EECFA released its 2025 Winter construction forecast on 12 December. Check out a sample report and place your order on eecfa.com. For discount, please contact us.

Southeast European construction markets

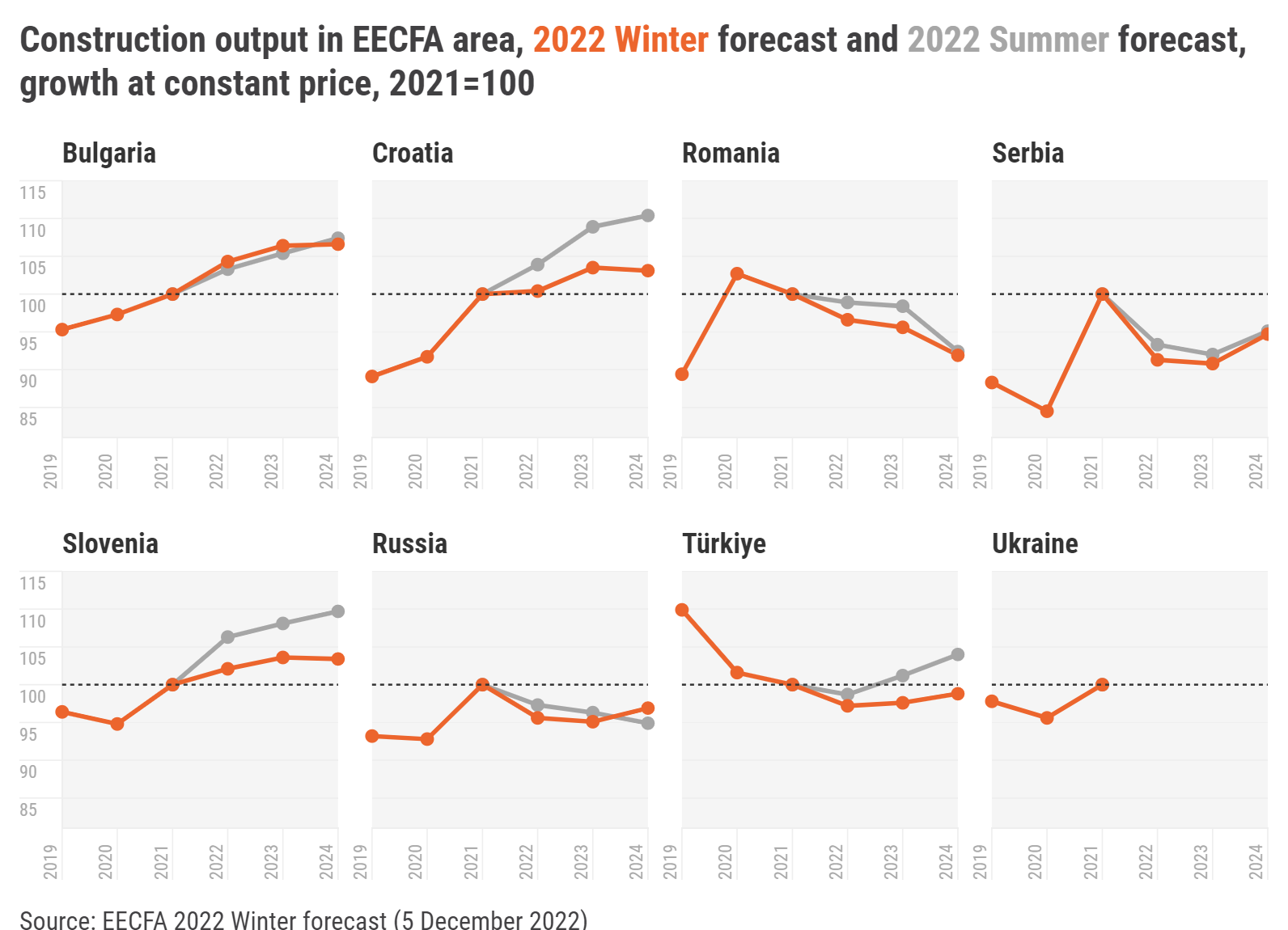

“Bulgaria’s total construction output is forecasted to increase by 3% on average for 2026-2027” – says Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian research institute. He adds that this is to follow estimates for a similar performance of almost 3% in 2025. The sectoral background, however, shows, a nuanced picture – cooling of residential construction, positive news from non-residential and a robust performance of civil engineering. The latter will benefit from investments which will be backed by the absorption of EU funds through the Recovery and Resilience Plan (RRP) and classical operational programmes, both with implementation deadlines in 2026 and 2027. At the same time, Bulgaria’s economy is to expand by 2.4% on average in 2026-2027 – a period continuously shaped also by the Euro adoption on 1 January 2026.

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members, think that declining dwelling sales in Croatia have, paradoxically, failed to stop the growth in the value of Croatian residential output, because increases in the price per square meter of those dwellings that do get sold have more than compensated for the lower number of square meters bought. “But how long this can continue is unclear” – they add. “The policies that the Croatian government is implementing in order to ease the country’s housing crisis are confusing the residential picture still more, since a number of those policies have contradictory effects on output. As to non-residential building construction, output growth during the period covered by the current forecast will depend greatly on the sector, with some likely to continue to benefit from catch-up growth and EU support for a bit longer and others moving toward a steady state or even a decline. In civil engineering, EU funds continue to play the dominant role in financing construction of all sorts. Sports facility construction is experiencing a boom, but given the speed with which such projects are completed, the effect on output will be relatively brief. Renewable energy construction should be growing rapidly, but regulators’ hostility toward the sector are holding it back.”

“Romania’s economy is entering a challenging period as the recently implemented measures to reduce the national account deficit begin to take effect” – reports Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild. “While most forecasters do not anticipate a recession, economic growth is expected to remain subdued over the next two years. Inflation is the highest in the EU, boosted in 2025 by increases in sales taxes. As a result, consumer prices are rising at a pace that is forecasted to outstrip wage growth, leading to a decline in real incomes in both 2025 and 2026. Government spending is also facing cuts, thus both private and public consumption are predicted to decline, with a chilling effect on most construction activity types. There is also the challenge of the massive level of public investment required by civil engineering projects that have started since 2023, which will be difficult to sustain under the austerity and the mounting pressure of losing even more EU funding. On the brighter side, both the economy at large and the labour market are expected to be quite resilient. By 2027, assuming the deficit reaches manageable levels, the effects of contractionary policies should fade out, inflation could ease, and interest rates could come down. This means that demand for construction would rebound and with it, construction activity.”

Dejan Krajinović, EECFA’s Serbian researcher (Beobuild) says that “Serbia’s overall construction output sank into a negative territory in 2025, primarily owing to the weaker performance in civil engineering. This year recorded growth in building construction, but the substantial consolidation in civil engineering dragged totals in red. The completion of major road, railway and energy projects contributed mostly, but delayed construction starts played a role as well. Residential construction is stable and is on historical levels, while non-residential construction is booming led by the hosting of the EXPO 2027 in Belgrade. Investments into commercial, hotel and office buildings are all spurred by the event, with the purposely built EXPO 2027 complex consisting of numerous venues being the single largest investment in non-residential. Improving financial conditions and sustained demand still support relatively high construction activity, but a lot of global political and economic uncertainties are dimming future prospects.”

Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia, says that Slovenia’s construction sector is holding steady at EUR 6bn, though growth has cooled. Residential buildings remain the anchor, with output expected to show only a slight dip in 2025, helped by strong employment, rising wages and cheaper mortgages. Property transactions rebounded in early 2025, reversing last year’s slump, while prices continue to climb amid land shortages and slow permitting. Public housing programmes are ambitious, but private developers are concentrating on Ljubljana and coastal towns. Non-residential construction is mixed: offices are recovering slowly, retail stays subdued, but industrial and warehousing thrive on export demand and automation while health and education remain at very high levels. Civil engineering and public works lean on EU-backed projects and are anticipated to reach historically high levels by 2026.

Eastern European construction markets

Andrey Vakulenko at Macon, EECFA’s Russian research institute notes that “the high key rate and the overall economic slowdown are constraining the Russian construction industry with negative trends expected for the current year and over the next two years. An easing of monetary policy, which has already begun, could help normalize the situation, but a positive effect is not expected until 2027. The main drag on construction output will likely be the residential subsector where high rates and revised government demand support principles are reducing activity among both buyers and developers. Negative trends will also likely persist in most non-residential segments due to declining growth rates of budget financing, a general decrease in business activity and a slowdown in consumption. The overall descending dynamics in the construction market may somewhat be mitigated by stable growth in civil engineering driven by export projects in energy and transport, but this growth is not predicted to be enough to keep the construction market in a positive zone”.

Prof. Ali Türel, EECFA’s Turkish researcher, reports that “the major effect of inflation-curb policies in Türkiye is the decline in disposable income and in the purchasing power of wage earners and pensioners. The moderate to lower-income population is unlikely to save enough equity for buying a home when rents have also become unaffordable for many. Ironically, housing sales have been increasing at a much higher rate than the growth of households. This can be attributed to the typical trend in Türkiye, where, during inflation, people expect a higher real return on their financial assets from real estate investments compared to alternative investment options. The reconstruction of earthquake-damaged buildings and infrastructure also contributed to the high rate of growth in building starts and completions from Q2 2025 onward, leading to the highest rates of change in the construction sector’s contribution to GDP compared to other sectors. Our latest forecast indicates that total construction output in Türkiye may reach 6.4 trillion TL in 2027 (EUR 180 billion), all at 2024 prices.”

According to Prof. Sergii Zapototskyi of Uvecon, EECFA Ukraine, despite the war and high risks, Ukraine’s construction industry remains one of the key drivers of economic recovery in 2025. The RDNA4 (the latest Rapid Damage and Needs Assessment Report) estimates Ukraine’s reconstruction needs for the next decade to be USD 486-524 billion, creating long-term demand for residential, non-residential and civil engineering construction works. Major challenges persist, including the uncertainty regarding the duration of the war, especially in frontline regions, labour shortages, bureaucratic barriers in the urban planning legislation, and logistical constraints due to the relocation of production facilities, and often, shortages in building materials. At the same time, the industry is demonstrating resilience: developers are diversifying supply chains, stabilizing procurement schedules, and increasing activity in the Central and Western regions. Demand for housing, intensive infrastructure restoration, and international investment from the EBRD, EIB, and other partners continue to support positive dynamics. The sector’s development prospects for 2026-2027 will largely depend on the security situation and the effectiveness of state recovery programs.