There was no construction start indicator in Romania, so we have created an estimation for it.

This poster is a summary of our monthly findings. It shows how the total value of started construction works have changed over the same period last year. Besides, it presents which segments have the biggest start value in the current year. We call this indicator Activity-Start. And they are computed every month for 18 construction segments by aggregating data of construction projects. The projects are from the iBuild database and ELTINGA and Buildecon found the way of creating indicators out of them.

If you need short-term foresight, you will like it.

Brief comment from Janos Gaspar, head of Buildecon:

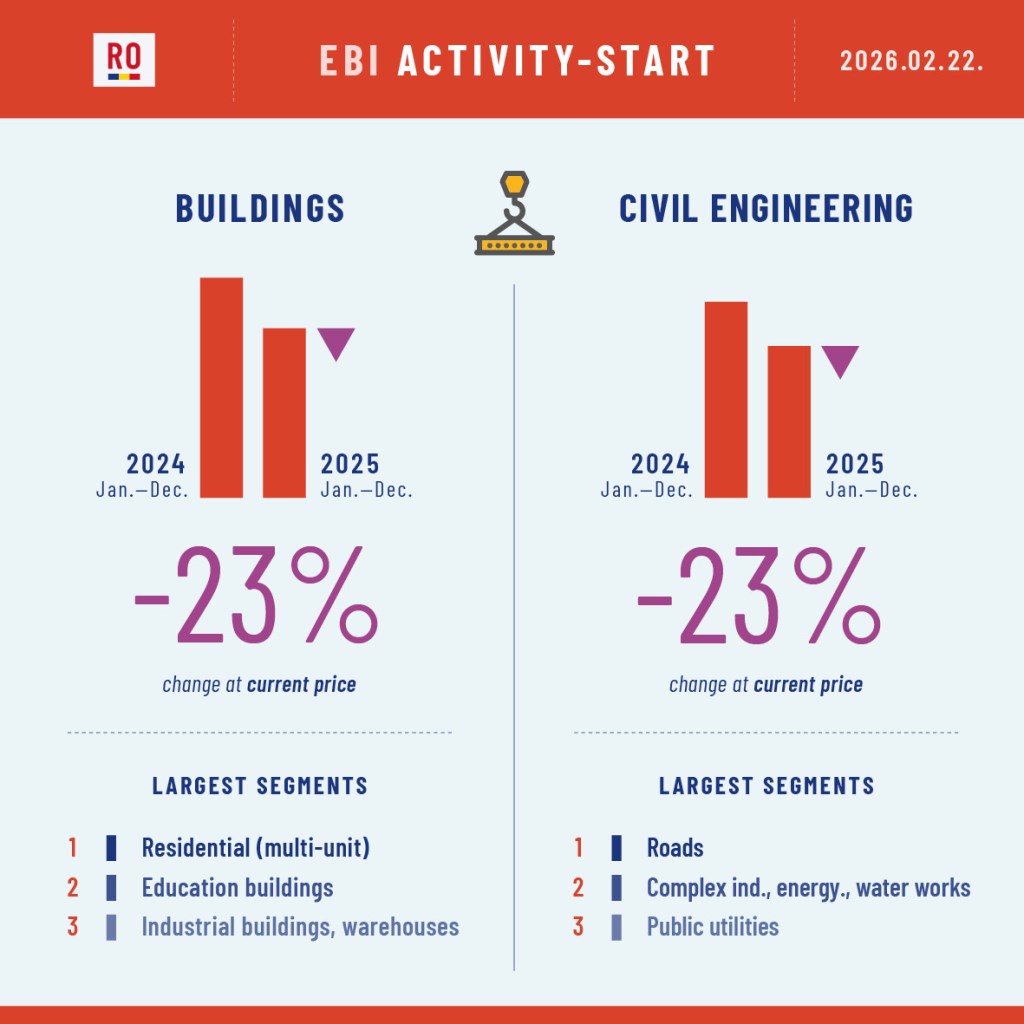

Building construction Activity-Start was significantly down last year. And neither of its submarkets managed to grow. The drop in multi-unit residential was mild, but it means that recovery (started in early 2024) stopped last year. In non-residential, the drop was harsh, the total value of started works in 2025 fell back to the level experienced in 2023. Civil engineering Activity-Start was also down last year, but it is still at a high level.

Every month this poster will be available here on our blog. If your interest is deeper, we have the EBI data visualization (with indicators for all the 18 segments of the construction market), updated monthly and we have the EBI Construction Activity Report Romania (with data and explanations), published quarterly in English and in Romanian. All these are packed into a yearly subscription. For the specifics, please contact us.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Reading the recent blog post regarding permit and completion data one can see that the trend for residential permits in Romania seems to have taken a downturn since 2021, and this naturally raises the questions: What has happened? Has the market peaked or is it just a temporary setback?

The supply-side story

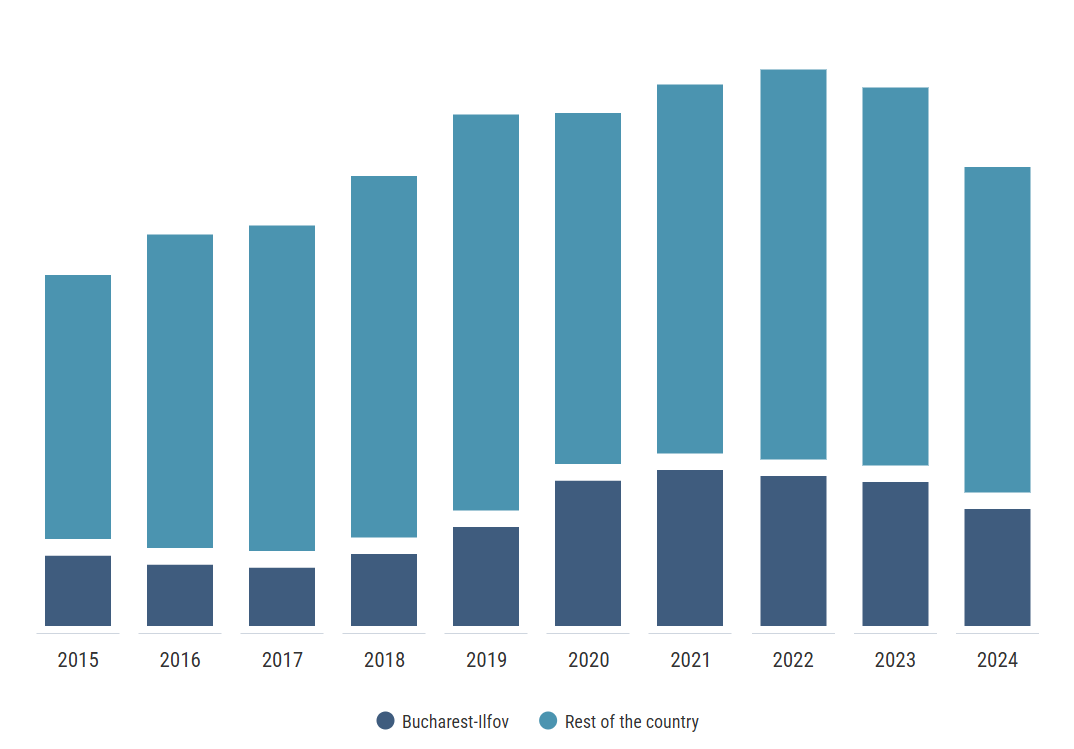

In order to attempt answering these questions, Dr. Sebastian Sipos-Gug, EECFA’s researcher on Romania, started by looking at permit data for a longer period and split by regions. The slowdown in 2023 and 2024 was present in most regions, but none of them was hit as hard as Bucharest where the useful area in residential permits nearly halved in 2024 compared to the peak of 2022. Thus, whatever effect led to the drop in permits, it disproportionately affected Bucharest. While it remains by far the most active region, the drop is oversized when adjusted for its share of the market.

In case of Bucharest, a non-trivial amount of this effect could be explained by the gridlock in the urban planning area, with permits for all types of construction hindered by the cancellation in 2022 of the existing zoning plans which have yet to be replaced by newer versions. This makes it more difficult to gain permits for new developments, and could be, at least partly responsible, for the observed shrinkage in residential permits in the last two years.

Figure 1: Useful area in residential permits, 2015-2024, Bucharest-Ilfov chart presented outside the map due to relative market size (Source: own calculations based on NSI data)

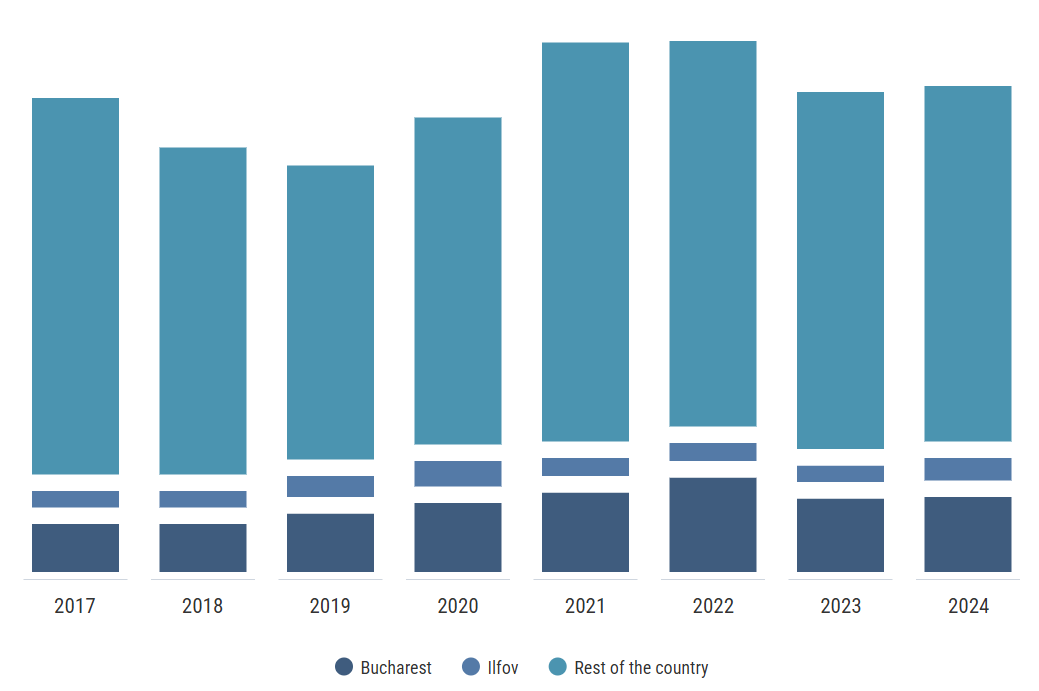

The next logical step seemed to be looking at other indicators such as completions and seeing what happened there. Indeed, they have also been on the decline with the number of completed homes country-wide in 2024 being comparable to that of 2018. Again, Bucharest-Ilfov saw a much larger drop in 2024 over the 2021 figures, standing at –33% compared to –12% in the rest of the country.

Figure 2: Home completions between 2015-2024 (Source: own calculations based on NSI data)

The decline is quite apparent in the supply of new housing overall, but that the situation is much more dire in Bucharest.

The demand-side story

Could the decrease in supply be a response to lower demand? After all, if developers have difficulties selling stock, they are unlikely to start new projects.

Looking at the number of transactions, they indeed declined overall in 2024 compared to the peak of 2021, but the effect was much smaller with just around 10% fewer properties being sold in the whole country, while in the Bucharest-Ilfov region there was barely any change (-0.3%).

At the same time, prices of homes continued growing, but this time Bucharest (+20%) lagged behind the country (+27%), meaning that the price gap between the capital and the rest of the country is slowly closing.

Figure 3: Number of real estate transactions between 2017 and 2024 (Source: own calculations based on ANCPI data)

However, when comparing the growth in home prices to that of the rise in construction costs, the situation looks more dire. As of 2024, residential construction costs grew 41% over the 2021 level, far outpacing the increase in prices. This was partly due to increased materials costs (+32%), but also due to much higher labor costs (+60%) for construction workers. Since in January 2025 tax breaks for construction workers were eliminated and the minimum wage for them grew, it’s unlikely for the situation to improve in the short term, potentially discouraging developers from new investments until prices reach a place where they offset the costs and offer similar margins as before.

What does this mean for housing affordability?

This topic was touched upon last year, in another blogpost, with the conclusion that it is useful to look at affordability from two standpoints: cash buyers and mortgage takers, since increased interest rates can negate the effects of wage growth.

Taking a regional split into account this time, it’s noticeable, and perhaps slightly surprising that homes are more affordable in Bucharest as the wage gap between it and the country average is higher than the residential prices gap.

This took a turn, however, in 2024 as home affordability in Bucharest started to drop, while the national average remained more or less the same. If the previously mentioned issues that limit permitting are not resolved, we can expect this trend to continue in the future as well since a limited supply will mean higher prices.

Another factor that could limit future supply, at a national level, is developer funding. It used to be the case that developers would focus on presales and use very high downpayments in the project phase (up to 90% in some cases) to fund the construction work, without requiring a bank loan.

Since a high-profile scandal regarding a large developer brought this issue into the limelight, confidence in this type of arrangement has declined and buyers are less likely to accept paying high downpayments before construction has even started. Concurrently, there is a bill underway aiming to limit downpayments for unfinished buildings to 10%. Should developers resort to banking loans for their projects, it would make the market more stable but more expensive for them, leading to either lower margins, or higher prices.

Figure 4: Home affordability for cash buyers: sqm in an average 2-room apartment one could afford with average monthly net wage (Source: own calculations based on data from NSI and imobiliare.ro)

When it comes to home affordability for those using a mortgage loan, things are not looking better than they did last year. Inflation has proved to be stickier than expected, and the Central Bank is lowering reference interest rates slowly, meaning mortgages will continue to be relatively expensive in the near future.

While the higher wages in the capital again prove to be an advantage, making homes slightly more affordable than for the average Romanian, this indicator was also on the decline in 2024 for Bucharest, and stable for the rest, shrinking the gap between the two.

Figure 5: Home affordability for mortgage buyers: size of the home (in sqm) one could afford to buy with a mortgage loan, assuming a 25% downpayment, a 30-year term and a debt-to-income ratio of 40% of the average monthly net wage (Source: own calculations based on data from NBR, NSI and imobiliare.ro).

In the context of high energy costs, in 2021 construction costs increased. Since then, the situation has not improved dramatically, and it’s unlikely to change in the near future as inflation and high wage growth will keep an upwards pressure on them in 2025 as well.

Bucharest is doubly feeling the pain when it comes to new residential development. Adding to high construction costs, there are issues with urban zoning and permits approvals. The supply constraints mean higher prices, leading to slightly declining home affordability, especially for those relying on mortgages.

Figure 6: Construction costs for residential buildings (Source: own calculations based on data from NSI)

Forecast for the Romanian residential market is available in the EECFA Forecast Report. EECFA conducts research on the construction markets of 8 Eastern-European countries, including Romania. Contact us for orders and sample report

Activity-Start, that is, the total value of started construction works, greatly increased (+64%) in 2023 across Romania compared to the previous year. It reached the highest level seen in the past decade, both as gross value and growth rate – according to the EBI Construction Activity Report. Even more impressive is the serendipity that as Activity-Start of building construction began to decline, civil engineering sprang up to cover the difference and more.

What is EBI Construction Activity Report? There was no construction start indicator in Romania, so we have created an estimation for it. It helps you understand what could happen on the market in the coming months. The indicators are based on project information from iBuild project database and are published monthly in the EBI data visualization (for all the 18 segments of the construction market). On top of this the EBI Construction Activity Report Romania is published quarterly with data and explanations. This research is a fruit of the cooperation among Eltinga, Buildecon and iBuild. And this is where the name EBI comes from.

Civil engineering in the spotlight

Residential multi-unit buildings seem to have peaked in 2021 in terms of the Activity-Start indicator. With construction costs rising in 2019, followed by high inflation and interest rates, it seems developers were less optimistic about the market’s short-term outlook and consequently, they started fewer projects.

When it comes to non-residential construction, 2023 saw a slight downturn after a very good performance in the previous year. The main factor was Bucharest where the current issues regarding urban planning, compounded with wavering demand, slowed down the development of new buildings across all non-residential segments, but mainly in the office sector.

With the spending deadline for funding from the EU 2013-2020 programs at the end of 2023, a surge in activity in civil engineering was to be expected, and this also explains why Q4 was milder than previous quarters in terms of the Activity-Start. The projects that had a reasonable chance to reach an advanced stage or to be phased into the new programs were prioritized and started in previous quarters.

Of all the projects that started construction in 2023, one stands out: the 37.4km section (Cornetu – Tigveni) of the A1 motorway will be one of the most complex and expensive road segments build so far in Romania since it crosses the Carpathian Mountains and will require 12km of bridges, tunnels and viaducts. It will also have the longest motorway tunnel built so far in the country (1.7km), nearly five times larger than the current record holder.

Several renewable energy projects were also started in Q4 2023: a 102MW wind energy park in Braila County and a 60MW solar plant in Alba County, signaling a renewed interest in green sources of electricity after the recent volatility in the prices of fossil fuels.

The third spot on the list of the largest projects that began in the last quarter of 2023 is taken by the 12,000-seat Sports Arena in Targoviste. The local football team there (FC Chindia – named after a tower built in the city by Vlad the Impaler) had to play its games on other cities’ stadiums in the four years it was in Romania’s First League as its local arena was considered inadequate.

Less glamorous, but equally important, work was also started in Q4 2023 on the water and sewer networks in Dambovita, Iasi and Brasov counties, part of the ongoing efforts at national level to improve the existing infrastructure and provide increased access to public utilities.

When it comes to building construction, all top projects started in the last quarter of 2023 were residential parks, three of which were in Bucharest (Theodor Pallady residential area, Nusco City Phase 2 and Cortina Elysium, totaling more than 1600 flats) and two more in Sibiu County (Magnolia Residence Phase 2 and a residential complex in Selimbar, adding nearly 1000 more flats).

Bucharest loses the first place in Activity-Start

2023 was an unusually even year regarding the regional distribution of the Activity-Start indicator. Previously, Bucharest-Ilfov took the largest piece of the pie and accounted for around one quarter of the value of construction works started in each year. In 2023, however, it lost its lead because other regions saw major increases in Activity-Start, while it and the Center underperformed compared to the previous couple of years and fell behind. The slowdown in Bucharest was visible across the board with drops in new projects, both in civil engineering and buildings. Infrastructure starts had previously peaked in 2022, and the focus switched to completion, while urban planning issues limit new developments for all segments.

The North East region had a boost moving from the third least active right to the top of the podium in terms of Activity-Start. Likewise, West shot up to the top half from the very last position that it held for four consecutive years.

North West region: steady as it goes

While other regions, as mentioned previously, saw major upward and downward changes in their share of the national started construction works, North West maintained the second place that it usually holds. Behind this veneer of stability, however, lies an uneven evolution of different construction types, the EBI Construction Activity Report suggests. Activity-Start indicator (deep orange on the chart) of the building construction submarket began strong, growing fast in Q1 and Q2, and then it plateaued, while civil engineering had a very different path, having a boom in activity in Q3.

Much of the growth can be attributed to the Cluj Napoca – Episcopia railway electrification (166 km), that in itself accounted for almost 1/3 of the value of all started construction works in North West in 2023. The fastest passenger train on this railway averaged 60km/h, with added delays at the Hungarian border and in Cluj caused by switching locomotives from electric to diesel and vice versa. The new electric line will remove this impediment and allow speeds up to 160km/h for passenger trains and the doubling of the lines will facilitate cargo transit as well.

Other major construction works started in 2023 in the North West include several sections of the much-delayed A3 motorway as well as airport terminals in Cluj, Satu Mare, Bihor and Maramures counties. The region attracted several manufacturing investments with the largest project in the building submarket being the Nokian Tyers factory that started construction in Q2 2023 in Oradea.

Healthcare and education buildings are a rising concern due to the aging stock and limited access to services. Thus, extensions of the emergency clinics in Oradea (5.500sqm) and Bistrita (9.750 sqm) also started in 2023. In the same year, work began on a new private school in Oradea (29 classrooms) and on renovating a university building in Cluj County (10.000 sqm).

Cluj Napoca gained notoriety for its tight residential market. Limited deliveries and high demand have pushed the prices here higher every year, and it’s now the most expensive city in the country for home buyers. Supply is slowly expanding with phases of larger projects like Elite City (279 flats) and The Nest (102 flats) starting construction in 2023. Several multi-unit projects were also completed here in 2023, including Liberty Residential (268 flats) and Seasons by Studium Green (150 flats).

Completions (light orange) in the North West were on an upward trend for the past couple of years with building construction overshadowing civil engineering. This is poised to change starting with 2024 as the expected completion of infrastructure projects started by 2023 could even out the field. However, road and railroad projects in Romania have had a long history of delays, cancelled contracts and legal woes, thus, some caution is in order when looking forward.

During 2023 nearly 30km of motorway on A3 were completed on two sections. However, one of them (Nusfalau – Suplacul de Baracu) is quite isolated, so its usage will be limited until it’s connected to the remainder of the network, in 2025 at earliest.

With good Activity-Start and completions, Output (blue) also had a favorable evolution in 2023 for both buildings and civil engineering. Enforcing the idea of steadiness of the North West, Output showed steady growth in each quarter of the last couple of years, at least at current prices.

The major challenges for the North West region in the upcoming years will be to find new avenues of growth, especially in the building segment, and to secure funding and manage ongoing works for infrastructure construction. To quote Lewis Carroll “[…] here we must run as fast as we can, just to stay in place. And if you wish to go anywhere you must run twice as fast as that.”

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Brașov, Romania – Photo by Zoltan Rakottyai on unsplash.com

Dr. Sebastian Sipos-Gug, EECFA’s researcher on Romania, visited the affordability of homes several times in the past as an argument for market stability and to counter doomsayers. Last time he did so, however, he wrote that the residential market was approaching a turning point. And last year, despite decelerating growth in average home prices, the hike in interest rates made housing less affordable for those resorting to a mortgage loan. In case of cash buyers, on the other hand, affordability grew to historically high levels.

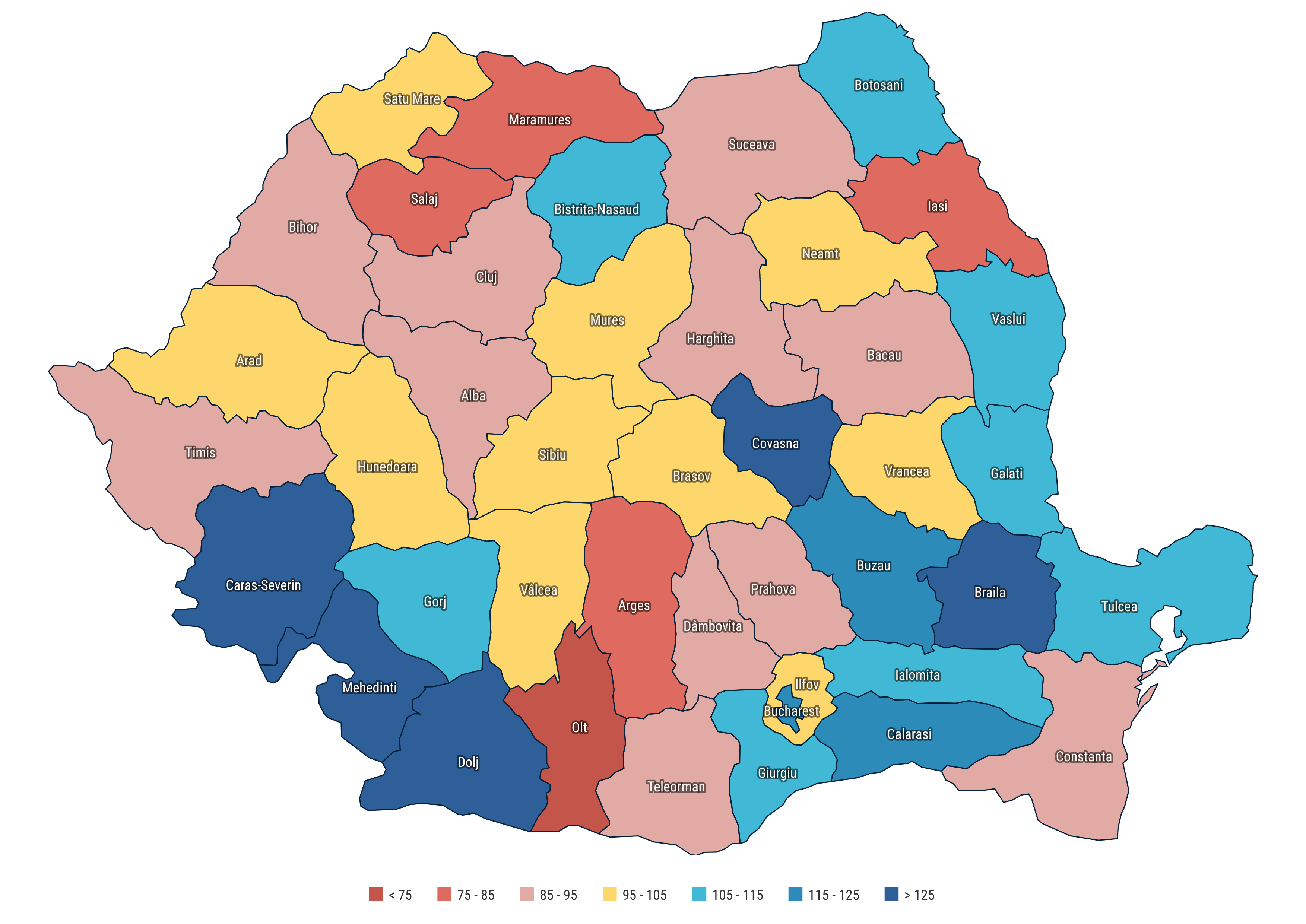

Change in useful area in home permits issued in 2023 vs 2022 (own calculations based on data from NSI)

While official output data is lagging a couple of years, some indicators are painting a less optimistic picture. For instance, permits for homes dropped massively in 2023 like-for-like (-24%) and real-estate transactions also declined (-10%). Decline in the useful area in permits for residential buildings seems to be a national issue since only a handful of counties saw an increase in the useful area permitted, while the usual drivers of growth (Bucharest, Center and West regions) were in the red. This does not mean construction will necessarily decline since the permits issued in 2021 and 2022 were at historically high levels, but it does put a cap on the growth potential of the market. EECFA looked at these figures in more detail and provided forecast up to 2025 in the latest EECFA Forecast Report.

Housing affordability: a key indicator of the stability of the residential real estate market

Housing affordability can signal potential issues in the near future such as right before the market crashed in 2008 one could see that prices became disconnected from income, pointing to a speculative market. Decreasing home affordability can also have a negative impact on economic growth as it diminishes the available share of income that can be used for optional purchases.

A commonly used indicator of housing affordability is the time it would take to purchase a 70sqm home with the average monthly gross wage. While this indicator has merits in allowing international comparisons, it is preferable to look at net wages instead as fiscal changes in 2018 (moving tax burden from employers to employees) would have otherwise distorted the indicator by introducing a break in time series.

Home affordability for cash buyers: sqm in an average 2-room apartment one could afford with the average monthly net wage(own calculations based on data from NSI and imobiliare.ro)

Homes were getting more and more affordable for cash buyers as prices grew more slowly than wages in most years from 2009 onwards. However, this simple model fails to explain all of the data. If it were true that more people could afford homes, we should see a surge in purchases. If not enough homes were for sale, prices would rise quickly. Since we are not seeing either, one needs to assume that some other factor is at play here. A potential solution to this conundrum lies in the fact that cash transactions are estimated to account for slightly more than half of all transactions, with the remainder being funded by mortgage loans.

Accounting for mortgage loans, however, requires some assumptions to be made. Namely, purchasing a home with a mortgage loan that has a 25% downpayment, a 30-year loan term, an average interest rate for the respective year and no additional costs and a debt-to-income ratio of 40% of the national average net wage (currently the legal maximum with some exceptions).

This shows the impact that increasing interest rates to combat inflation has had on housing affordability. While in 2021 the average individual could purchase an average home (under the previous assumptions) of 60sqm, by 2023 this had declined to 47sqm, meaning that for borrowers homes are the least affordable in the last decade.

Home affordability for mortgage buyers: sqm one could afford with mortgage (25% downpayment, 30-year term, 40% debt-to-income ratio of average monthly net wage)(own calculations based on data from NBR, NSI and imobiliare.ro)

What’s in store for the future?

From what we see, the major trends with impact on home affordability are somewhat optimistic:

Interest rates are to drop as the National Bank is set to reduce reference rates once inflation comes down. With current national and EC forecasts placing inflation within the target range by 2025-2026, a gradual reduction is expected in the reference rates by then (a positive impact on mortgage affordability).

Income growth rate has outperformed the increase in home prices in all but two years since 2008. With a robust labor market and a modest but positive outlook of the economy, wages are set to keep growing in real terms in the near future.

Rentals are an increasing alternative to purchasing a home. Traditionally, Romania has one of the highest home ownership rates in the EU (97.7% at the time of the 2011 census), but the recent uptick in rents signals a rise in demand for housing, so this warrants closer monitoring. Depending on the availability of supply, this could mean more transactions or a higher price point since a share of current renters will consider converting to a mortgage, should it be more affordable.

Rent and home price growth rates(own calculations based on data from NSI and imobiliare.ro)

Demography is on the decline. The overall population shrank by more than 5.3% between the two censuses of 2021 and 2011, especially in the southern part of Romania (apart from Ilfov). This should, in theory, make housing more affordable, but the demographic decline is most prevalent in less desirable rural areas, so the impact might be minimal.

Demographic changes between the 2011 and 2021 censuses (own calculations based on data from NSI)

If left unchecked, the combination of these two trends (housing is less affordable for mortgage borrowers, but housing affordability for cash buyers is record high), could lead to increased wealth inequality in longer term. For now, they seem to cancel each other out and demand is somewhat mollified. Nonetheless, Romania remains above the EU average in terms of housing affordability, and, assuming no unexpected changes in market dynamics, it is predicted to improve in the near future as inflation and interest rates come down.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

This question is quite often asked both by those looking to buy a home and by those building homes. The former are hoping for prices to come down, while the latter are worried that prices will come down. Whereas a definitive answer cannot be given, Dr. Sebastian Sipos-Gug, EECFA’s researcher on Romania, has looked at several factors that might tip the balance of the residential market, one way or the other.

For a more in-depth analysis and forecast you can purchase the latest EECFA Romania Construction Forecast Report at www.eecfa.com. EECFA (Eastern European Construction Forecasting Association) conducts research on the construction markets of 8 Eastern-European countries, including Romania.

Where we are now

Despite a rocky start, real estate sales in 2022 were comparable to those of 2021 (+0.2%, source: ANCPI) and so, at least from this point of view, the market seems to be relatively stable, and could tip either way. In a regional view, the northern half of the country was more likely to see a drop in transactions, and Bucharest remains the most active market, with 1 in 5 real estate sales registered in Romania in 2022 taking place in the capital city.

Real estate sales in 2022 as a percentage of the 2021 volumes (Source: ANCPI)

Looking at the longer-term trends, the number of sales in 2022 were 29% higher than those of 2019, but still below the peaks of 2015 (-21%) and 2008 (-31%), and thus it would seem like we are approaching another turning point in the market cycle.

From a house price perspective, there are some signals that asking prices started to go down, however, as of Q3 2022, this didn’t translate in a decrease in official transaction prices. Instead, prices kept rising, albeit their growth rate has somewhat slowed down.

Quarterly indices of Inflation, Rent costs and House prices (Source: Eurostat)

Residential real estate as an investment vehicle

While no official data is available, anecdotally a significant share of newly built homes have been purchased as an investment asset, rather than to be lived in by the owner. Between 2015 and 2019 the increase in prices outperformed inflation and rent growth. Coupled with a low reference interest rate, which made loans cheap and made savings offer lower returns than inflation rate, many retail investors turned to real-estate, with residential being the most accessible market.

As inflation soared in 2022 (+13.8% yearly average), residential prices failed to follow. With inflation expected to remain high in 2023 and 2024 (+10.8% and +5.7%, according to the CNP forecasts, or +9.7% and +5.5% according to the EC forecast), the appeal of investing in residential properties would diminish, pushing down demand, transactions and prices and thus potentially leading to a negative feedback loop. Since real-estate has traditionally been held as an inflation hedge, prices would have to drop quite significantly to trigger this type of loop, a scenario that many feel unlikely at the moment.

Home affordability

Most home purchasers are looking for a place to live, and for them affordability is a very important factor. A useful estimation is that of comparing average prices to the average income, an indicator we looked at in previous blog posts (here, and here) as well. While in 2007 the average monthly wage could buy you 0.20sqm in an average sized two-room flat, this steadily grew to around 0.50sqm in 2020. However, it declined to 0.45sqm in 2022, making homes slightly less affordable for the average worker.

Home affordability – what useful area in an average two-room apartment would the average monthly wage buy you? (Source: own calculations based on data from NSI and imobiliare.ro)

To add to this, rising interest rates for mortgage loans make it even harder to buy a home. In 2022 there were 8 hikes to the National Bank’s reference interest rate, that climbed to 6.75% in December, up from 2% in January 2022. This translated into a near doubling (+82%) of interest rates for new housing loans, and they will remain high as long as the National Bank keeps reference rates up. As inflation subsides, cheaper loans might be on the horizon with a positive impact on demand for residential real-estate for both housing and investment purposes.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

Construction in Romania is not directly impacted by the conflict in Ukraine, however, there are several issues that would be indirectly made worse by it: construction costs, interest rates and inflation.

Construction costs already grew at a fast rate in 2021 (+25% yearly average over 2020), and even more so in early 2022, with January seeing a 41% increase in costs compared to January 2021. In these circumstances, an increase in energy costs and base materials due to both import difficulties and increases in global prices would lead to even higher costs and discourage investment in new construction. The Romanian economy is not strongly connected to that of Russia, Ukraine or Belarus, with imports from all three countries totaling at less than 5% of all imports into Romania in 2019 and exports to them totaling less than 2.5% of all exports in 2019 (last year unaffected by the pandemic, source: NSI). However, there are some segments where trade intensity is much higher: energy and ores. In 2019, 37% of all mineral fuels and oils and 40% of ores came from one of the three countries. Thus, trade difficulties would negatively impact the availability of fuel and materials and, thus, the price of construction.

Brasov, Romania, 3 March, 2022. Photo by Traian Titilincu on unsplash.com

While construction costs impact supply, the other two issues (interest rates and inflation) work together to negatively impact demand. The National Bank of Romania increased the reference rates to 3%: the 5th raise since September 2021. This will have a knock-on effect on the costs of consumer and new mortgage loans, making them more expensive, at a time when the residential real estate prices are highest since 2008 with asking prices for apartments up 20% in March 2022, compared to the same month of 2021 (source: imobiliare.ro). Coupled with record levels of inflation, especially related to fuel, heating and food, this would make financing new home purchases exceedingly difficult, and will push demand down.

Although the non-residential construction market, thanks to the easing of restrictions, was on recovery track, all the previously mentioned factors would hinder recovery. Additionally, the subsector would also have some specific challenges such as global supply chain disruptions due to sanctions, rising energy and transport costs at a time when there is a moderate worker shortage and increased pressure from employees for more remote work options.

When it comes to civil engineering, demand for construction remains high, but the ability of the government to deliver on that demand will be hindered by reductions in the available budget for investment. Increased construction costs make public investment more difficult. The increasing current account deficit, the need for subsidies to counter the effects of inflation and energy costs on the most vulnerable citizens and increased defense spending (to 2.5% of GDP in 2023, from 2% in 2022) are all eroding the public funding available for construction of civil engineering projects. The saving grace of the segment will be the availability of EU funding, however even that will be made less effective by the increases in costs.

Written by Dr. Sebastian Sipos-Gug – Ebuild srl, EECFA Romania

The Romanian construction is poised to grow in both 2022 and 2023. The main drivers of growth vary, including low interest rates and excess liquidity that boost the residential subsector or the use of EU 2014-2020 cohesion funds to help boost civil engineering. At the same time, the pandemic and the responses to it negatively impact construction, mainly in terms of hotel and restaurant construction, but also when it comes to office buildings. The EU Recovery and Resilience Facility (RRF) is another potential source of funding that could help counter these negative effects and maintain Romania’s construction sector on a positive growth rate for the near future.

Detailed construction forecast up to 2023 for Romania is available in the latest EECFA Construction Forecast Report that can be purchased on eecfa.com.

What is the PNRR?

The National Recovery and Resilience Plan (PNRR) contains the projects and measures Romania aims to implement in order to benefit from the EU’s Recovery and Resiliency Facility (RRF). The RRF is a temporary instrument used as a means to mitigate some of the pandemic’s effects on the members’ economies and has a total funding budget of EUR 723.8bln (out of which EUR 29.2bln are available for Romania).

The RRF sets minimum targets for climate spending (37%) and digital spending (20%), which Romania has pledged to exceed (41% and 21%, respectively). Romania’s Recovery and Resilience Plan includes 171 measures (out of which 107 are investments) and has six pillars, mirroring those of the RRF.

How do the RRF and PNRR work?

Out of the total amount, Romania can receive EUR 14.2bln in grants and EUR 14.9bln in loans (this is 13.09% of 2019’s GDP). A pre-financing payment of 13% of each financing source has been granted to Romania, with the remainder of the loans and grants arriving in up to 10 installments, which are themselves conditioned on the achievement of the milestones agreed with the EU in the PNRR. These milestones include several legal, policy and administrative reforms, as well as the completion of investments on time. Thus, the amounts received could be delayed or even rejected if Romania fails to achieve its milestones and targets.

How will this impact the construction segments?

Residential construction

The PNRR has provisions for both new construction and renovation of dwellings. In terms of renovations, the plan has EUR 1bln allotted for improving the energy efficiency of around 4.3mln sqm of residential stock. To put this into context, in 2019, the entire residential renovation market in Romania totaled EUR 800mln (source: NSI). This measure has a deadline of June 2026, and the first step is for the Romanian Government to create a national support scheme (by March 2022) and the local authorities will award the actual contracts.

Regarding new construction, 4418 new units will be built for the housing of young people from vulnerable communities and 1104 new units for teachers and healthcare professionals in areas where access to these services is lacking, such as villages and small towns. The assignment of contracts will again be tasked to local authorities, according to a grant scheme built on national level. The program has a deadline of 2022 for the assignment of contracts and 2026 for the actual construction. The impact of this measure on the construction segment would be rather small, since, for comparison, in 2019 there were 67488 new residential units constructed across the country (source: NSI).

Non-residential construction

The PNRR should impact several types of non-residential construction, but mainly healthcare, education and public buildings.

In terms of healthcare, there are several investments planned:

Renovation of at least 3000 family doctors’ practices by the end of 2023.

124 additional neonatal intensive care beds would be made available through the modernization/extension of 25 intensive care units, by the end of 2024

30 outpatient care units would be built or renovated, also by 2024.

200 community centers would be built or renovated by mid-2025.

And finally, by mid-2026, 25 new hospitals would be partially financed by the program with a focus on the energy efficiency of buildings. This would also cover the required medical equipment.

When it comes to education, there are also several projects planned, including:

300 000sqm of educational spaces to be renovated, another 46 400sqm built with a “green” focus and 3 200 electric school minibuses to be purchased (EUR 425mln),

construction and modernization of 19520 reading places, 6625 canteens and 19130 student housing places for universities (EUR 260mln),

Additionally, 75 000 classrooms and 10 000 labs would be re-equipped across the country (EUR 600mln).

The total budget of these investments in healthcare and education exceeds EUR 4bln if we include the equipment. For comparison, the total expenditure for the construction of healthcare, education and recreational buildings in 2019 was EUR 284mln (source: NSI) so the impact of the PNRR here could be rather large. The renovation of public buildings is also included in the plan with a target of 2.3mln sqm to be renovated with a focus on improving energy efficiency on a total budget of EUR 1170mln and another 1.3mln sqm for moderate renovation (EUR 575mln). For comparison, in 2019 the entire administrative building segment saw less than EUR 266mln invested in renovation (source: NSI), so here, again, PNRR could help grow the construction segment.

Civil engineering

PNRR targets several civil engineering segments as well, with a focus on public utilities, transportation and energy.

In terms of public utilities, the water network would be expanded with 1600km and sewers with 2900km until mid-2026 on EUR 800mln. For reference, in 2020, compared to the previous year, the networks increased with 1500km and 1898km, respectively, so this would in effect be comparable to the current yearly output in this segment. Another focal point is waste management with EUR 1239mln allotted for various investments in waste collection, monitoring and recycling.

Sustainable transportation takes up more than 1/4 of the total PNRR budget, with an EUR 7.62mln allocation. This would include:

EUR 3.480bln for railroad infrastructure – 2426km of rail renewals, 315km of modernized rail and 110km of electrified rail. For reference, in 2019 the value of railroad construction was EUR 185mln (source: NSI).

EUR 3.095bln for the construction of 429km of motorways (equivalent to the amount of new motorways completed between 2012 and 2020). The program will finance several segments on the A1, A3, A7 and A8 Motorways. For comparison, in 2019, EUR 227mln were spent on motorway construction (source: NSI).

EUR 600mln for the metro networks in Bucharest (5.2km) and Cluj Napoca (7.5km).

EUR 620mln for green transport infrastructure – electric vehicle charging stations (52) and urban bicycle lanes (1091km).

When it comes to energy, the focus is of course on renewable and green initiatives:

EUR 460mln for 3000MW of new wind and solar plants and developing battery storage facilities (480MWh). For comparison, the net generating capacity for wind and solar power across Romania in 2021 was 4273MW (source: Transelectrica), so this program would significantly increase production capacities.

EUR 515mln for renewable gas transportation, green hydrogen production and energy storage using hydrogen (1870km distribution pipeline).

EUR 300mln for methane production for electrical and central heating (1300MW).

EUR 280mln for battery and photovoltaic panel production and recycling (2GW worth of batteries /year).

Conclusion

The PNRR’s impact would be maximized by reaching the appropriate milestones and targets on time, and by using this program together with other financing sources, like the national budget or other sources of EU funding.

Thus, if implemented fully, it could have a positive impact across the entire construction sector, from residential and non-residential renovation, to road, railroad and energy related construction.

In January 2020, the World Health Organization started issuing the first warning of a novel coronavirus emerging, and on 26 February the first case was confirmed in Romania. Measures taken to try and contain it led a state of emergency and a lockdown introduced on 16 March. One year later, we can look back at how the residential real estate market reacted to the pandemic and the economic crisis that accompanied it, and we can make an attempt to understand where the market might go next.

To start with, prices on the residential real estate market in Q1 2020 reached their highest value in the past decade and an unease started to permeate the market with flashbacks to the 2008 credit crunch and the massive drop in prices and transactions that followed. This made many developers rush to complete projects before the market collapse, a trend we described in a previous blog post.

Prices did indeed start to drop slightly by Q3 2020, but they remained at a level higher than that of the previous year and by the end of the year the early indicators pointed to a return to growth. This has been pointed out in other markets as well and seems to have impacted a large number of developed and developing economies. However, each country is different, and in the case of Romania, albeit some of the causes of this phenomenon are shared, the outcome and forecast might be different.

Residential forecast is available in the latest EECFA Construction Forecast Report Romania that can be purchased on eecfa.com

Everything is relative and so are prices.

One can wonder if these prices are too high, and if they might grow further or if we’re looking at a potential bubble that will burst in the near future. We previously addressed some of these questions in (yet) another blog post.

Since then, the main factors have changed in light of the pandemic, but it might still be useful to look at the same ratio between income and home prices that we analyzed then and bring it up to date. In 2007, the average net monthly income could buy you approximately 0.20sqm of an average located two-room apartment. By 2017, when we last ran this test, one could buy 0.46sqm with the average wage. For 2019 and 2020 alike, our estimates place this indicator at 0.50sqm and so home prices relative to income actually seemed to be relatively stable.

Why some prices were expected to fall and why they haven’t.

While in general there might be a plethora of reasons for residential prices to drop, in the case of the pandemic-related economic downturn we were initially looking at several factors, somewhat similar to those we saw in 2008, such as unemployment, lower income, higher mortgage default rates, stricter lending criteria, higher interest rates and/or a rush to sell off properties by underfunded developers. In the case of the pandemic, some of these did indeed happen:

Employment did indeed decline between March and November 2020, but only by 2%-3% compared to the same months of the previous year (source: NSI). This was largely due to the employment protection measures taken by the government, which provided incentives to furlough personnel rather than firing them.

Average income rose during the pandemic. Even in April and May, the months worse hit by the lockdown, net wages actually grew by 2% over the same months of 2019 (source: NSI). This was also maintained by the furlough scheme that provided payments of up to 75% of wages for the employees of companies affected by the pandemic.

Loans past due declined. By November 2020, the share of loans past due in total loans was 4.83%, down from 5.46% in November 2019 (source: NBR). Granted, this is still far from the 1.24% average we saw in 2008 but is well within the general descending trend of the previous three years. There was some government support in this segment as well, with the possibility of postponing loan repayments for those negatively impacted by the pandemic, and some banks also took their own measures in this direction.

Lending criteria and interest rates. Lending conditions remained relatively stable while interest rates for mortgage loans declined slightly by November 2020 over November 2019 (-0.5pp, source: NBR). This was partly due to the impact of the tax change in late 2018 that raised interest rates in 2019 over their trend and was later reversed.

Developers had a more secure line of financing. While during the previous recession in 2008 a lot of development was carried out through credit, by early 2020 many properties under construction were pre-sold, and down payments on these provided the necessary cashflow to continue building and even wait longer to find buyers in order to sell at a better price.

Furthermore, due to the reduced spending possibilities with the shutdown of non-essential travel, in-restaurant dining and entertainment venues, spending habits changed. Despite income slightly growing (on average), the saving rate went up and thus by end 2020 the population had a lot more money saved on their accounts, even if the term deposits didn’t go up as much. This high level of very liquid capital can be used to fund residential investments, be it renovation, construction or purchasing a new home.

Where the market is heading.

The longer-term trend of price increases on the residential market continues to be the most likely scenario as demand continues to outpace supply in many of the larger cities like Bucharest or Cluj Napoca. Some potential events would bring merit to a more pessimistic outlook:

Changes in employment and income might be ’ticking bombs’. As said, a lot of the market stability is due to government intervention in preventing mass unemployment and ensuring a minimum income. Once these braces come off, there are genuine concerns that the labor market might see a correction, which would have a negative impact on the residential real estate market. The risk of this is somewhat low, though, since a large portion of those furloughed have returned to work (with some notable exceptions in the hospitality industry), but a small correction could still happen.

Medium- and long-term changes in work trends. With the surge in remote work due to the pandemic measures, one can wonder if this would lead to more structural changes in the way people work in the future. If remote work becomes more common for a significant proportion of people, this will have a massive impact on the residential market. It would lower demand in large cities and increase it in metropolitan areas and smaller cities. This would be somewhat limited in the case of Romania, though, as the country still has relatively large economic segments being less prone to remote work such as manufacturing and construction.

We are already noticing some changes in home buyer preferences. After spending more time at home, either in lockdown or from working at home, home buyers now focus on larger homes, preferably with a yard or at least a large balcony.

Case in point: Cluj Napoca.

Taking Cluj Napoca as an example, the local real estate market is seeing massive demand increases as young people, mainly in the IT field, move to the city to study and take up work. They enjoy higher-than-average income and living in the city gives them proximity to various entertainment and services options, access to a booming labor market, entrepreneurship, and business opportunities. But they also have some major downsides: high rents and residential prices that chip away at their income, gridlocks, light and noise pollution and many other disadvantages of living in a city. With the advent of the work-at-home scheme, they might be more interested in relocating to homes in the neighboring rural area (even more so than they are now) and thus retain a higher share of their wages without the downside of commuting. This would put less pressure on the residential market in the city itself, and lead to lower rents and prices. The city thus becomes less interesting for developers and construction might slow down.

The conclusion.

Despite the pandemic, home prices are seemingly growing. While this might seem strange at first, the actual impact of the current recession on home purchases is limited since the average individual still has their job with a similar or even higher income and is actually spending less of their income on goods and services and thus can afford to save for a down payment.

In the shorter run, the market shows some signs of overheating, but is far from brittle. If the pandemic recovery turns out to be lengthy and there are major changes in the way work is done, it could limit prices and drive them down temporarily. However, if you are holding out in buying a home waiting for prices to collapse, you might be in for a bit of a disappointment.

Written by Dr. Sebastian Sipos-Gug – Ebuild, EECFA Romania

The first quarter of the year 2020, mostly starting with mid-February, was marked by ominous economic forecasts. Thus, some decline in construction activity was to be expected, and indeed newly started construction projects dropped to just over EUR 1.3bln in Q1 2020. This amounts to a 14% decrease compared to the equivalent period of 2019, according to the latest edition of the EBI Construction Activity Report for Romania.

At the same time, the amount spent on construction increased by 25%. Coupled with the record amount of completed construction works (nearly double that of the first quarters in each of the previous 5 years), lends us to the conclusion that investment was increased in order to rush and complete the (at the time) ongoing projects, before the anticipated negative economic impact of Covid-19 took place.

Covid-19 changes in reporting frequency

In light of the Covid-19 pandemic and the accompanying economic impact, the data visualization for EBI Construction Activity Report is currently updated on a monthly basis, rather than quarterly.

Renovation activity increases in building construction

Building constructions started for the first quarter of 2020 dropped by 3% over the same period of 2019. However, the amount of new building construction for Q1 2020 is actually higher than in the first quarters of 2014-2018, and thus this small drop is more due to the good performance in 2019 than a clear sign of decline for 2020.

Looking at renovation figures, however, we can notice a somewhat new trend: that of increased renovation activity. While new building construction can, and in some cases was, pushed back due to uncertainty regarding the economic conditions, renovation works are less prone to this effect since they are more urgent in nature. Furthermore, as government measures started to be implemented in March, individuals and businesses alike needed to make adjustments to their living and working conditions: spaces were converted to quarantine centres, offices and industry alike had to adapt to new conditions and started to ensure layouts that allow more social distancing, hospital wings were relocated and so on.

Civil engineering output exceeds expectations, but low activity starts caution about future

The first quarter of 2020 saw an estimated expenditure of EUR 804mln on civil engineering projects, exceeding any single quarter since data aggregation started in 2014. The high level of output achieved came with the completion of many ongoing works and comes with a significant caveat: the quarter was also markedly worse than the previous year in terms of Activity Starts, with a 38% drop over Q1 2019. The most notable drops in new projects were in the segments of road and public utilities. Both reportedly had quite an increase in output over the same period, and thus the focus here seemed to be completion, rather than starting new projects.

Regional disparities in new construction activity

Despite the national-level decline in new activity, a large level of regional disparity can be noticed. The Center, South and West regions are showing an actual increase in construction starts compared to Q1 2019 in several segments, moving against the overall trend of the country. This could be an indicator of the higher level of resilience of local construction markets and a higher investor confidence in local economies. These regions might also be tardier in their response to the anticipated crisis, but it’s something to keep an eye on in the future and more data will show how resilient they are.

EBI Construction Activity Report

The EBI Construction Activity Report is a quarterly publication that relies on the project information database of iBuild and is prepared by Buildecon and Eltinga. It comprises an analysis of projects based upon several object types: multi-unit residential construction, non-residential (further split into 9 segments) and civil engineering (split into 8 segments). The report offers information about the number and value of projects started or completed, and an estimate of the total amount spent on each segment in that quarter. If you would like to receive a data visualization for the EBI Construction Activity Report free of charge, please write to us at the ebi@ibuild.info e-mail address.

Written by Dr. Sebastian Sipos-Gug – Ebuild, EECFA Romania

UPDATE ON 7 MAY 2020: from May 15 on a “state of alert” will take over the “state of emergency”. People will be allowed to move freely within localities without having to declare their destination, but only in groups no bigger than 3 people. Movement restrictions in towns under quarantine will remain in force.

Timeline

26 February: the first confirmed case reported in Romania

11 March: schools closed

16 March: the Romanian president issued a state of emergency, granting the government enhanced emergency powers to cope with the pandemic. At the time Romania had 168 confirmed cases and no deaths.

17 March: restaurants closed, and all public gatherings and events suspended

21 March: shopping malls closed

22 March: first death attributed to Covid-19 reported

On 24 March a state of lockdown was announced via military order and the population was restricted from moving freely outside of home, with several exceptions (work that cannot be done remotely, essential shopping, assisting the elderly, medical emergencies, walking pets, personal exercise in the proximity of the home, volunteering, agriculture). A proof for the valid reason for leaving home is required, with citizens asked to produce a personal statement prepared before leaving the home and/or to have a proof of employment. Elderly citizens (65+) were further restricted, being allowed to leave the home only for 2 hours per day (11:00-13:00). However, retailers were instructed to provide preferential service to them during this interval.

On 15th May, the State of Emergency is up for revision. However, even in the event of it being lifted, some restrictions are to remain in place, like the interdiction on festivals and large gatherings and the mandatory use of face masks in public spaces and on means of public transport.

Construction Works

While the lockdown significantly reduced the mobility of persons, it provided little restrictions in the range of work activities that could be done (dental work, non-emergency medical interventions, hospitality and in-house food service).

As of the writing of this article, there have only been a few major construction works delayed and, anecdotally, some projects are in fact moving faster than scheduled, such as bridge and road construction, taking advantage of reduced traffic. DIY works are also reported to be ongoing, with furloughed workers from other industries taking advantage of the time at home to engage in renovation works, with a noted increase in online sales of DIY retailers.

The new EECFA Romania Construction Forecast Report is planned to be issued on 29 June 2020. Sample report and order

Factors limiting the construction sector’s performance

The direct impact on the ongoing construction activity has been minimal since no restrictions were in place specifically targeting construction works. Recommendations regarding social distancing were given, but not mandated. Several indirect factors, however, were expected to limit the amount of construction activity:

Initial concerns over construction material availability have been raised. However, as of yet, no major shortages have been reported. Some manufacturers noticed a reduction in direct sales to individuals, however, B2B material sales have continued at comparable levels and online sales have increased.

Occasional worker shortages have been reported, as some workers have taken medical leave or used vacation days, especially in the early stages of the lockdown. Fortunately, no major shortages have been reported due to the infection.

At the same time, other companies have had to let employees go, with 37.750 work contracts in construction having been terminated from the start of the emergency period as of 29th April.

Lack of interest in investment is expected, especially in the hotel and restaurant segments, which will likely reduce demand in the current year. With slim changes of reopening for the summer season, tourism related construction is expected to be postponed.

Trends in office construction are also expected to change, with working from home on the rise and open office plans under scrutiny.

Lack of public funding could have a major negative impact on construction activity once the initial blow of the pandemic passes. Many county governments and city halls have used a large portion of their investment funds for measures aimed at reducing the spread of the virus, and thus there remains little for projects like infrastructure development or renovation. On national level, according to several governmental agencies, public deficit is set to reach 6.7-7.3% of GDP in 2020 and economic growth is to be stunted, with a decline of at least 1.9-4.7% of GDP.

Lack of private funding is also a major concern, with many companies losing significant resources and burning through their savings and credit lines.

At the same time, more than 1 million Romanians have had their work contracts suspended and 270 thousand lost their jobs since the state of emergency was instated (as of 29th April) and thus their spending power would have been significantly diminished.

Real estate transactions are showing signs of slowing down, with March 2020 seeing 4.6% fewer houses and 11.7% fewer apartments traded compared to the previous month. The market remained 8.5% more active than March 2019, however.

Anticovid measures in construction

There are no specific measures announced, as of the time of writing this article, aimed to supporting construction. However, there are some measures that could, indirectly, help:

The government is providing the resources to pay 75% of the initial wage for those with suspended contracts, helping public consumption remain afloat, with a positive impact on companies trying to retain qualified workers and maintain their cash-flow.

A RON 15bln program to support small and medium enterprises (“IMM Invest”) was launched on 28th April, providing state-backed loans for investment and working capital.

EUR 750mln have been allotted from EU funding for Romania for supporting small and medium enterprises, with a further EUR 300mln for assisting workers with suspended contracts.

The government’s economic recovery plan takes into account using infrastructure construction to boost the economy (which would increase the deficit even further). However, as of the writing of this article, no plan has been approved, and so the impact it would have cannot be assessed.

The government backing of mortgage loans for first time home owners is expected to continue into 2021, rebranded as “One family, one home” (Romanian: “O familie, o casa”), which should help counter some of the negative effects on the residential market. Its impact on the market diminished in 2019, with regular loans becoming almost as affordable, but it comprises a large portion of the segment nonetheless, since the programme covered 45% of all ongoing mortgage loans in March 2019.