustments. Growth expectations for both the EU and the Euro Area have also slightly declined, mirroring the broader cooling of optimism across the region.

Average GDP growth in 2025-2026 is projected to be positive in all examined countries, though to differing degrees. Serbia is expected to record the highest expansion at 3.5%, followed by Türkiye (3.15%) and Croatia (3.05%), while Russia (1.45%) is forecast to have the slowest growth in the region. Growth in Euroconstruct member Hungary is projected at 1.65%, falling between the regional average and the broader EU outlook. The remaining EECFA countries (Romania, Bulgaria, and Slovenia) are expected to grow between 1.8% and 2.2%. Despite downward revisions, all countries in the region are forecast to outperform the averages of the EU (1.3%) and the Euro Area (1.15%), continuing the trend of a stronger growth in Eastern and Southeast Europe.

The projected growth rate of gross fixed capital formation (GFCF) for 2025-2026 has weakened in nearly all countries since the Autumn 2024 forecast. Romania has witnessed a major downward revision with the expected growth dropping by just over 4 percentage points, while Hungary has also registered a significant cut of around 2.4 percentage points. Türkiye, Slovenia, and Bulgaria have experienced more moderate declines. In Croatia, the outlook remained unchanged at 3.75%, and Russia was the only country with a slight upward revision. Despite the general slowdown, Serbia is projected to post the strongest GFCF growth at 6.7%, followed by Croatia (3.75%) and Romania (2.95%), while most other countries are set to grow between 1.25% and 2.75%. The EU (1.95%) and Euro Area (1.75%) are to remain at the lower end of the spectrum.

Expectations for the growth rate of gross fixed capital formation into construction have also been revised downward in all countries where data is available. Romania has seen the steepest decline with its projected growth falling from 8.45% to 3.9%, though it still holds the highest rate among the observed countries. Hungary and Slovenia have experienced similar reductions, both dropping by more than 2.5 percentage points. Smaller adjustments have been recorded in Bulgaria and Croatia where the outlook for GFCF into construction growth remains relatively strong at 2.85% and 3.8%, respectively. In the broader European context, the EU and the Euro Area are projected to see only a respective modest growth of 1.9% and 1.6%, slightly below most national forecasts in the region.

The Commission’s view on construction investment is somewhat different from ours. Partly it is because we examine the sector from the bottom. For each segment we come up with an individual story and this is how the total construction market is formed.Our latest forecast is in the 2025 Summer EECFA Construction Forecast Reports. Sample report and order

We, in EECFA, are also less optimistic about the near future than half a year ago. The direction of the revision is mostly downward. In cases of Bulgaria, Croatia and Hungary we project moderate growth which is pretty close to the Commission’s expectations. In four countries, however, we do not think average real growth until 2026 could be positive.

EECFA released its 2025 Summer construction forecast on 23 June. See a sample report and place your order on eecfa.com. To get discounts, you may contact us.

Southeast European construction markets up to 2027

According to Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian research institute, total construction output in Bulgaria is anticipated to grow by 3% on average for 2025-2027 with a stronger growth in the middle of the period when the absorption of operational programmes and the implementation of the Recovery and Resilience Plan are to gain momentum. According to the sectoral breakdown, residential construction is expected to be the subsector with the weakest performance, while non-residential construction and particularly civil engineering are predicted to see stronger growth figures. Against this backdrop, the country’s economy is set to register a slower-than-expected growth in 2025 and 2026. In parallel, it is awaited to benefit from the effects from the full Schengen area membership effective from the beginning of 2025 and from the euro adoption expected on 1 January 2026.

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members think that Croatia’s construction as a whole continues vibrant due to the combination of continuing transitioning-economy catch-up growth and large inflows of EU money. Both are beginning to diminish, however, and that will affect all construction segments, some more strongly and more quickly than others. In building construction several sectors have seen the end or are close to seeing the end of catch-up growth. Others, particularly those that benefit most from EU finance, are still going strong. Civil engineering continues to profit greatly from EU funding, and because of the poor initial condition of Croatia’s infrastructure after independence, much catch-up construction remains to be done. Certain government policies will have a great influence on specific building and civil engineering sectors. Those policies include the housing policies embodied in Croatia’s new National Housing Policy Plan until 2030, the new tax on real estate and the country’s renewable energy permitting and electrical grid hook-up fee rules.

‘Romania’s macroeconomic outlook remains positive, but more reserved as the political instability and fiscal uncertainty have done little to improve growth opportunities’ – says Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild. At the same time, he adds, the country has the largest government deficit in the EU, which will dampen public investment capabilities. All these will make it harder to finance public works and could negatively impact civil engineering. This is doubly worrying as this subsector countered the decline in other construction segments in 2024, and thus the outlook for total construction remains negative in 2025 and 2026 in real terms. Not all is gloom and doom, however. As inflation and interest rates come down, and employment indicators remain strong, private consumption could boost demand for residential and non-residential construction.

‘In 2025 Serbia’s construction is making new gains in building construction, while civil engineering has entered a period of consolidation after the strong expansion during 2023 and 2024′ – believes Dejan Krajinović, EECFA’s Serbian researcher at Beobuild. Building construction is supported by both public and private investments, boosted by the hosting of the EXPO 2027 in Belgrade. Non-residential construction is the main beneficiary of this event, particularly commercial, office and hotel segments, while residential construction is also keeping historically high volumes. Some delays are seen in civil engineering, but the overall performance is still strong with a long list of planned projects in all major subsegments. Domestic demand is still relatively strong, but economic growth and the level of investments are being muffled this year by uncertainties in the global markets, particularly the weak EU economy, international trade issues and the ongoing wars in Ukraine and the Middle East.

‘Total construction output in Slovenia is expected to decrease from the historic high of EUR 5,5 billion reached in 2023. In both 2024 and 2025, it could contract but remain above EUR 5 billion annually’ – as per the opinion of Dr. Aleš Pustovrh at Bogatin, EECFA’s Slovenian member institute. He predicts the sector to return to growth in 2026 and 2027, mostly on the back of a healthy growth in residential construction buoyed by decreasing mortgage rates. On the other hand, civil engineering is prognosticated to shrink significantly in 2024 and 2025 due to some large projects nearing completion, like the new railroad connecting Port Koper. Both non-residential and civil engineering depend to a large degree on public financing that was widely available in the post-Covid period but will become much less available in 2025-2027. Especially if the overall economic activity continues to slow down. This deceleration and more foreign labourers have also caused lower construction cost growth, but other challenges persist such as the additional bureaucratic burdens (changed permitting process, increase in tax, ongoing discussion on changes to short-term rental legislation, among others) and many external risks in the global economic and political environment.

Eastern European construction markets up to 2027

‘In the forecast horizon, the construction sector of Russia will be under pressure from a range of macroeconomic factors, the main one being the high key rate, which will negatively affect the pace and volume of construction projects’ – according to Andrey Vakulenko at MACON, EECFA’s Russian research institute. The tight monetary policy and the reduced availability of mortgages will likely slow down housing construction, on the one hand. On the other, the high cost of project financing, the general cooling of the economy as well as reduced consumption and business activity will likely shrink the volume of investment in non-residential construction. However, these trends can partly be offset by high volumes of government financing of priority infrastructure and energy projects, which can support civil engineering and ensure near-zero growth in total construction market in 2025-2027.

Prof. Ali Türel, EECFA’s Turkish researcher says that Türkiye has been trying to control high inflation by raising the base rate and managing exchange rate increases through market instruments by the Central Bank and maintaining wage growth at zero or negative rates. This created financing difficulties for industries and businesses, reduced demand for basic consumer goods, and led to affordability problems for mortgage credits. Big declines in building starts and completions in Q1 2025 may also be related to these measures. Yet, the Central Bank’s inflation target for 2025 remains high at 24%. Positive real changes in housing prices relative to building construction costs encourage house building, while their negative real change compared to inflation may be the leading factor in the increase of home sales through equity financing when mortgage credits are not affordable for most households. Rebuilding the quake-damaged 870 thousand units requires about EUR 100 billion and these expenditures have been the primary factor of the large national deficits in recent years.

‘This year, in spite of the continuing war and the economic instability in the country, Ukraine’s construction industry shows signs of recovery and growth on the back of successful programs financing both the construction of new facilities and the reconstruction and restoration of infrastructure in eastern and southern regions’ – according to Prof. Sergii Zapototskyi at Uvecon, EECFA Ukraine. The World Bank estimates that reconstruction would require USD 486 billion. On the negative side for the sector are bureaucratic barriers in the urban planning legislation, shortage of workers caused by mobilization, shortage and high cost of building materials, and logistical difficulties. On the positive side for the sector is demand for housing and the need to restore damaged infrastructure. The near-term future of the industry depends on the level of security, the effectiveness of restoration programs and the volume of international investments.

2025 started off weak in Hungarian construction despite the much higher Activity-Start at the end of 2024 fuelled by launched major projects then. In Q1 2025 the value of started construction works greatly dropped compared to both the previous quarter and the same period of the previous year. The Activity-Start of EBI Construction Activity Report at current price was around HUF 570 billion in Q1 2025; the second lowest quarterly value since July 2020. At constant price, and if adjusted with price changes, it has been the second worst three-month Activity-Start since 2015.

Value of started building construction works fuelled by multi-unit residential projects

Building construction has slightly improved compared to the previous two weaker quarters: the value of started works was well over HUF 500 billion, 18% up from Q4 2024. The improvement, which was also evident at constant price compared to H2 2024, was attributable to the surge in multi-unit residential works. At the same time, Non-Residential Activity-Start continued to see the low levels of the last two quarters of 2024. In the first three months of this year, non-residential construction works of slightly more than HUF 240 billion started, the lowest quarterly figure since 2017. At constant price, no building construction works have started in such a low quarterly value in the past 10 years.

Among biggest building projects launched in Q1 2025 were mainly logistics buildings: CTP logistics halls in Vecsés (Phase 2) and Biatorbágy, and HelloParks logistics hall in Fót. Construction also began on Phase 2 of Building A of H2Offices in Budapest, and the Hungerit poultry processing plant in Szentes.

Critically low value of started civil engineering projects

Civil Engineering Activity-Start was extremely low in Q1 2025 with started construction works worth only HUF 31 billion. This has by no means been the lowest value recorded in the subsector since 2014, both at current and constant prices. Activity-Start in road and railways and in non-road and non-railways amounted to around HUF 16 billion, respectively. Sadly, not a single civil engineering project made it into the largest projects entering construction phase in the quarter.

Regional comparison: Budapest on the lead

According to EBI Construction Activity Report, Budapest had the highest value of construction projects started in Hungary in the last four quarters. And although its share in total Activity-Start slightly dropped, it still stood at 32%, exceeding the 20%-30% typical in the period between 2021 and 2023.

In Northern Great Plain, the region that previously was on the lead, 14% of projects started in Q1 2025. The share of Southern Transdanubia was 16%, while that of Southern Great Plain 11%. Western Transdanubia and Northern Hungary registered the lowest value at 5%, respectively. In Central Transdanubia, 7% of projects started, whereas in the Pest region, 10%.

Multi-unit residential projects shooting up

The latest EBI Construction Activity Report Hungary has found that 2025 started off greatly in the multi-unit residential segment as in the first three months the value of construction starts was almost HUF 300 billion at current price. It has been a record since 2014 and exceeds the previous quarter’s highest value (HUF 209 billion). Even at constant price, the growth in Activity-Start is a 39% rise over the previous quarter.

This increased activity comes as no surprise: the last quarter of last year already witnessed recovery with developers responding to growing demand and preparing for increased interest at the beginning of this year.

The market has confirmed these expectations, and as per ELTINGA’s Housing Market Report, the latest two quarters saw a record in Budapest in the number of sold new multi-unit dwellings. Although a major part of demand came from investors, the question is how long this can last. Developers might become more cautious with project starts towards the end of the year as demand might decrease following interest payments and maturing government bonds.

When it comes to completions, the value of completed multi-unit residential projects in Q1 2025 was around HUF 76 billion, a drop compared to both the previous quarter and the same period last year. At constant price, Activity-Completion in Q1 2025 has been the third worst value since 2019.

Regionally, looking at the past four quarters, Budapest accounted for 70% of multi-unit projects entering construction, while Central Hungary recorded slightly more than 72% of the value of such projects. Eastern Hungary had a 13%, while Western Hungary had a 16% share in Activity-Start.

Better Q1 2025 in industrial buildings and warehouses than in the construction industry as a whole

In Q1 2025 the total value of construction starts of industrial buildings and warehouseswithover HUF 150 billion was slightly higher than in the previous two quarters. True, if we look at the period between 2022 and H1 2024, it was the second lowest value. Last year, in addition to automotive industry projects, several food industry projects started such as Pick’s plant in Szeged, Master Good-Sága plant in Sárvár, or Félegyházi Bakery plant and warehouse in Kiskunfélegyháza.

In the first quarter of this year, as previously mentioned, the largest projects entering construction phase included several logistics projects such as CTP’s logistics halls in Biatorbágy and Vecsés, and HelloParks’ project in Fót. Besides, the construction of several plants began: Unilever’s deodorant factory in Nyírbátor, Phase 2 of Scheider Electric’s Duna Smart Power Systems smart factory in Dunavecse, or Kométa’s packaging plant in Kaposvár.

As for completions in the segment, industrial buildings and warehouses were completed at a value of HUF 250 billion in the first quarter of this year – the third highest value since 2014. Biggest completed industrial projects include CATL warehouse and metalworking plant in Debrecen and HelloParks AN1 logistics hall in Alsónémedi. And we expect to see further major completions this year.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). To purchase the report, ask for a quote

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

Less than 25% of the funding for its Resilience and Recovery Plan has landed in Bulgaria so far. Last month, the new Bulgarian government, which took office this January, submitted a request to revise its Plan. Will all milestones and targets be achieved and will the country get all payments by the deadline of August 2026?

No reforms, no money

Do you remember the Resilience and Recovery Facility (RRF) the European Commission came up with to assist member states after the pandemic? Unlike traditional EU funds, this instrument in the form of national Resilience and Recovery Plans (RRPs) is meant to provide grants in exchange for specific reforms, making it a performance-based tool going hand in hand with time-bound milestones and targets (i.e. reforms). The completion of the latter is strictly tied to the disbursement of funds for public investments which literally means “no reforms, no money”.

For various reasons, in many EU member countries the implementation of the RRF is not going according to initial plans, and governments are currently submitting requests for revisions. They are to be reviewed and eventually approved by the European Commission. This is the case also with Bulgaria and its RRP that is financed with EUR 5.69bln in grants. As of mid-May 2025, though, the country has received less than 25% of the overall amount in the form of a first installment totaling EUR 1.36bln.

What is now at stake is the remaining EUR 4.32bln

The question is when this sumwill be disbursed and whether the disbursement will be in full. The overall completion rate of the milestones and targets Bulgaria committed to in its RRP is at 38%, which stands for 122 finished reforms out of 321 in total.

To make things worse, the respective regulation at EU level says that all milestones and targets are to be achieved by 31 August 2026, and any payment under the RRF is be executed by 31 December 2026.

The new government is trying to speed up implementation and get full access to eligible funding

To address the accumulated delays (resulting also from a series of seven parliamentary elections in three years) and several underperforming parliaments that failed to adopt the respective legislative reforms, in April 2025 the new government submitted a request to the Commission to revise its RRP.

Bulgaria proposes to remove or modify several measures across the plan while cancelling or downsizing projects currently delayed. Since some of the proposed modifications concern outstanding issues under the second payment request, along with the modification request, Bulgaria also withdrew the payment request, with a view to resubmit it following the approval of the amended plan.

The biggest construction-related projects that are to drop out of the new RRP include a programme for the construction and reconstruction of water supply and sewerage systems (EUR 152mln), a project for heat and electricity co-generation from geothermal sources (EUR 123mln) and a pilot project for green hydrogen (EUR 33mln).

Other investments to see reduced funds are the construction of industrial parks and youth centres with an overall cut of EUR 15mln. While funding for all of these projects is to be potentially channeled from other EU programmes, there are projects that will receive more from the RRP than initially foreseen like the construction of the third metro line in Sofia with EUR 33mln in additional funding.

If proposed reforms and modified projects are approved in Brussels, the government expects to get the second and third RRF payment in the course of the year, while all remaining installments are to be disbursed by the deadline in 2026.

Needless to say, this seems like a very ambitious plan given the insufficient performance of the RRP in Bulgaria so far. This could also be seen in the official position of the government – the country may receive all payments by the deadline of August 2026 but will not have time to make all investments. This would mean that the projects underway at that time are either going to be downsized or put on hold until money from other sources is secured.

Segment-level construction forecast on Bulgaria can be found in the EECFA Construction Forecast Report. The new forecast will be out on 23 June. Orders and sample report: eecfa.com

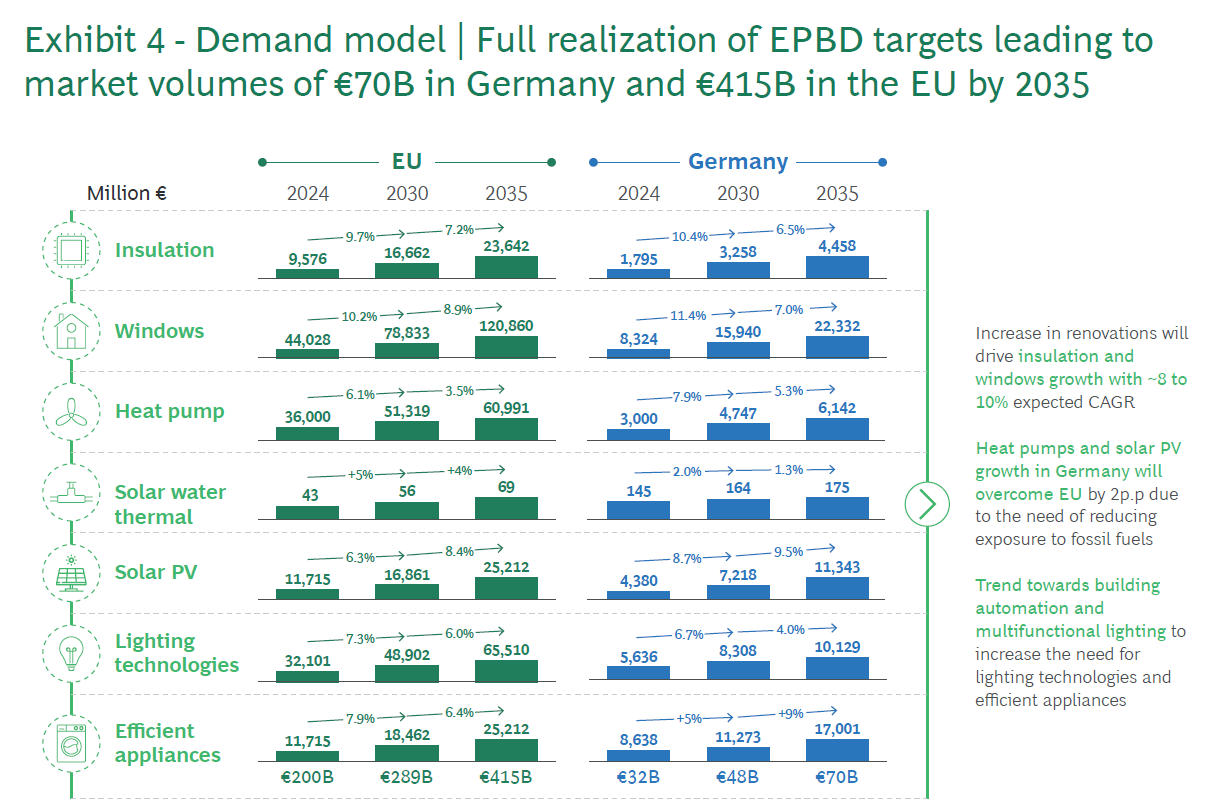

A Boston Consulting Group (BCG) idén februárban publikált egy tanulmányt a tavaly felülvizsgált EU-s EPBD irányelv apropójából, amelyben az energiahatékony anyagok és technológiák iránti jövőbeli keresletet modellezte. A tanulmány szerzői: Johannes Blauhuth, Lorenzo Fantini, Martin Feth, Jannik Leiendecker, és Alberto Pizcueta. Kőrösi Péter (ELTINGA) összefoglalója.

Klímasemleges új épületek az EU-ban 2030-tól

A klímavédelem célkeresztjébe került a legnagyobb energiafogyasztó Európában: az építőipar. Európa szén-dioxid-kibocsátásának több mint egyharmadáért az épületek felelősek, ami összefügg azzal, hogy energiahatékonyságuk átlagosan igen alacsony. Emiatt az épületállomány dekarbonizációja középtávú uniós irány – már rövid távon is érzékelhető célkitűzésekkel.

Az Európai Unió célja a fosszilis tüzelőanyagok fokozatos kivezetése és a megújuló energiaforrások elterjedésének felgyorsítása, ezért tavaly májusban felülvizsgálták az épületek energiahatékonyságáról szóló irányelvet (Energy Performance of Buildings Directive – EPBD). Az új irányelv előírja, hogy a 2030-as évek elejére az épületállomány legrosszabbul teljesítő elemeit fel kell újítani, 2035-re pedig a lakóépületek energiafogyasztását 20–22%-kal kell csökkenteni. Továbbá 2028-tól minden új középületnek, 2030-tól pedig minden egyes új épületnek zéró kibocsátásúnak kell lennie.

A tagállamoknak 2026 májusáig kell átültetniük az irányelvet a nemzeti jogrendbe.

A BCG előrejelzése az energiahatékony építési technikák és anyagok iránti keresletre

Az új irányelv várhatóan már a következő negyedévekben hatással lesz az európai építőipar működésére. Bár a nemzeti szabályozás kidolgozása némi időt vehet igénybe, az első lépések már befolyásolhatják a befektetői döntéseket és a közbeszerzési szabályokat, különösen a középületek és az energetikai felújítások esetében.

Ha az EU-s célok teljes mértékben teljesülnek, jelentős felújítási hullámra számíthatunk és a zöld építkezés is fellendülhet. A BCG előrejelzése szerint a modern szigetelőanyagok és a nagy hatékonyságú ablakok iránti kereslet évi körülbelül 10%-kal, míg a hőszivattyúk és napelemek iránti kereslet évi 6-8%-kal bővülhet.

A lenti ábra a keresletet modellezi az EPBD-célok teljes megvalósulása esetén, mely 2035-re 70 milliárd eurós piaci volument jelent Németországban és 415 milliárd eurós piaci volument az EU-ban.

Az EPBD célkitűzéseihez időben alkalmazkodó vállalatok előnyre tehetnek szert versenytársaikkal szemben az egyre szigorúbb energiaszabványok és a fenntartható építési trendek környezetében.

Forrás: Boston Consulting Group (BCG), White paper: The building sector and EPBD – Demand impications for energy-efficient materials and technologies, February 2025 by Johannes Blauhuth, Lorenzo Fantini, Martin Feth, Jannik Leiendecker, and Alberto Pizcueta.

Written by Dr Aleš Pustovrh – Bogatin, EECFA Slovenia

With the main construction consortium submitting a claim for another EUR 350 million now, the project of Port Koper in Slovenia has again caught public imagination. Despite its 80% readiness, given its past controversies, it is facing scrutiny in its final phase. The second double-track railway line, scheduled for completion in 2026, is set to remove the bottleneck of the existing single-track one between Koper and Divača.

Why such a large-scale railway investment was necessary

Port Koper, Slovenia’s largest seaport, saw consistent growth over the past two decades and evolved into a major logistics gateway for Central and Eastern Europe. In 2024 alone, the port handled approximately 23 million tons of cargo, 3% up from the previous year, while container throughput reached a record 1.13 million TEUs. This performance positions Koper among the leading Adriatic ports, competing closely with Trieste and Rijeka. However, growing volumes of container traffic, vehicle imports, and bulk cargo pushed the port’s capacity toward its limits, particularly due to inadequate inland rail connectivity. The existing single-track railway between Koper and Divača became a major bottleneck, hindering further expansion and reducing overall logistics efficiency.

To enable continued growth, enhance competitiveness, and shift freight from road to rail, the construction of a new, modern double-track railway became essential. The new 27km line is designed to fully replace the existing track and significantly boost capacity—from 90 to 212 train compositions per day—enabling the annual transport of nearly 37 million tons of goods, nearly three times more than before.

An EUR 1.172 billion project

The project is highly complex as it requires significant altitude gain and traverses challenging terrain (20.5km of the new line runs through tunnels and an additional 1.2km over bridges). These engineering challenges have driven up costs considerably. The latest estimate for the project, excluding VAT and calculated at current prices, stands at around EUR 1.172 billion. Project costs have escalated over time.

Initially, in 2010, the project was estimated at around EUR 700 million as a single-track route. Once the plan was changed to a double-track design, costs were expected to rise, but no clear or transparent cost projection was communicated to the public. Combined with an unclear financing structure, this led to growing public concern and political controversy.

As a result, a national referendum was held in which a majority of voters supported the continuation of the project. This decision was later upheld by the Slovenian Supreme Court. To manage the project, the state established a dedicated company, 2TDK, which also implemented a civil oversight and advisory board to address public concerns. A special management and supervision system was introduced to improve transparency and accountability.

Preparations began in 2019, and major works commenced in 2021. Construction is carried out by several prominent companies organized into consortia. The main infrastructure works, including tunnels and viaducts, are executed by a consortium of Kolektor CPG (Slovenia), Yapı Merkezi İnşaat ve Sanayi A.Ş. (Türkiye) and Özaltın İnşaat Ticaret ve Sanayi A.Ş. (Türkiye) on a combined value of roughly EUR 628.3 million.

The final phase of the project, valued at EUR 203.8 million, covers railway system installation including tracks, signaling, telecommunications, electrification, and tunnel equipment, and is handled by another consortium comprising SŽ-Železniško gradbeno podjetje d.d. (Slovenia), Kolektor IGIN d.o.o. (Slovenia), GH Holding d.o.o. (Slovenia) and YM Construction d.o.o. (Slovenia).

Although there were occasional public reports of cost overruns and technical challenges during construction, the project remained largely out of the public spotlight until 2025, so this year, when the main construction consortium submitted a claim for an additional EUR 350 million in costs, citing technical difficulties.

Simultaneously, the Civil Oversight Council raised concerns about poor project governance, accusing 2TDK of opaque and inefficient decision-making. The company’s management firmly rejected these accusations. In response, the Minister of Infrastructure, Ms. Alenka Bratušek, visited the construction site and assured the public that 80% of the work had already been completed and that the project would be delivered on schedule by 2026.

Nevertheless, due to past controversies and rising scrutiny, public trust remains cautious, and the project is expected to face increased attention in its final phase.

Segment-level forecast for Slovenia is available in the EECFA Forecast Report. EECFA conducts research on the construction markets of 8 Eastern-European countries, including Slovenia. Orders and sample report

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Reading the recent blog post regarding permit and completion data one can see that the trend for residential permits in Romania seems to have taken a downturn since 2021, and this naturally raises the questions: What has happened? Has the market peaked or is it just a temporary setback?

The supply-side story

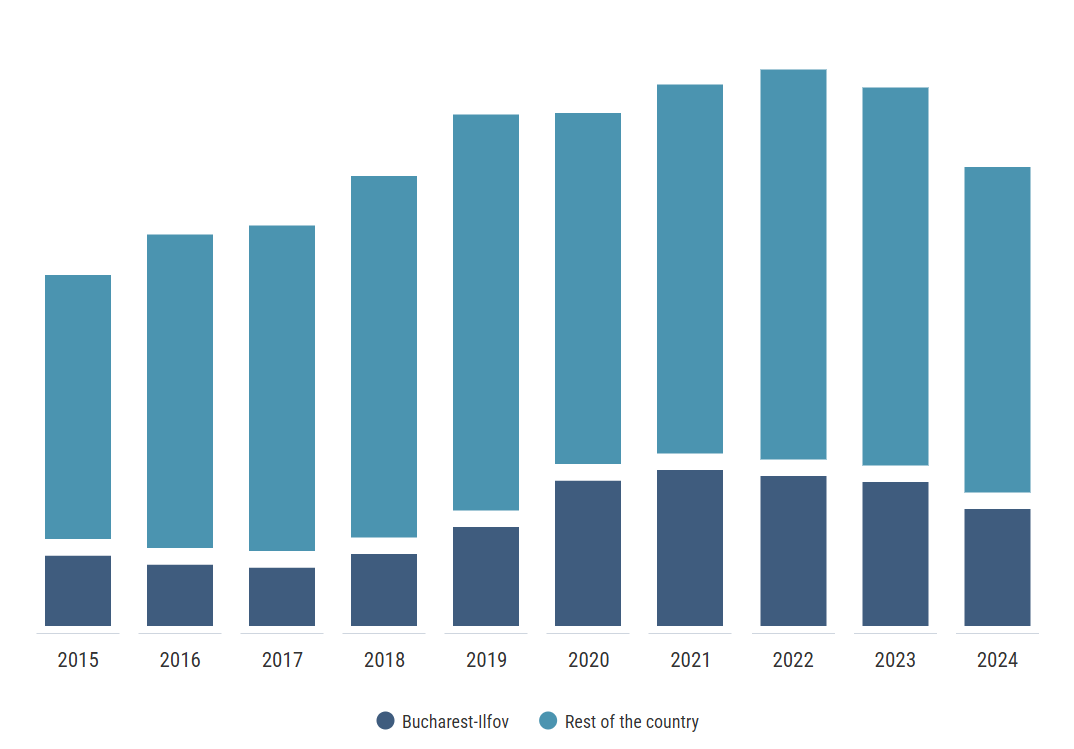

In order to attempt answering these questions, Dr. Sebastian Sipos-Gug, EECFA’s researcher on Romania, started by looking at permit data for a longer period and split by regions. The slowdown in 2023 and 2024 was present in most regions, but none of them was hit as hard as Bucharest where the useful area in residential permits nearly halved in 2024 compared to the peak of 2022. Thus, whatever effect led to the drop in permits, it disproportionately affected Bucharest. While it remains by far the most active region, the drop is oversized when adjusted for its share of the market.

In case of Bucharest, a non-trivial amount of this effect could be explained by the gridlock in the urban planning area, with permits for all types of construction hindered by the cancellation in 2022 of the existing zoning plans which have yet to be replaced by newer versions. This makes it more difficult to gain permits for new developments, and could be, at least partly responsible, for the observed shrinkage in residential permits in the last two years.

Figure 1: Useful area in residential permits, 2015-2024, Bucharest-Ilfov chart presented outside the map due to relative market size (Source: own calculations based on NSI data)

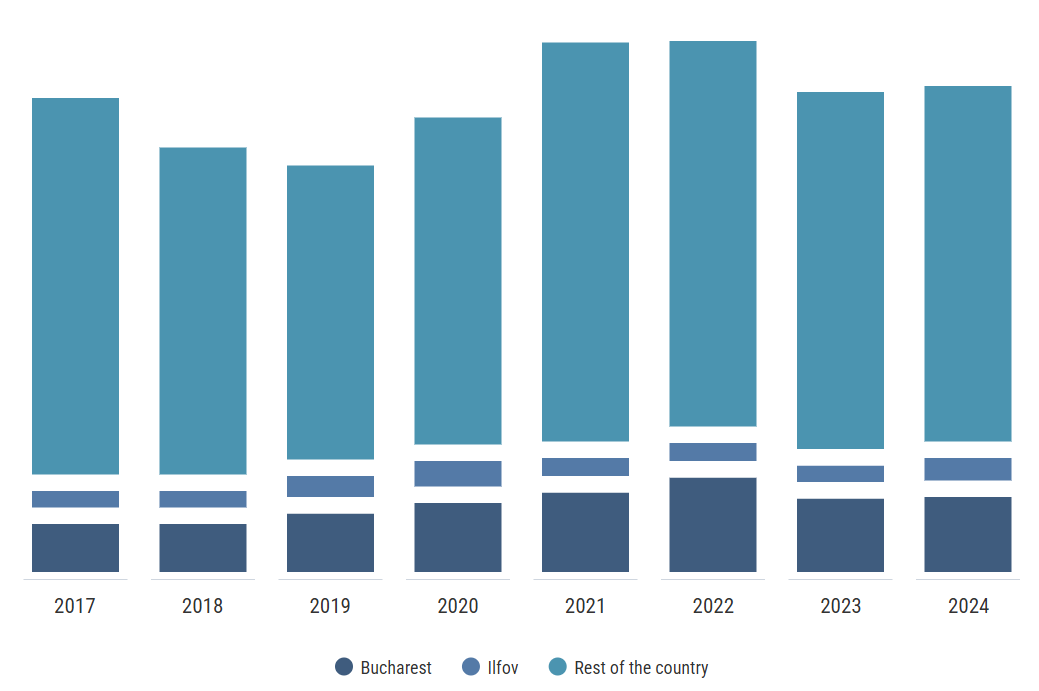

The next logical step seemed to be looking at other indicators such as completions and seeing what happened there. Indeed, they have also been on the decline with the number of completed homes country-wide in 2024 being comparable to that of 2018. Again, Bucharest-Ilfov saw a much larger drop in 2024 over the 2021 figures, standing at –33% compared to –12% in the rest of the country.

Figure 2: Home completions between 2015-2024 (Source: own calculations based on NSI data)

The decline is quite apparent in the supply of new housing overall, but that the situation is much more dire in Bucharest.

The demand-side story

Could the decrease in supply be a response to lower demand? After all, if developers have difficulties selling stock, they are unlikely to start new projects.

Looking at the number of transactions, they indeed declined overall in 2024 compared to the peak of 2021, but the effect was much smaller with just around 10% fewer properties being sold in the whole country, while in the Bucharest-Ilfov region there was barely any change (-0.3%).

At the same time, prices of homes continued growing, but this time Bucharest (+20%) lagged behind the country (+27%), meaning that the price gap between the capital and the rest of the country is slowly closing.

Figure 3: Number of real estate transactions between 2017 and 2024 (Source: own calculations based on ANCPI data)

However, when comparing the growth in home prices to that of the rise in construction costs, the situation looks more dire. As of 2024, residential construction costs grew 41% over the 2021 level, far outpacing the increase in prices. This was partly due to increased materials costs (+32%), but also due to much higher labor costs (+60%) for construction workers. Since in January 2025 tax breaks for construction workers were eliminated and the minimum wage for them grew, it’s unlikely for the situation to improve in the short term, potentially discouraging developers from new investments until prices reach a place where they offset the costs and offer similar margins as before.

What does this mean for housing affordability?

This topic was touched upon last year, in another blogpost, with the conclusion that it is useful to look at affordability from two standpoints: cash buyers and mortgage takers, since increased interest rates can negate the effects of wage growth.

Taking a regional split into account this time, it’s noticeable, and perhaps slightly surprising that homes are more affordable in Bucharest as the wage gap between it and the country average is higher than the residential prices gap.

This took a turn, however, in 2024 as home affordability in Bucharest started to drop, while the national average remained more or less the same. If the previously mentioned issues that limit permitting are not resolved, we can expect this trend to continue in the future as well since a limited supply will mean higher prices.

Another factor that could limit future supply, at a national level, is developer funding. It used to be the case that developers would focus on presales and use very high downpayments in the project phase (up to 90% in some cases) to fund the construction work, without requiring a bank loan.

Since a high-profile scandal regarding a large developer brought this issue into the limelight, confidence in this type of arrangement has declined and buyers are less likely to accept paying high downpayments before construction has even started. Concurrently, there is a bill underway aiming to limit downpayments for unfinished buildings to 10%. Should developers resort to banking loans for their projects, it would make the market more stable but more expensive for them, leading to either lower margins, or higher prices.

Figure 4: Home affordability for cash buyers: sqm in an average 2-room apartment one could afford with average monthly net wage (Source: own calculations based on data from NSI and imobiliare.ro)

When it comes to home affordability for those using a mortgage loan, things are not looking better than they did last year. Inflation has proved to be stickier than expected, and the Central Bank is lowering reference interest rates slowly, meaning mortgages will continue to be relatively expensive in the near future.

While the higher wages in the capital again prove to be an advantage, making homes slightly more affordable than for the average Romanian, this indicator was also on the decline in 2024 for Bucharest, and stable for the rest, shrinking the gap between the two.

Figure 5: Home affordability for mortgage buyers: size of the home (in sqm) one could afford to buy with a mortgage loan, assuming a 25% downpayment, a 30-year term and a debt-to-income ratio of 40% of the average monthly net wage (Source: own calculations based on data from NBR, NSI and imobiliare.ro).

In the context of high energy costs, in 2021 construction costs increased. Since then, the situation has not improved dramatically, and it’s unlikely to change in the near future as inflation and high wage growth will keep an upwards pressure on them in 2025 as well.

Bucharest is doubly feeling the pain when it comes to new residential development. Adding to high construction costs, there are issues with urban zoning and permits approvals. The supply constraints mean higher prices, leading to slightly declining home affordability, especially for those relying on mortgages.

Figure 6: Construction costs for residential buildings (Source: own calculations based on data from NSI)

Forecast for the Romanian residential market is available in the EECFA Forecast Report. EECFA conducts research on the construction markets of 8 Eastern-European countries, including Romania. Contact us for orders and sample report

Written by Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members

Ponderously thoughtful, long-form articles about current events are often entitled “Whither [name the country]?” as in where is that country going next? In that vein a perfectly good title for this (short) blog post would be “Whither the Croatian Construction Industry?”. But just as fine would be “Whether . . .?”, “Weather . . .?” and even “Wither . . .?”. Although probably not “Wether . . .?”. We’ll explain.

Peljesac bridge, Croatia – Photo by Tatjana Halapija

Even late last year Croatia’s economic and political signals were very mixed. Business optimism seemed high: The European Investment Bank’s October 2024 investment survey showed 78% of Croatian firms to be optimistic about their overall investment plans, pretty much in keeping with the EU average of 80%, while business investments had increase by 26% compared to COVID-era levels.

Croatian tourism, a major source of income to drive construction generally and an important driver of construction output (hotels) in itself, was doing well by a number of key measures. In 2024, the country attracted 21.3M visitors, up 4% from 2023, and overnight stays rose to 109M, a 1% increase on 2023. Off-season results were especially impressive, with the January 1 to May 31, 2024, pre-season recording 11% more visitors than the year before and 12.5% more overnights, and the October 1 to December 31 post-season seeing 10.3% more visitors and 9.7% more overnights.

There were some worrying signs, however. Foreign tourist revenues rose only 1.7%, to EUR 13.2B, in the first nine months of 2024, far lower than Croatia’s inflation rate of about 4%, so actually a significant drop in real terms. The governor of the Croatian central bank notes that Croatia’s tourism prices have risen 50% since 2022 compared to 20% for the countries against which it competes for tourists. This bodes poorly for the future of Croatian tourism, as he points out, and so for Croatian construction output. Further, the European Commission forecasts a fall in Croatia’s GDP growth, from 3.6% in 2024 to 3.0% in 2025 and 2.9% in 2026, another negative for construction output.

So, considerable uncertainty in the construction sector even before 2025 brought new, complicating developments. These included new laws, among them laws imposing new taxes on real estate (foreign-owned real estate, too) and on tourism guest houses and new limitations on short-term apartment rentals. On the other hand, they also included simplifications of the building permit process and reduction of the percentage of owners required to authorize repairs and improvements to multiunit dwellings. The combined effect of these developments on construction output is hard to assess.

Most important, though, 2025 brought with it a new United States President and legislature keen to shake up the world economically and politically. In this they have succeeded beyond their most optimistic dreams. The threat for Croatia is that the result will be deeper and longer recession in Germany, the country on which it counts for much or its tourism revenues, or even worldwide, which would prevent Croatia from making up for lost European tourists by increasing its appeal to non-traditional visitors. Europe’s rush to build a powerful defense industry will be of little use to Croatia in offsetting losses of tourism revenues, since its defense industry is relatively small. Again, all in all a significant threat to the Croatian construction sector.

Still, EU money continues to flow to Croatia in large amounts, at least for the time being, and this should support not just civil engineering output (think railways and the electrical grid) but also building construction (repair and renovation of residences, offices and cultural objects). Further, the City of Zagreb is gearing up for major new construction projects now that it has its debt under control, and logistics facilities continue to be inadequate in number and size to meet demand. That said, Croatia’s frequent scandals regarding EU funds could reduce the stream of EU money that is so important Croatia’s public sector construction output.

All told, the tea leaves for Croatian construction output are very hard to read. We’ll know more by our 2025 Summer EECFA Forecast Report, particularly since Croatia will have held its municipal and regional elections by then. These will be a strong indicator of whether the current ruling party has outlived its welcome.

Construction forecast for Croatia is available in the EECFA Forecast Report. EECFA conducts research on the construction markets of 8 Eastern-European countries, including Croatia. Contact us for orders and sample report

So, about those titles. It remains a very open question as to whether the many economic and political crosscurrents affecting Croatia will help or hurt the country’s construction output. One way or another, though, it seems likely that Croatia’s construction sector will weather the current uncertainties given the strength of the country’s tourism industry and the amount of EU money dedicated to the country. And while it’s certain that the sector will not wither, since it seems to have learned the lessons taught by the 2008-2009 Great Recession, it’s still not clear whether Croatia will become the GOAT of Mediterranean tourism destinations, a bell-wether for tourism so to speak, with all of the consequences that would have for construction in Croatia.

The Activity-Start of the latest EBI Construction Activity Report surpassed HUF 830 billion, a value considered to be exceptionally high. It should be added though, that these outstanding numbers were mostly thanks to the start of the construction works of the Mohács Danube Bridge project.

Despite the weaker Q2 and Q3, thanks to the good Q4, in the whole 2024 started construction works totalled about HUF 2800 billion, almost the same level as in 2023. Yet, it was a significant lag compared to the 2021-2022 figures, and at constant price it was still the lowest Activity-Start of recent years. Last time we saw a lower value of construction start than the 2024 level was in 2016.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). For purchasing the full report, please write to us.

Multi-unit residential projects boosting building construction

Building construction projects worth a total of around HUF 500 billion were launched between October and December last year. For the whole of 2024, the value of building projects entering construction phase was nearly HUF 2000 billion. Yet, last year’s Activity-Start fell short of the yearly figures for 2021-2023; the difference compared to 2023 was 5.9%, while compared to 2022 and 2021 it was 15% and 13%, respectively. At constant price, the last time a value lower than in 2024 was recorded was in 2015.

The reason for the better Building Construction Activity-Start in Q4 was clearly the multi-unit residential segment that posted a record growth over previous quarters. Activity-Start in the non-residential segment was low in Q4, though, almost the same as in Q3 (just over HUF 200 billion), still a very modest level compared to the quarterly figures of previous years. At constant price, Non-residential Activity-Start has not been as low in the past 11 years as in Q4 2024. Looking at the whole of 2024, construction works started here on slightly more than HUF 1,300 billion at current price, the lowest value since 2021. At constant price, the last time Non-residential Activity-Start was lower than last year was in 2014.

The biggest building construction projects that started in Q1 2024 included many multi-unit residential ones such as several phases of Kincsem by Bayer, the next phases of Park West and City Pearl. Also, the highest-value projects comprised the start of construction of several industrial and logistics buildings (Waberer’s logistics centre in Ecser, Phoenix Pharma logistics warehouse and office in Győr, the production facility of Félegyházi Bakery in Kiskunfélegyháza, Fémalk’s industrial plant in Dunavarsány and Phase 4 of Hankook tire factory in Rácalmás).

Civil engineering posted a good last quarter last year

In Q4 2024 civil engineering works worth more than HUF 330 billion started, approaching the exceptionally high value registered in Q1. Thus, overall, the level of Civil Engineering Activity-Start of EBI Construction Activity Report in 2024 exceeded HUF 800 billion, more than the 2023 figure and nearing the 2021 value. True, almost the entire Q4 Civil Engineering Activity-Start was due to the start of the Mohács Danube Bridge project.

Around half of the Activity-Start in Q4 2024 was related to road and railway projects with their level roughly being the same as in Q1. The situation was similar in case of non-road and non-railway construction works. The weak numbers in the middle of the year were followed by a larger number of construction starts in the last three months of the year. Yet, looking at the whole of 2024, projects worth less than HUF 400 billion entered construction in roads and railways, not even reaching the level recorded in 2023. At constant price, the last time Activity-Start was lower than last year was in 2015.

Most projects started in Central Hungary

Looking at the past 4 quarters, roughly half of the projects started in Central Hungary. Within, nearly 40% of the works started in Budapest. Eastern Hungary had a 23%, while Western Hungary had a 26% share in Activity-Start. Among the regions, thanks to the Mohács Danube Bridge project, the share of Southern Transdanubia spiked (14% after the previous 5%). The share of Northern Great Plain dropped; it was only 9% against the previous double-digit rates.

Multi-unit housing construction has picked up

In Q4 2024 multi-unit housing construction works practically exploded. The value of started works reached nearly HUF 300 billion, almost doubling the previous record of Activity-Start of EBI Construction Activity Report. Thanks to the outstanding last three months, 2024 was ultimately a record year with the value of started multi-unit construction works surpassing HUF 600 billion. It outnumbered the Activity-Start of 2023 by 66% and represented a growth of about 45% at current price over 2021 and 2022. At constant price, the value of multi-unit construction starts in 2024 was higher than in 2023 and 2022, roughly the same as in 2019 and 2021.

The acceleration in multi-unit housing constructions in Q4 2024 comes as no surprise. Developers may have responded to the pick-up in demand already noticeable last year, plus, they may have prepared for an even greater increase in demand this year – in line with market expectations. Subsidies in 2025 (maturing government bonds and interest payments, private pension fund savings that can only be used for housing purposes this year) may considerably spur the willingness to buy a home this year.

As for completions in the multi-unit segment, construction works of about HUF 400 billion were completed in 2024, exceeding the Activity-Completion indicator of EBI Construction Activity Report of the previous three years. Last year’s multi-unit residential completions were the second highest value registered after 2020.

Regionally, most multi-unit residential projects still started in Budapest, accounting for more than 70% of the value of construction starts in 2024, compared to the previous figure of under 60%. However, Eastern and Western Hungary posted a major decrease and had shares of 10% and 18%, respectively.

Weak H2 2024 in the value of started office construction projects

Activity-Start in office constructions fell sharply between July and December last year with works worth less than HUF 20 billion. Although H1 2024 managed to reach the figures of H1 2022 and H1 2023, overall, there was a large drop in 2024. The value of Activity-Start of EBI Construction Activity Report did not reach HUF 130 billion in 2024. This was a 24% decline compared to 2022, while a 68% and 66% lag behind the outstandingly successful years of 2023 and 2021. After 2015, even at current price, only in 2020 did office projects start in a lower value than last year. At constant price, the office market had not registered such a low Activity-Start as in 2024 in the past 11 years.

The start of MBH Bankholding HQ and the central office next to Rossmann warehouse was the two office construction projects with the biggest value last year. The decline in market-based office projects has not started now. Rather, in recent years, state orders have been able to enable growth in the segment. For instance, the fact that the overhaul of the former Ministry of Finance building in the Buda Castle, the historic reconstruction of the Hungarian National Bank HQ and Phases 1-3 of the reconstruction of the former Palace of Archduke Joseph all started at the same time in 2021 boosted Activity-Start that year. Or, in 2023, the start of renovation works on the Ministry of Agriculture building and on the Palace of Justice building, as well as the start of construction of the BudaPart and Zugló City Centre offices all contributed to high Activity-Start that year. A large part of these will also house state agencies and companies.

When it comes to office completions in 2024, the Activity-Completion indicator was nearing HUF 300 billion, the highest value ever measured in the market. For example, the Hungarian National Bank HQ and the reconstruction of the Ministry of Finance building both reached completion. 2025 may be another record-breaking year in terms of office completions as several office buildings in BudaPart and Zugló City Centre may also be completed.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)