With the latest governmental decision, the number of projects in designated rust belt action areas reached 81 in Hungary. Estimated 46 thousand dwellings1 is to be built on these brownfield sites. The sole purpose of this post is to follow these projects and to see how they will or will not help the recovery of the new residential construction sub-market in Hungary.

Status on 28 January 2026. The upswing has not been too intensive lately, but many XXL projects have moved closer to under construction status. — Completed: 3 620 dwellings Under construction: 10 484 dwellings Before construction: 26 149 dwellings

Brief background

Rust belt action areas (let me shorten them to rusty) are practically brownfield areas with special benefits. The owner of the site or the developer should initiate the process (with specific development plans) and there is a Committee to examine if the proposed site is entitled for the rusty status. Based on the opinion of the Committee, the final decision is made by the government. The decisions (about the exact sites) are announced in a decree and the special benefits coming with it are:

priority investment status, meaning e.g. faster permitting procedures2,

newly built homes can be sold at 5% VAT without limitation in time3,

By the current regulations, it means a min. 5% and a max. 27% price advantage over competitors developing on non-rusty area until 2030 (depending on when the permit was obtained) and a 27% price advantage from 2031 on.

Our focus

What we do is to turn the mentioned decree into information we need for forecasting. With the help of Eltinga Building Permit Monitor database and the iBuild project information database, actual projects are identified from the lot numbers specified in the decree. Among all the general project specifics, the number of dwellings (where it is known), are attached to these projects.

The map shows the stages of the housing projects that were given rusty status. Bluish dots are those before construction, neon yellow dots are those under construction and the dot disappears once the project is completed.

OK, it is very convenient to see projects on a map, but our focus is more on the chart under the map where the yellow is the number of homes under construction.

What we are curious about is if and when the right end of the yellow curve shows a strong upturn.

In other words, we are curious whether the regulation ignites a recovery or not. As of now, it is more common that the yellow line has increased because projects having started in the past were given the rusty status. (So they were just re-qualified, it did not mean new project starts.) In parallel, it is less common that projects start after they were given the status. Just two extreme examples for these: Unipark Buda has been under construction since 2019 and it got the rusty status at the end of 2023, while Láng quarter was given the rusty status in 2021 and it is still before construction.

The charts will be updated quarterly, so check back if you are also curious.

Another way we like to look at it is a list. Here we do not separate the projects to phases (like on the map) and it gives a quick understanding on how each rusty project moves ahead from 1 February 2024 on.

Data sources

The data mostly come from Eltinga Building Permit Monitor (in Hungarian: Építési Engedély Figyelő). This is a very detailed database on before construction multi-unit housing projects in Budapest. It is aiming primarily at developers who would like to understand the competition. For further information on this, please turn to Mr Zoltán Sápi, Eltinga, sapiz@eltinga.hu. Besides, we use the iBuild project information database.

This is an estimation based on the median size of those rusty projects where the number of homes were announced ↩︎

There was no construction start indicator in Romania, so we have created an estimation for it.

This poster is a summary of our monthly findings. It shows how the total value of started construction works have changed over the same period last year. Besides, it presents which segments have the biggest start value in the current year. We call this indicator Activity-Start. And they are computed every month for 18 construction segments by aggregating data of construction projects. The projects are from the iBuild database and ELTINGA and Buildecon found the way of creating indicators out of them.

If you need short-term foresight, you will like it.

Brief comment from Janos Gaspar, head of Buildecon:

Activity-Start of building construction dropped massively in 2025. Both the residential and the non-residential submarkets are in red, but residential looks less bad. These are not the final results, though, as Q4 figures are still ‘very’ preliminary. There was a drop in civil engineering, too. With more than 6-billion-euro worth of started works, however, 2025 is still considered to be a very good year. It is just that it was not as exceptionally great as 2023 and 2024.

Every month this poster will be available here on our blog. If your interest is deeper, we have the EBI data visualization (with indicators for all the 18 segments of the construction market), updated monthly and we have the EBI Construction Activity Report Romania (with data and explanations), published quarterly in English and in Romanian. All these are packed into a yearly subscription. For the specifics, please contact us.

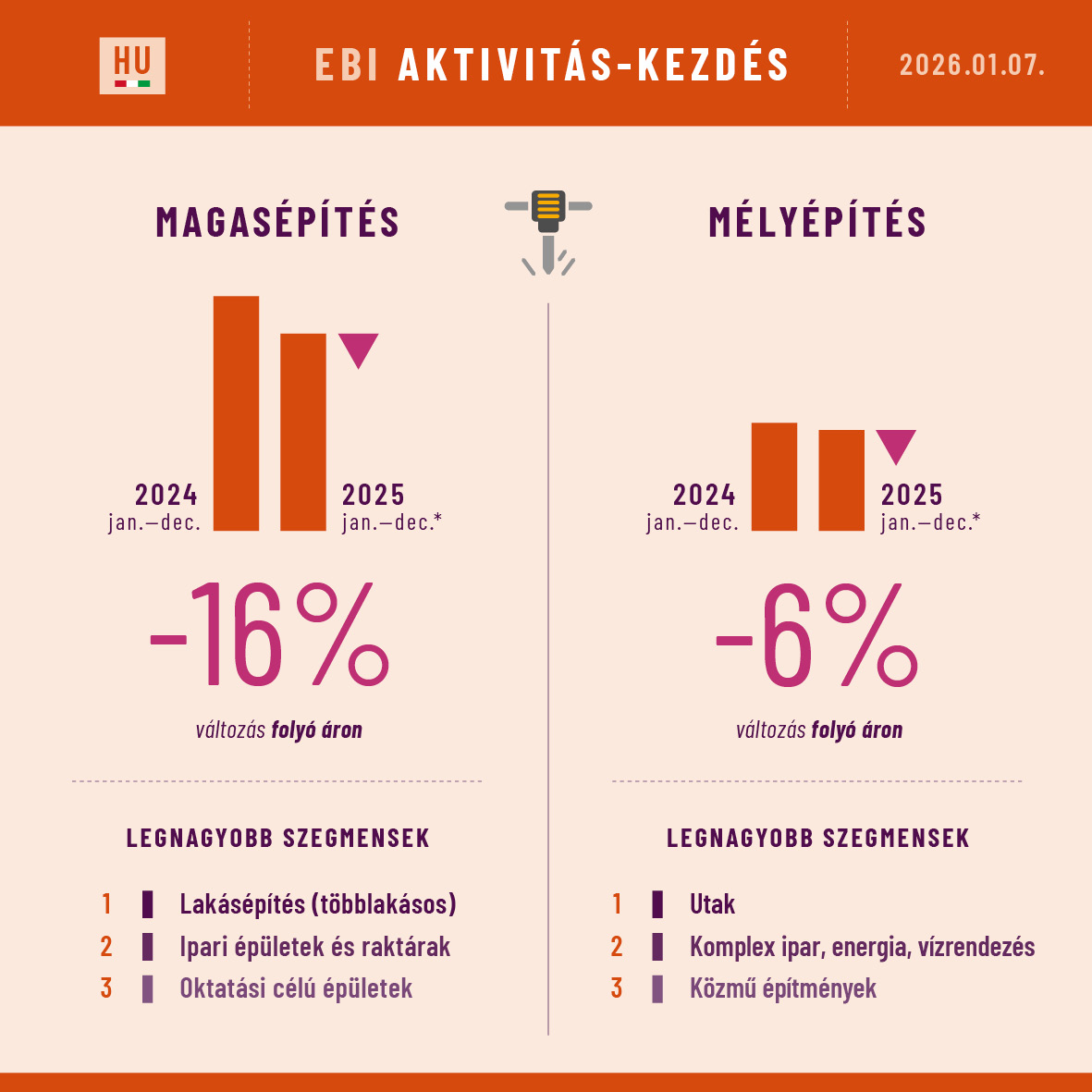

Az év vége nagyon gyenge lett a társasházi lakásépítés részpiacon, de 2025 egészében még így is megduplázódott az Aktivitás-Kezdés 2024-hez képest. Ezzel szemben a megkezdett nem-lakáscélú projektek értéke hatalmasat esett a tavalyi évben. Ezen a részpiacon nagyon tartós a visszaesés, három éve folyamatosan csökkenést mérünk. A mélyépítés 2025-ös Aktivitás-Kezdése lényegében megegyezik a tavaly előtti (és az előtti) év alacsony szintjével.

A poszter a két nagy építési részpiac Aktivitás-Kezdés indikátorának időszak/időszak változását mutatja, valamint a szegmenseket amelyekben a legnagyobb értékben indultak kivitelezések. Ezt a posztert minden hónapban kitesszük ide a blogunkra. A teljes építési piacot részletesen bemutató EBI Építésaktivitási Adatvizualizációt (összesen 18 szegmens adataival) is havonta frissítjük, és negyedévente az EBI Építésaktivitási Jelentésben is elmondjuk, hogy mit látunk a piacon. Ha érdeklik a részletek akkor a contact oldalon írjon nekünk.

The end of the year was very weak in the multi-unit residential submarket, but Activity Start in 2025 (as a whole) still doubled compared to 2024. In contrast, the value of started non-residential projects fell dramatically last year. The decline in this submarket is very persistent; it has been going on for three years. The Activity Start of civil engineering in 2025 stayed at the same low level as in the year before (and in the year before that).

The poster (above) shows the period/period changes of the Activity-Start indicator in the 2 main submarkets and the segments with the largest value of started works. This poster is published every month here in the blog. The EBI Construction Activity Data visualization with the details on the whole construction market (with altogether 18 segments) is also updated monthly and the EBI Construction Activity Report, summarizing what’s happening in the market, is published in each quarter. If your interest in construction markets is deeper, please contact us for the details.

The viz was updated on 29 November 2025 and it is great to see the recoveries here and there. The text will be updated as soon as we have all the permit data (Ukraine Q3 is missing now).

When it comes to permits, Croatia and Serbia are still very stable. Both countries experienced massive expansion between 2014 and 2022 and they have remained close to their peak every since. Croatia has had around 4 million, while Serbia has had above 7 million permitted m2 for three years. Q2 in Slovenia was not soo good, so it remained well below the peak reached in 2022. Bulgaria is also below its latest peak, but permit data of the latest 3 quarters depict a growing optimism. In Romania the mild recovery is ongoing, led by the residential submarket. Hungary also turned upward, also because of the residential permits. The non-residential submarket looks very bad. Permits have fallen back to the level experienced in 2015.

You may use the dropdown in the viz for selecting either the residential or the non-residential submarket, or both.

In the full visualization, not only permit but completion data can be followed (where available).Just click on the Country-by-country sheet.

Led by the residential submarket, Türkiye bounced back and up. And due to changing accounting method, all permit time series from 2010 have been revised. From Q2 2025 on, permits issued by authorities other than the municipalities are also reported by TUIK. So the scope is bigger, the results show the full picture. Click through the below viz for understanding the size and the impact of this revision. Mild optimism prevails in Ukraine, the permitted floor area keeps expanding. Since the beginning of this year the residential submarket drives this growth. Russia is stable when it comes to completion of buildings. Non-residential has been edging up, residential has been edging down lately.

Written by Tünde Tancsics and Dóra Barát – ELTINGA-EECFA Research

Similarly to every summer, this summer too we have looked at how the European Commission sees our countries. Here is how GDP, investment and construction investment forecast have changed in the past half year.

Between Autumn 2023 and Spring 2024 economic outlook has improved for the majority of countries in the Eastern and Central Eastern European region (EECFA countries) for 2024-2025. Exceptions only included Türkiye, Romania and Hungary (this latter is covered by Euroconstruct), but the deterioration of the outlook was minimal. Expected GDP growth also decreased in case of the EU and the Eurozone.

Economic growth in the examined countries is expected to be between 2.3% and 3.9% by 2024-2025. The largest GDP expansion is related to Serbia, while Russia’s economy may grow least. At the same time, the expansion in the countries of the region is set to be much higher than in the EU and the Eurozone where projected GDP growth is only 1.1% and 1.3%, respectively.

Projected gross fixed capital formation (GFCF) growth rate for 2024-2025 sank in the majority of the countries by Spring 2024 from the previous level in Autumn 2023 with the only exceptions being Russia and Serbia. In Russia, a slight increase was seen from Autumn 2023 to Spring 2024. Prospects in Serbia significantly improved and next to Romania, its growth rate became the highest (6,45%) in the Eastern- and Central Eastern-European region (EECFA countries).

Expected GFCF (investment) growth is also high in Hungary, 4.9%, while for the other countries in the region, projected GFCF increase in 2024-2025 is between 3.05% and 3.6%. In the EU and the Eurozone, a much more modest expansion is estimated than in the region; GFCF prospects decreased from Autumn 2023 to Spring 2024, and they are only 1.15% and 0.85%.

Growth rate for investment into construction for 2024-2025 improved in Croatia, Hungary and Bulgaria, while in Romania, Slovenia, and in the EU and the Eurozone the outlook deteriorated from Autumn 2023 to Spring 2024. When it comes to the EU, growth is foreseen to be close to zero, whereas in the Eurozone a slight drop is projected for 2024-2025. The predicted growth for investment into construction in Spring 2024 was the highest in Romania (8.05%), followed by Hungary, Bulgaria, Slovenia (between 4.1% and 4.4%) and Croatia (2.45%).

This above represents the Commission’s view and it is different from ours at some point. It might be because our focus is exclusively on construction. For each segment we come up with an individual story and this is how the total construction market is formed. The latest predictions are in the 2024 Summer EECFA Construction Forecast Reports. Sample report and order: eecfa.com

As we see, Türkiye and Croatia could be top performers, while Russia and Romania are forecast to shrink. Although the Ukrainian growth rate is impressive it is because the market is coming back from a very low level.

In terms of permit, there has been no sign of pessimism so far in the SEE countries. Right the opposite. Croatia, Serbia, and Slovenia are all expanding. Bulgaria peaked with 9 million permitted residential plus non-residential sqm in Q3 before correcting downward in Q4 and Serbia is beyond 7 million sqm. The biggest country, Romania, stayed close to its peak in the meantime.

Permit recovery in Turkey has stalled, and continuous growth in non-residential cannot compensate the pessimism in the residential submarket. The current level of around 140 million sqm is still less than half of the all-time high reached in 2017. Ukraine’s stat office managed to publish permit and completion figures for the whole 2022. The non-residential permit figs are about 60% less, while residential is 50% less than in 2021. (You may go to Country-by-country sheet from completion and choose quarterly from the observed period dropdown. By default you will see the latest 4 quarters together data)

In the coming months the rest of the countries will publish their Q4 data and we will update the chart, so please check back.

The Permit-Completion visualization contains data on 8 EECFA (Bulgaria, Croatia, Romania, Russia, Serbia, Slovenia, Turkey, Ukraine) + 1 Euroconstruct country (Hungary).

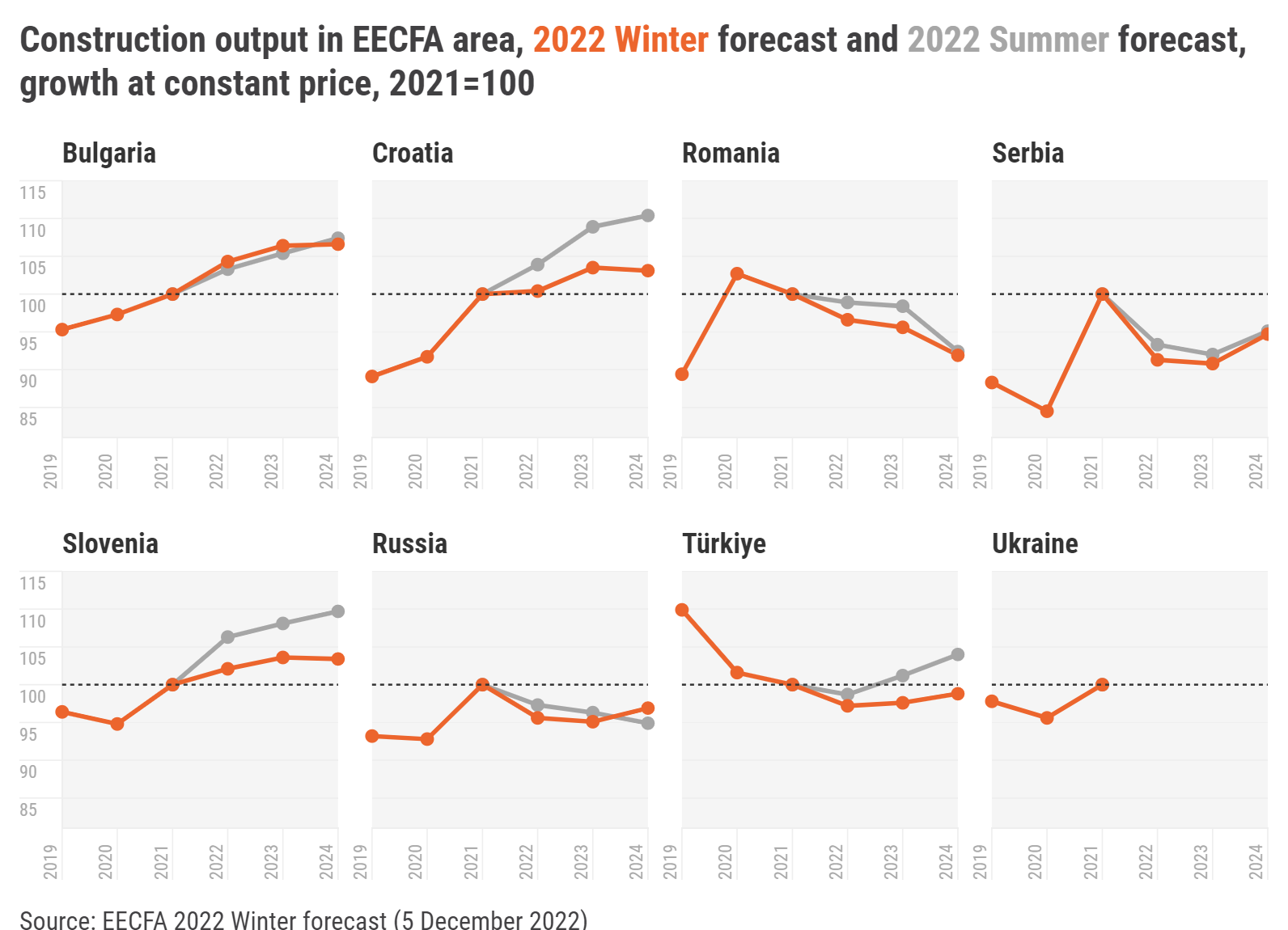

EECFA’s 2022 Winter Construction Forecast Report was released on 5 December. Full reports can be purchased. Discounts and sample reports: info@eecfa.com. EECFA (Eastern European Construction Forecasting Association) conducts research on the construction markets of 8 Eastern-European countries.

Yet another downward revision characterizes the forecast for both regions. Southeast Europe could see shrinkage on the horizon. This, however, comes after a great period of construction in between 2016 and 2021, so the market is foreseen to come down from a peak level. In this respect, the 3% decline until 2024 is no drama, in EECFA’s view. The drama is in East Europe where the peak was reached in 2018 and the market was around 10% below that peak level even before the Ukraine war began. Since then, EECFA has paused issuing forecasts in Ukraine and a status report has been prepared. Without Ukraine, the region is expected to reach its bottom in 2023.

In Southeast Europe, almost all countries have been revised downward. Three out of them, however, could see expansion until 2024. The foreseen contraction in Romania and Serbia pulls down the region to negative. Romania is quite pessimistic; the market could shrink by almost 10% by 2024. Serbia is expected to witness a sizeable drop, too, before growth returns in 2024. As the region saw much construction in 2016-2021, the market will likely decline from the peak, making the 3% drop on the forecast horizon not-so-drastic.

Bulgaria:

Under the projected economic slowdown, construction will increasingly be affected by the ongoing political instability that is likely to undermine reforms within the Recovery and Resilience Plan, and delay implementation of the EU’s operational programmes.

Тotal construction output is estimated to have grown in 2022.

For 2023-2024 civil engineering is forecasted to increase at a more accelerated pace.

Croatia:

Residential construction output held up in 2022, impervious to war and disease. But it’s likely residential’s rapid growth will over time succumb to rising prices and a falling population.

Rail construction output will rise as more rail projects come online. Some new high-cost road projects may yet be undertaken for political reasons.

Energy prices will fuel building of oil/gas port facilities, pipelines and storage in 2022-2023, construction that the EU’s green-energy push may quench in favor of renewable energy and power grid projects.

Romania:

The Romanian construction market is set to shrink slightly in 2023 and 2024 as internal and external factors conspire to make building materials more costly.

Inflation-induced lower purchasing power and growing mortgage interest rates are making loans more expensive, and few people can afford to buy a home in cash.

On the one hand, Romania could benefit from the current global instability and attract more foreign investment to grow its economy. On the other, increased energy costs translate to higher operating and construction costs and discourage investment.

Serbia:

The challenging economic situation will undoubtedly have negative effects on construction outputs. But how negative is the question of external factors and the coming events.

The domestic market is strong, with high public and foreign investments, as well as record employment. The highest economic risk comes from inflation and the expected recession in the EU.

The current economic slowdown could deepen the contraction in case of a prolonged crisis.

Slovenia:

Slovenia has experienced expansion in construction output on the back of the strong overall economic growth.

However, risks for the future include high inflation, large construction cost increases, and overheating economic growth. And increased interest rates will depress residential output in the future.

Supply chain constraints might jeopardize the completion of large civil engineering projects.

In East Europe, 2022 could be the 4th consecutive year of drop in Türkiye, and no quick recovery is foreseen on the horizon. We have turned somewhat optimistic in Russia, but only from 2024 on. Without Ukraine, the region will likely hit bottom in 2023. The region reached its peak in 2018 and just before the war in Ukraine started, the market was around 10% below this 2018 level. Owing to the war, Uvecon, the Ukrainian member institute of EECFA, has prepared a status report for the second time instead of the forecast report.

Russia:

Direct and indirect effects of sanctions hammered the construction market that declined faster in 2022 than previously expected.

Forced acceleration of projects in transport and energy, in response to export and import structure changes due to sanctions, will spur growth in civil engineering.

Many targeted programs and national projects will support the construction sector throughout the forecast horizon.

Türkiye:

The construction industry has been trying to deal with high inflation that has led to 120% yearly rise in construction cost and 189% increase in housing prices.

There has been some deficit between produced and needed home numbers since 2000, augmented by the influx of refugees from Syria and neighbouring countries (3,920 million registered; unknown unregistered).

The low-cost housing project of the government as of September is expected to stop the current slump in the construction sector.

Ukraine:

Prospects for construction depend on the existing situation on the market as a result of the destruction of residential, non-residential and engineering infrastructure, and the end of hostilities with the possible economic recovery.

Total area of damaged or destroyed housing is 74.1 million sqm (7.3% of the total area of Ukraine’s housing stock), a number which, unfortunately, grows every day. Restoring the housing stock will become a key issue for Ukraine after the war ends.

Energy infrastructure remains the top priority for recovery, as nearly 40% of the energy system has been destroyed.

I see the current situation now as a combined supply-demand shock for the region’s construction market. This could be true to each EECFA country, but UA and RU are not in the position to be discussed right now. So, this is my framework of thinking:

Supply side shock (on product market) causes cost increase

supply chain issues for UA, RU (and China) construction materials (sanctions, war, transit problems)

energy, fuel price hike

FX rate

Combined supply and demand shock

Demand side shock causes delayed / cancelled construction investment

decreasing real income

tightening monetary conditions

decreasing confidence

decreasing corporate profitability

uncertainty

high geopolitical risk

new pressures on budgets (refugees, energy, fuel price compensation)

The negative demand shock could be counterbalanced in some segments of construction in mid-term if business operations (services or production) have to be relocated from UA and RU. These could affect industrial building and warehouse, and office segments positively.

Besides, new demands could arrive for strengthening the defense industry, and investments aiming energy-security and energy-efficiency could also be prioritized and supported by policy measures. These could affect industrial buildings, energy production and transmission, and residential renovation segments positively.

And these factors can be considered for understanding country-specific impacts:

exposure to trade with UA and RU (general, construction materials)

exposure to RU energy

exposure to war

exposure to RU financing

exposure to financial shocks (banking system, monetary policy regimes)

non-EU members relations with Russia

current cyclical position of a given construction market

The (fiscal and monetary) policy responses to these shocks will set the final picture.

EECFA’s 2021 Winter Construction Forecast Report was released on 6 December. Full reports can be purchased, and a sample report can be viewed here: www.eecfa.com. EECFA (Eastern European Construction Forecasting Association) conducts research on the construction markets of 8 Eastern-European countries.

We are more optimistic for 2022 in the Southeast European region of EECFA than in the previous forecast round. The drop in 2023 is caused by Bulgaria; the awaited shrinkage is so sizeable there that expansion elsewhere in the region might not counterbalance it. Expansion in the East European region of EECFA is foreseen to be smaller both in 2022 and in 2023 than in the previous forecast round. Growth in Turkey was revised downward.

The largest Southeast European construction market of EECFA, Romania, is expected to see only moderate growth on the horizon. Serbia, having recorded the biggest expansion of almost 100% in the 2014-2020 period, is foreseen to plateau in the upcoming years. In Eastern Europe, in Turkey we maintain to believe that the recovery could start, but we lowered our growth expectation compared to our previous forecast. After 2 years of no-growth, Russia’s construction market is foreseen to expand gradually until 2023.

Bulgaria. The Bulgarian economy is recovering more slowly than expected, and the likely growth rate is 3.8% in 2021. However, residential construction looks strong thanks to low interest rates on housing loans, making home purchase more affordable. Real estate is also the safest and easiest way for those wanting to invest to avoid negative deposit rates. The pandemic and its lasting follow-up effects played an additionally strong cooling effect on non-residential construction because of a surge in office and industrial construction earlier and with an emptying pipeline. Zero progress on big-league infrastructure projects will take its toll on growth in civil engineering construction in 2021, but it is set to catch up in 2022. Total construction output in Bulgaria is anticipated to grow by 6.5% in 2021 and 16.5% in 2022. The lack of preparation for the new programming period 2021-2027 and the National Recovery and Resilience Plan are to negatively affect total construction output which is expected to drop by 24.9% in 2023.

Croatia. Croatia’s tourism season surpassed all expectations, driving a 16.2 percentage point swing in the country’s GDP growth, from -8.1% in 2020 to +8.1% this year, and a one-notch jump in its Fitch rating, to BBB. The near-term future of Croatia’s construction sector now depends greatly on the evolution of the COVID-19 pandemic, particularly its effect on tourism. EU and international financial institution crisis-relief funding will, though, soften any blow that the disease delivers. The City of Zagreb’s budget crisis, bureaucratic delays in spending crisis-relief money and much higher construction costs are other negative factors that will affect the growth of construction output, which must be assessed not for the sector as a whole, but segment by segment (e.g., hotels vs. residential).

Romania. The economy is expected to return to pre-pandemic levels, in terms of GDP, by the end of 2021, after growing 7% in real terms. The European Commission forecasts Romania’s GDP growth rate to stay above the EU average in both 2022 (5.1%) and 2023 (5.2%), and, with the help of the Recovery and Resilience Facility (RRF), construction would have a positive ground to grow upon. Total construction output in 2021 is predicted to slightly decline (-0.3%), but to recover and grow in 2022 and 2023. Low interest rates and excess liquidity coalesce into an expanding residential subsector, while non-residential construction continues to be impeded by pandemic-related changes to work habits and various restrictions. On the back of the RRF and the 2014-2020 EU cohesion funds, and despite ongoing difficulties and delays in implementing projects, civil engineering construction continues to have a high potential for growth.

Serbia. After the restrictions in 2020, economic recovery came faster than expected and GDP growth is estimated to reach at least 7.3% in 2021. This strong rebound is supported by accelerated construction activity and increased capital investments, where a high single-digit expansion is projected in 2021 outputs. Construction output is fuelled by civil engineering projects, but also the robust residential and industrial related constructions. Furthermore, budgetary expenditures for investments are planned to reach record levels, with 7.5% of GDP dedicated for this purpose in 2022. All indicators are pointing towards more extensive growth and sustained construction activity at record levels in this forecast horizon.

Slovenia. The Slovenian economy has rebounded stronger than expected after the pandemic. One of the strongest economic growth accelerators was gross fixed capital investment, causing construction output to get back on feet. Total construction output is projected to exceed EUR 4bln sooner than previously predicted – already in 2022 – and reach EUR 4,3bln in 2023. Construction cost growth will probably slow down from a hike in 2021, resulting in a more stable construction environment without supply shocks. This will enable several big civil engineering projects to continue apace, but the main contributor to construction output will be new residential projects. Of course, our forecasts remain contingent on the condition that no further lockdowns hinder the overall economic activity.

Russia. The construction industry in Russia is going through the second year of the pandemic relatively successfully, and the previously expected stagnation in 2021 is likely to turn into a 3.2% growth by the end of the year. This unexpectedly good result was enabled by segments with traditionally active government participation: residential and civil engineering which were supported by large funds. The non-residential subsector also contributed to the growth of the construction market in 2021, mainly due to the massive completion of objects whose construction was previously postponed from 2020. But because all these factors are temporary, construction market growth in 2022 and 2023 will lessen and is prognosticated to post +1.9% and +1.2% per year, respectively, as a part of the potential for the positive dynamics was already exhausted in 2021.

Turkey. The Turkish economy started to regain senses from the pandemic blow in Q3 2020, which continued with high GDP growth in Q2 2021. Although Turkey removed most COVID-19 related restrictions on 1 June 2020 with the elevated number of vaccinations, now, like across Europe, the fourth wave of the pandemic has started (yet with relatively fewer new cases). The estimated economic growth rate by end 2021 is about 10%, but the primary concern in recent months has been high inflation caused by the national currency’s devaluation. Building starts expanded greatly, but completions registered a small drop in the first 9 months of 2021. The government requires interest rates (also for mortgages) to be kept at less than half of the rate of rise in building construction cost. Keeping real incomes positive during high inflation times is important for demand for commodities like housing and other real estates. Turkey’s total construction output is prognosticated to be positive in the forecast horizon with an average growth of 2.6% up to 2023.

Ukraine. For the construction sector in Ukraine, 2021 marks the year of completion of the construction regulation reform launched back in 2019. In mid-September, the newly created State Inspectorate for Architecture and Urban Planning began to work as a full-fledged new body with its own structure, powers, and new work principles. Ukraine’s construction market in H2 2021 has showed a good recovery in investment activity and the resumption of construction. The residential subsector remains the driver of the construction sector due to stable demand from the population. The main constraint in the development of the construction market in 2021 has been increased construction costs despite the active implementation of residential projects against the backdrop of the revival of mortgage lending, increased demand from the manufacturing sector, as well as high volumes of financing.