Written by Sergii Zapototskyi – UVECON, EECFA Ukraine

The full-scale invasion of Russia caused a deep humanitarian crisis and exacerbated socio-economic disparities in Ukraine. One of the key challenges is to provide homes for internally displaced persons (IDPs). The mass movement of the population created a shortage of affordable and temporary housing as the infrastructure was not ready for such a load. The government is already working on a new housing policy, which might also help resolve the issue of housing for IDPs.

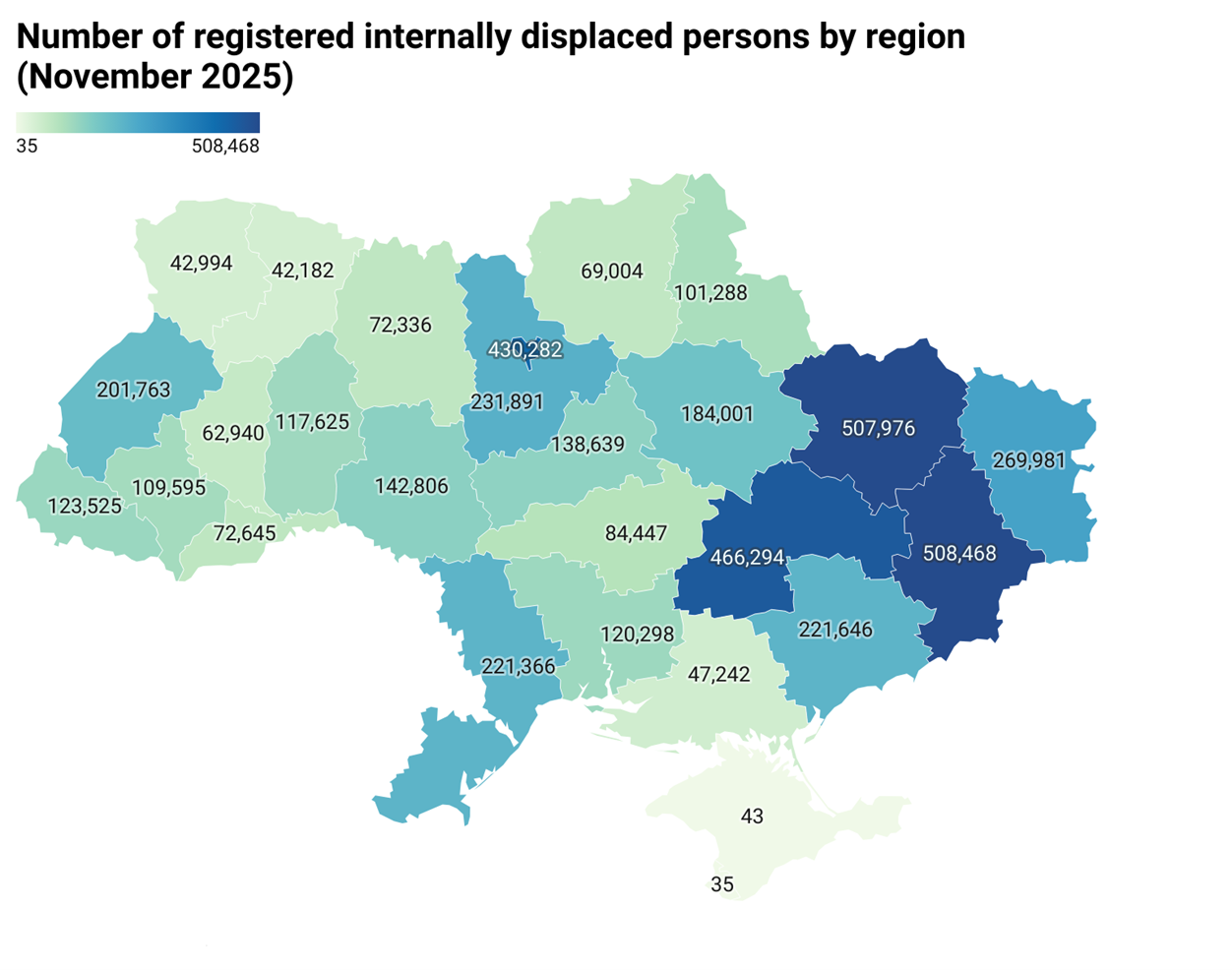

Statistics on internally displaced persons

As of 1 November, this year, 4,588,045 internally displaced persons were officially registered in Ukraine, including 838,436 children under the age of 18 [1]. Most IDPS are in Kharkiv region (508 thousand or 11%), followed by Dnipropetrovsk region (467 thousand or 10%), the city of Kyiv (430 thousand or 9.4%) and Kyiv region (232 thousand or 5%). [3]. IDPs in these regions total about 1.6 million people [1]. As per the result of the 16th round of the survey conducted by The International Organization for Migration (IOM, UN Migration), as of April 2024, about 2.7 million internally displaced people were from frontline areas.

Housing damages, needs and solutions

In total, more than 1.3 million Ukrainian households lost their homes because of the war, including not only IDPs, but also residents of settlements that suffered extensive destruction. The World Bank estimates total housing needs in Ukraine between 2025 and 2035 to be USD 86 billion, mostly to finance repair and reconstruction works of the housing stock (estimated at USD 75.5 billion including the cost of clearing rubble at USD 5.7 billion). USD 404.6 million should go to acute housing needs and funding has also been identified for organizational measures (USD 37.5 million) and regulatory and technical processes, including the development of strategies (USD 12.5 million) to coordinate and implement reconstruction programs [4].

Citizens have already submitted over 850,000 reports of housing damage through the Diia app (the national public-services portal) totalling over 60 million sqm of losses. For comparison, in the pre-war period, an average of 9-10 million sqm of homes were completed in Ukraine each year, demonstrating the scale of challenge and need for multi-level solutions in housing policy. Preferential lending programs are unable to solve this situation and cover the housing needs. The ‘jeOselia’ program provided loans worth over UAH 28 billion, but 52% of this went to military personnel, while IDPs received only 566 pieces of loans. In 2024, within the framework of this 3% mortgage program, only 500 families were provided with housing. The situation is even more critical in the rental market as the state program for subsidizing rental housing has shown low efficiency. The majority of IDPs (90-95%) rent homes unofficially, making them vulnerable to unreliable living conditions and unjustified rental charge increases or evictions.

Modular settlements are a key temporary housing for IDPs, although living conditions here cannot be considered fully comfortable. Initially, they were meant to be short-term but gradually became long-term housing for many families due to their limited finances. Today, besides the psychological difficulties and discomfort of residents, operating such facilities is also a major challenge. The maintenance of modular settlements, including payment for utilities, repairs and security, falls entirely on local budgets, an additional financial burden for communities which often do not have enough resources to sustainably finance these.

Housing policy changes

As the problem of providing housing for IDPs is systemic in nature and cannot be solved solely through financial instruments, a comprehensive review of state housing policy has become necessary, particularly the development of an affordable rental housing segment, social programs, and long-term support mechanisms for both IDPs and vulnerable categories of the population in general.

The Ukrainian Parliament is already working on several key legislative initiatives. The central one is draft law No. 12377 ‘On the Basic Principles of Housing Policy’ to replace the current Housing Code from 1983 which does not contain basic concepts for modern housing policy such as social rental housing or housing stock of communal ownership. Draft law No. 4080 is also important on the inventory of the housing stock. In parallel with drafting these laws, necessary by-laws are being prepared to regulate the practical mechanisms for implementing housing policy (creation and maintenance of housing queues, criteria for selecting recipients of state support, and the procedure of providing various forms of housing assistance). In addition, the government’s plans until 2027 include allocating EUR 650 million to the eRecovery Program, EUR 450 million to support IDPs, military personnel and the families of the deceased, creating a social housing fund and introducing a unified state online system for the long-term strategy of social integration and support for vulnerable categories of the population. All this might help resolve housing for IDPs.

Sources:

- Internally Displaced Persons. State Enterprise “Information and Computing Center of the Ministry of Social Policy, Family and Unity of Ukraine”: https://www.ioc.gov.ua/analytics/dashboard-vpo

- Housing crisis in Ukraine: how to provide IDPs with housing in 2025? International Renaissance Foundation: https://www.irf.ua/zhytlova-kryza-v-ukrayini-yak-zabezpechyty-vpo-zhytlom-u-2025-roczi/

- Internal Displacement Report, IOM Ukraine: https://dtm.iom.int/sites/g/files/tmzbdl1461/files/reports/IOM_UKR_GPS_Internal%20Displacement%20Report_Round%2016_UA_June%202024.pdf

- Rapid Assessment of Damage and Recovery Needs RDNA4, World Bank Group: https://documents1.worldbank.org/curated/en/099052925103531065/pdf/P180174-93c8e8c1-83a2-487d-aaec-a8435f9db418.pdf

- Cedos, Housing and Residential Conditions in Ukraine: Survey Results, 2024: https://cedos.org.ua/wp-content/uploads/zhytlo-ta-zhytlovi-umovy-ukrayin_ok_rezultaty-opytuvannya.pdf

More on the Ukrainian housing market and forecast for the segment, as well as the rest of the construction market will be in our Winter Forecast Report Ukraine to be out on 12 December, along with our other 7 country reports. To obtain it and check a sample report: https://eecfa.com/