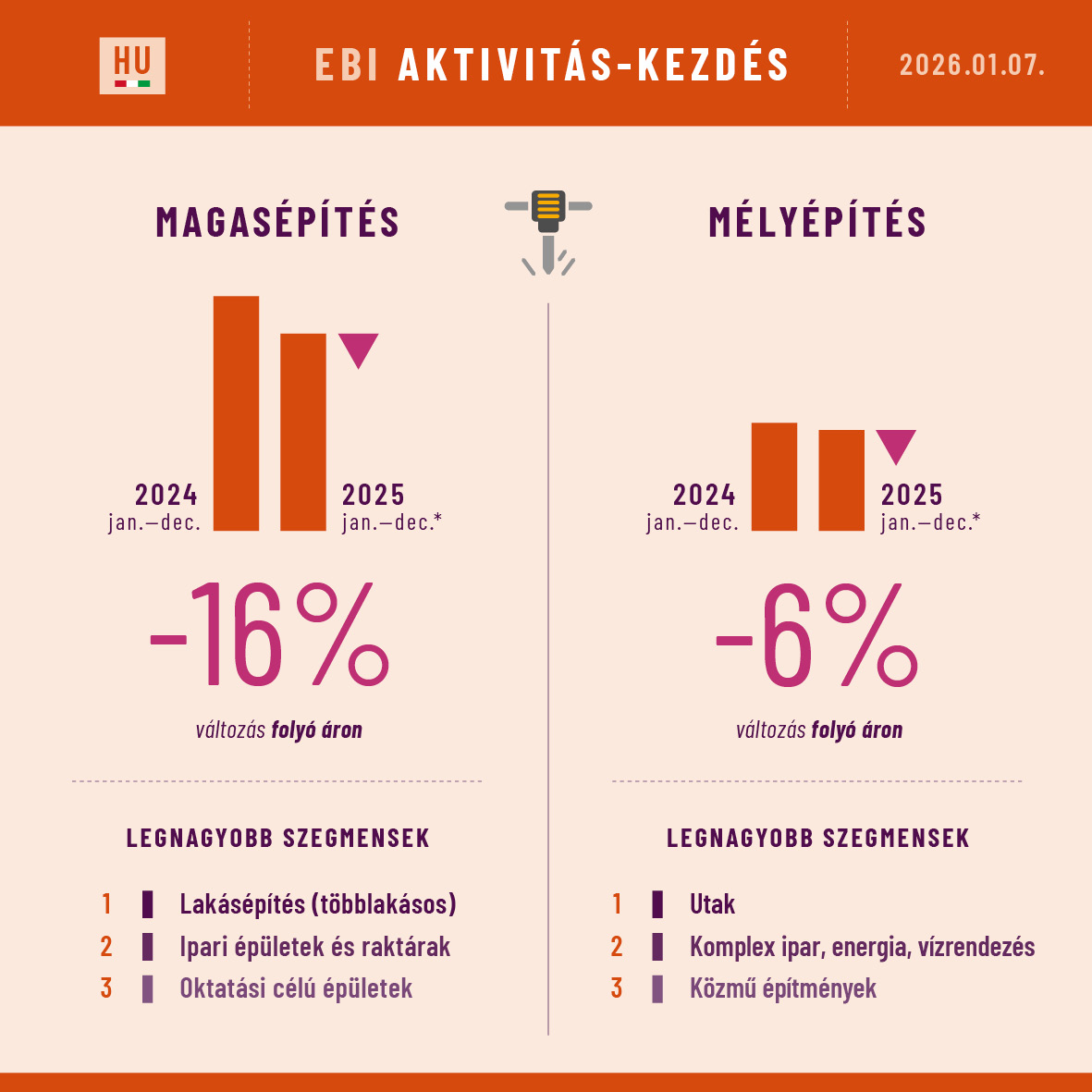

Az év vége nagyon gyenge lett a társasházi lakásépítés részpiacon, de 2025 egészében még így is megduplázódott az Aktivitás-Kezdés 2024-hez képest. Ezzel szemben a megkezdett nem-lakáscélú projektek értéke hatalmasat esett a tavalyi évben. Ezen a részpiacon nagyon tartós a visszaesés, három éve folyamatosan csökkenést mérünk. A mélyépítés 2025-ös Aktivitás-Kezdése lényegében megegyezik a tavaly előtti (és az előtti) év alacsony szintjével.

A poszter a két nagy építési részpiac Aktivitás-Kezdés indikátorának időszak/időszak változását mutatja, valamint a szegmenseket amelyekben a legnagyobb értékben indultak kivitelezések. Ezt a posztert minden hónapban kitesszük ide a blogunkra. A teljes építési piacot részletesen bemutató EBI Építésaktivitási Adatvizualizációt (összesen 18 szegmens adataival) is havonta frissítjük, és negyedévente az EBI Építésaktivitási Jelentésben is elmondjuk, hogy mit látunk a piacon. Ha érdeklik a részletek akkor a contact oldalon írjon nekünk.

The end of the year was very weak in the multi-unit residential submarket, but Activity Start in 2025 (as a whole) still doubled compared to 2024. In contrast, the value of started non-residential projects fell dramatically last year. The decline in this submarket is very persistent; it has been going on for three years. The Activity Start of civil engineering in 2025 stayed at the same low level as in the year before (and in the year before that).

The poster (above) shows the period/period changes of the Activity-Start indicator in the 2 main submarkets and the segments with the largest value of started works. This poster is published every month here in the blog. The EBI Construction Activity Data visualization with the details on the whole construction market (with altogether 18 segments) is also updated monthly and the EBI Construction Activity Report, summarizing what’s happening in the market, is published in each quarter. If your interest in construction markets is deeper, please contact us for the details.

EECFA released its 2025 Winter construction forecast on 12 December. Check out a sample report and place your order on eecfa.com. For discount, please contact us.

Southeast European construction markets

“Bulgaria’s total construction output is forecasted to increase by 3% on average for 2026-2027” – says Yasen Georgiev at Economic Policy Institute (EPI), EECFA’s Bulgarian research institute. He adds that this is to follow estimates for a similar performance of almost 3% in 2025. The sectoral background, however, shows, a nuanced picture – cooling of residential construction, positive news from non-residential and a robust performance of civil engineering. The latter will benefit from investments which will be backed by the absorption of EU funds through the Recovery and Resilience Plan (RRP) and classical operational programmes, both with implementation deadlines in 2026 and 2027. At the same time, Bulgaria’s economy is to expand by 2.4% on average in 2026-2027 – a period continuously shaped also by the Euro adoption on 1 January 2026.

Michael Glazer (SEE Regional Advisors) and Tatjana Halapija (Nada Projekt), EECFA’s Croatian members, think that declining dwelling sales in Croatia have, paradoxically, failed to stop the growth in the value of Croatian residential output, because increases in the price per square meter of those dwellings that do get sold have more than compensated for the lower number of square meters bought. “But how long this can continue is unclear” – they add. “The policies that the Croatian government is implementing in order to ease the country’s housing crisis are confusing the residential picture still more, since a number of those policies have contradictory effects on output. As to non-residential building construction, output growth during the period covered by the current forecast will depend greatly on the sector, with some likely to continue to benefit from catch-up growth and EU support for a bit longer and others moving toward a steady state or even a decline. In civil engineering, EU funds continue to play the dominant role in financing construction of all sorts. Sports facility construction is experiencing a boom, but given the speed with which such projects are completed, the effect on output will be relatively brief. Renewable energy construction should be growing rapidly, but regulators’ hostility toward the sector are holding it back.”

“Romania’s economy is entering a challenging period as the recently implemented measures to reduce the national account deficit begin to take effect” – reports Dr. Sebastian Sipos-Gug, EECFA’s Romanian researcher at Ebuild. “While most forecasters do not anticipate a recession, economic growth is expected to remain subdued over the next two years. Inflation is the highest in the EU, boosted in 2025 by increases in sales taxes. As a result, consumer prices are rising at a pace that is forecasted to outstrip wage growth, leading to a decline in real incomes in both 2025 and 2026. Government spending is also facing cuts, thus both private and public consumption are predicted to decline, with a chilling effect on most construction activity types. There is also the challenge of the massive level of public investment required by civil engineering projects that have started since 2023, which will be difficult to sustain under the austerity and the mounting pressure of losing even more EU funding. On the brighter side, both the economy at large and the labour market are expected to be quite resilient. By 2027, assuming the deficit reaches manageable levels, the effects of contractionary policies should fade out, inflation could ease, and interest rates could come down. This means that demand for construction would rebound and with it, construction activity.”

Dejan Krajinović, EECFA’s Serbian researcher (Beobuild) says that “Serbia’s overall construction output sank into a negative territory in 2025, primarily owing to the weaker performance in civil engineering. This year recorded growth in building construction, but the substantial consolidation in civil engineering dragged totals in red. The completion of major road, railway and energy projects contributed mostly, but delayed construction starts played a role as well. Residential construction is stable and is on historical levels, while non-residential construction is booming led by the hosting of the EXPO 2027 in Belgrade. Investments into commercial, hotel and office buildings are all spurred by the event, with the purposely built EXPO 2027 complex consisting of numerous venues being the single largest investment in non-residential. Improving financial conditions and sustained demand still support relatively high construction activity, but a lot of global political and economic uncertainties are dimming future prospects.”

Dr. Aleš Pustovrh at Bogatin, EECFA Slovenia, says that Slovenia’s construction sector is holding steady at EUR 6bn, though growth has cooled. Residential buildings remain the anchor, with output expected to show only a slight dip in 2025, helped by strong employment, rising wages and cheaper mortgages. Property transactions rebounded in early 2025, reversing last year’s slump, while prices continue to climb amid land shortages and slow permitting. Public housing programmes are ambitious, but private developers are concentrating on Ljubljana and coastal towns. Non-residential construction is mixed: offices are recovering slowly, retail stays subdued, but industrial and warehousing thrive on export demand and automation while health and education remain at very high levels. Civil engineering and public works lean on EU-backed projects and are anticipated to reach historically high levels by 2026.

Eastern European construction markets

Andrey Vakulenko at Macon, EECFA’s Russian research institute notes that “the high key rate and the overall economic slowdown are constraining the Russian construction industry with negative trends expected for the current year and over the next two years. An easing of monetary policy, which has already begun, could help normalize the situation, but a positive effect is not expected until 2027. The main drag on construction output will likely be the residential subsector where high rates and revised government demand support principles are reducing activity among both buyers and developers. Negative trends will also likely persist in most non-residential segments due to declining growth rates of budget financing, a general decrease in business activity and a slowdown in consumption. The overall descending dynamics in the construction market may somewhat be mitigated by stable growth in civil engineering driven by export projects in energy and transport, but this growth is not predicted to be enough to keep the construction market in a positive zone”.

Prof. Ali Türel, EECFA’s Turkish researcher, reports that “the major effect of inflation-curb policies in Türkiye is the decline in disposable income and in the purchasing power of wage earners and pensioners. The moderate to lower-income population is unlikely to save enough equity for buying a home when rents have also become unaffordable for many. Ironically, housing sales have been increasing at a much higher rate than the growth of households. This can be attributed to the typical trend in Türkiye, where, during inflation, people expect a higher real return on their financial assets from real estate investments compared to alternative investment options. The reconstruction of earthquake-damaged buildings and infrastructure also contributed to the high rate of growth in building starts and completions from Q2 2025 onward, leading to the highest rates of change in the construction sector’s contribution to GDP compared to other sectors. Our latest forecast indicates that total construction output in Türkiye may reach 6.4 trillion TL in 2027 (EUR 180 billion), all at 2024 prices.”

According to Prof. Sergii Zapototskyi of Uvecon, EECFA Ukraine, despite the war and high risks, Ukraine’s construction industry remains one of the key drivers of economic recovery in 2025. The RDNA4 (the latest Rapid Damage and Needs Assessment Report) estimates Ukraine’s reconstruction needs for the next decade to be USD 486-524 billion, creating long-term demand for residential, non-residential and civil engineering construction works. Major challenges persist, including the uncertainty regarding the duration of the war, especially in frontline regions, labour shortages, bureaucratic barriers in the urban planning legislation, and logistical constraints due to the relocation of production facilities, and often, shortages in building materials. At the same time, the industry is demonstrating resilience: developers are diversifying supply chains, stabilizing procurement schedules, and increasing activity in the Central and Western regions. Demand for housing, intensive infrastructure restoration, and international investment from the EBRD, EIB, and other partners continue to support positive dynamics. The sector’s development prospects for 2026-2027 will largely depend on the security situation and the effectiveness of state recovery programs.

There was no construction start indicator in Romania, so we have created an estimation for it.

This poster is a summary of our monthly findings. It shows how the total value of started construction works have changed over the same period last year. Besides, it presents which segments have the biggest start value in the current year. We call this indicator Activity-Start. And they are computed every month for 18 construction segments by aggregating data of construction projects. The projects are from the iBuild database and ELTINGA and Buildecon found the way of creating indicators out of them.

If you need short-term foresight, you will like it.

Brief comment from Janos Gaspar, head of Buildecon:

Activity-Start of building construction is still well below the peak year of 2024, but does not look as bad as before. This is mostly because works commenced on Rivius Mall, a grandiose retail and office complex in Cluj-Napoca. It is a very good sign, but it is too early to say whether the optimism returned to these segments. Activity-Start of civil engineering has been gradually coming down from the super high of 2023 but is still strong.

Every month this poster will be available here on our blog. If your interest is deeper, we have the EBI data visualization (with indicators for all the 18 segments of the construction market), updated monthly and we have the EBI Construction Activity Report Romania (with data and explanations), published quarterly in English and in Romanian. All these are packed into a yearly subscription. For the specifics, please contact us.

The latest EBI Construction Activity Report Hungary has found that it was mainly due to the ongoing M1 motorway expansion that the value of started construction projects rose significantly in the third quarter of this year. The value of projects entering construction in July-September 2025 exceeded HUF 1,000 billion at current price – the second highest level in the past ten years. Without this motorway expansion, accounting for around 60% of Activity-Start, the figures would have been much more modest, though.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database).

Building Construction Activity-Start

In Q3 2025 the value of started building construction projects was HUF 400 billion, around the same value as between April and June. Thanks to the outstanding figures between January and March, the value of building construction projects entering construction phase exceeded HUF 1,500 billion, only 4 points short of the same period in 2023 and 2024. At constant price, Activity-Start between January and September of this year was the lowest in the past 9 years.

Activity-Start of EBI Construction Activity Report in multi-unit housing construction, although greatly sank, stayed at a high level, with the total value of projects started in Q3 2025 exceeding HUF 170 billion. The situation was the opposite in non-residential construction. The segment recovered somewhat between July and September from the previous quarter’s low point, but projects still entered construction at a low value: Activity-Start was around HUF 230 billion. Since 2017 non-residential construction projects haven’t started at a lower value than in the first 9 months of this year.

The largest non-residential projects entering construction in Q3 2025 included MCC’s talent centre in Miskolc, BYD’s electric bus assembly plant in Komárom, Panattoni Logistics Park Building A in Mosonmagyaróvár, IGPark automotive parts manufacturing hall in Nyíregyháza, Phase 2 of Weerts Ebes logistics centre, and MVM Neuron headquarters office building in the 3rd district of Budapest.

Civil engineering Activity-Start

Civil Engineering Activity-Start of EBI Construction Activity Report registered a surge in Q3 2025 due to M1 motorway expansion (M0-Concó rest area). Outside road construction, the value of construction projects started in other civil engineering segments was moderate. While total Civil Engineering Activity-Start exceeded HUF 760 billion, the value of non-road and railway projects started was only around HUF 50 billion in Q3. In addition to the two phases of M1 motorway expansion, only Phase 7 of the closure of the Gyöngyösoroszi ore mine could make it to the list of the biggest started civil engineering projects.

Budapest on top among regions

In the past four quarters, the highest value of construction projects in Hungary started in Budapest and its share in total Activity-Start was 28%. Central Transdanubia also had a large share of 23%. 39% of projects started in Western Hungary, 38% in Central Hungary, while Eastern Hungary’s share was 23%.

Still high multi-unit housing Activity-Start

Although Q3 2025 was the second consecutive year to see a significant drop in the value of started multi-unit housing construction works, Activity-Start stayed high, far exceeding the average of recent years. At current price, multi-unit housing construction works started at an over HUF 170 billion, the fourth highest value after the first two quarters of 2025 and the last quarter of 2024. Overall, the successful first 9 months of this year brought a huge jump in multi-unit housing Activity-Start at current price, but it was also outstanding at constant price, only surpassed by the same period in 2017 in the last 10 years.

Multi-unit housing construction is likely to remain strong. There was a high number of building permits issued in the first three quarters of this year, meaning plenty of projects to get started. In Q3 2025 permitting was boosted by the preferential loan program dubbed Otthon Start available since September which could continue to have a positive impact on the number of homes under construction.

In Q3 this year, multi-unit homes worth around HUF 80 billion were completed at current price, while in the first 9 months, multi-unit housing Activity-Completion was well over HUF 200 billion, only slightly lower than in the same period in 2023-2024.

Looking at the past 4 quarters, Budapest continued to have a major share in multi-unit constructions entering construction (73%). Central Hungary had a 76%, while Western Hungary and Eastern Hungary had a share of 12% each.

Still weak Activity-Start in industrial buildings and warehouses

Industrial buildings and warehouses thrived between 2022 and 2024 when construction works worth between HUF 700 billion and 1,000 billion started annually. For example, construction started on several BMW plants around Debrecen, on Mercedes-Benz projects in Kecskemét, and on several battery factories. This year has seen a decline so far and the value of projects started during three months in Q2-Q3 2025 has been the lowest since 2021. Overall, in the first 9 months of 2025, Activity-Start in industrial buildings and warehouses was around HUF 400 billion, 37% lower than in the same period of 2024, and 29%-39% lower than the 2022-2023 values. Trends are similar at constant price: the period of 2021-2023 was exceptionally good for industrial buildings and warehouses, while there was a strong decline in 2025. In the last 10 years, Activity-Start at constant price in the first 9 months has not been so low as now.

The biggest projects started between January and September 2025 were CTP’s logistics halls in Biatorbágy and Vecsés, HelloParks’ logistics hall in Fót and BYD’s projects in Szeged and Komárom. Construction of Phase 1 of Halms automotive parts manufacturing plant in Miskolc and Panattoni Logistics Park Building A in Mosonmagyaróvár also started.

Activity-Completion was relatively high in all three quarters of 2025 as several projects that started in 2022-2024 reached completion. The value of projects completed since the beginning of 2025 neared HUF 700 billion. For example, this year saw the completion of CATL warehouse and metalworking plant in Debrecen and its surroundings, two BMW factories, and the hangar complex of the Helicopter Base in Szolnok. And Activity-Completion may also remain high in the last quarter of this year.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)

The viz was updated on 29 November 2025 and it is great to see the recoveries here and there. The text will be updated as soon as we have all the permit data (Ukraine Q3 is missing now).

When it comes to permits, Croatia and Serbia are still very stable. Both countries experienced massive expansion between 2014 and 2022 and they have remained close to their peak every since. Croatia has had around 4 million, while Serbia has had above 7 million permitted m2 for three years. Q2 in Slovenia was not soo good, so it remained well below the peak reached in 2022. Bulgaria is also below its latest peak, but permit data of the latest 3 quarters depict a growing optimism. In Romania the mild recovery is ongoing, led by the residential submarket. Hungary also turned upward, also because of the residential permits. The non-residential submarket looks very bad. Permits have fallen back to the level experienced in 2015.

You may use the dropdown in the viz for selecting either the residential or the non-residential submarket, or both.

In the full visualization, not only permit but completion data can be followed (where available).Just click on the Country-by-country sheet.

Led by the residential submarket, Türkiye bounced back and up. And due to changing accounting method, all permit time series from 2010 have been revised. From Q2 2025 on, permits issued by authorities other than the municipalities are also reported by TUIK. So the scope is bigger, the results show the full picture. Click through the below viz for understanding the size and the impact of this revision. Mild optimism prevails in Ukraine, the permitted floor area keeps expanding. Since the beginning of this year the residential submarket drives this growth. Russia is stable when it comes to completion of buildings. Non-residential has been edging up, residential has been edging down lately.

Written by Sergii Zapototskyi – UVECON, EECFA Ukraine

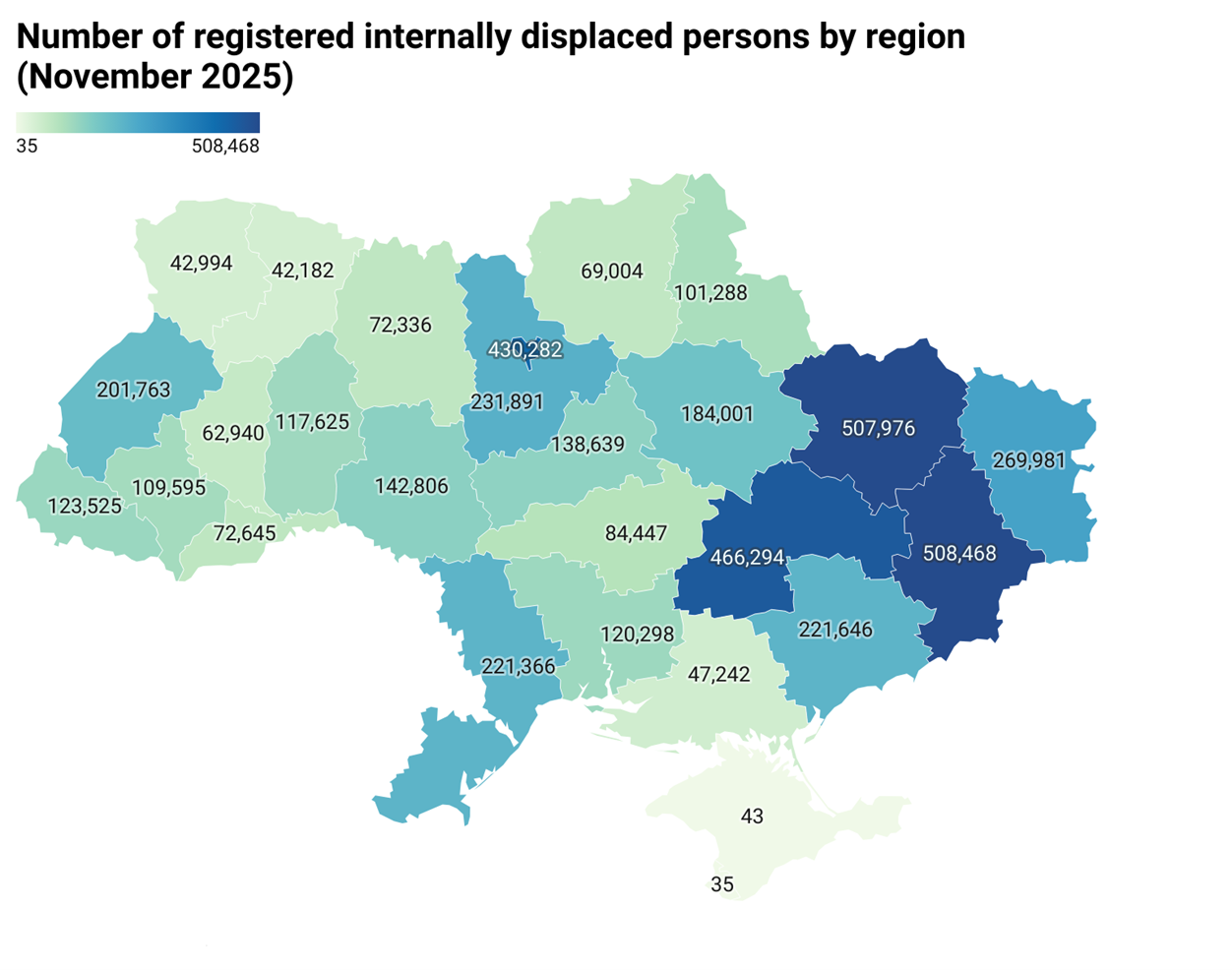

The full-scale invasion of Russia caused a deep humanitarian crisis and exacerbated socio-economic disparities in Ukraine. One of the key challenges is to provide homes for internally displaced persons (IDPs). The mass movement of the population created a shortage of affordable and temporary housing as the infrastructure was not ready for such a load. The government is already working on a new housing policy, which might also help resolve the issue of housing for IDPs.

As of 1 November, this year, 4,588,045 internally displaced persons were officially registered in Ukraine, including 838,436 children under the age of 18 [1]. Most IDPS are in Kharkiv region (508 thousand or 11%), followed by Dnipropetrovsk region (467 thousand or 10%), the city of Kyiv (430 thousand or 9.4%) and Kyiv region (232 thousand or 5%). [3]. IDPs in these regions total about 1.6 million people [1]. As per the result of the 16th round of the survey conducted by The International Organization for Migration (IOM, UN Migration), as of April 2024, about 2.7 million internally displaced people were from frontline areas.

Housing damages, needs and solutions

In total, more than 1.3 million Ukrainian households lost their homes because of the war, including not only IDPs, but also residents of settlements that suffered extensive destruction. The World Bank estimates total housing needs in Ukraine between 2025 and 2035 to be USD 86 billion, mostly to finance repair and reconstruction works of the housing stock (estimated at USD 75.5 billion including the cost of clearing rubble at USD 5.7 billion). USD 404.6 million should go to acute housing needs and funding has also been identified for organizational measures (USD 37.5 million) and regulatory and technical processes, including the development of strategies (USD 12.5 million) to coordinate and implement reconstruction programs [4].

Citizens have already submitted over 850,000 reports of housing damage through the Diia app (the national public-services portal) totalling over 60 million sqm of losses. For comparison, in the pre-war period, an average of 9-10 million sqm of homes were completed in Ukraine each year, demonstrating the scale of challenge and need for multi-level solutions in housing policy. Preferential lending programs are unable to solve this situation and cover the housing needs. The ‘jeOselia’ program provided loans worth over UAH 28 billion, but 52% of this went to military personnel, while IDPs received only 566 pieces of loans. In 2024, within the framework of this 3% mortgage program, only 500 families were provided with housing. The situation is even more critical in the rental market as the state program for subsidizing rental housing has shown low efficiency. The majority of IDPs (90-95%) rent homes unofficially, making them vulnerable to unreliable living conditions and unjustified rental charge increases or evictions.

Modular settlements are a key temporary housing for IDPs, although living conditions here cannot be considered fully comfortable. Initially, they were meant to be short-term but gradually became long-term housing for many families due to their limited finances. Today, besides the psychological difficulties and discomfort of residents, operating such facilities is also a major challenge. The maintenance of modular settlements, including payment for utilities, repairs and security, falls entirely on local budgets, an additional financial burden for communities which often do not have enough resources to sustainably finance these.

As the problem of providing housing for IDPs is systemic in nature and cannot be solved solely through financial instruments, a comprehensive review of state housing policy has become necessary, particularly the development of an affordable rental housing segment, social programs, and long-term support mechanisms for both IDPs and vulnerable categories of the population in general.

The Ukrainian Parliament is already working on several key legislative initiatives. The central one is draft law No. 12377 ‘On the Basic Principles of Housing Policy’ to replace the current Housing Code from 1983 which does not contain basic concepts for modern housing policy such as social rental housing or housing stock of communal ownership. Draft law No. 4080 is also important on the inventory of the housing stock. In parallel with drafting these laws, necessary by-laws are being prepared to regulate the practical mechanisms for implementing housing policy (creation and maintenance of housing queues, criteria for selecting recipients of state support, and the procedure of providing various forms of housing assistance). In addition, the government’s plans until 2027 include allocating EUR 650 million to the eRecovery Program, EUR 450 million to support IDPs, military personnel and the families of the deceased, creating a social housing fund and introducing a unified state online system for the long-term strategy of social integration and support for vulnerable categories of the population. All this might help resolve housing for IDPs.

Sources:

Internally Displaced Persons. State Enterprise “Information and Computing Center of the Ministry of Social Policy, Family and Unity of Ukraine”: https://www.ioc.gov.ua/analytics/dashboard-vpo

More on the Ukrainian housing market and forecast for the segment, as well as the rest of the construction market will be in our Winter Forecast Report Ukraine to be out on 12 December, along with our other 7 country reports. To obtain it and check a sample report: https://eecfa.com/

Russia’s resort real estate market has seen a dynamic growth in recent years, partly due to the emergence of aparthotels – a format attractive to both developers and hotel operators. The coming years are also expected to see a sharp increase in aparthotel construction, supporting the non-residential construction market – according to Andrey Vakulenko, EECFA’s Russian analyst.

Thriving aparthotel segment

Resort real estate has been one of the fastest-growing segments of the Russian construction market in recent years. Aparthotels – apartment complexes with minimal infrastructure and services, and with the mandatory availability of a trust management – have particularly seen a rapid growth, though they are relatively new to the Russian market. The core of the supply is (and will be) resort projects, i.e. aparthotels in locations with developed recreational and tourist infrastructure for seasonal vacations. Urban aparthotels – primarily in metropolitan areas with minimal infrastructure – are rather aimed at business travelers and to a lesser extent at traditional tourism and long-term rentals.

As of Q3 2025, the aparthotel market size stood at 25,200 units with a total area of 612,500 sqm and by the end of this year, roughly 143,000 sqm of new aparthotels, or 4,300 new units are expected to open. Based on the announced plans, the next three to four years will register a sharp rise, and by the end of 2029 aparthotels may amount to around 109,800 units with over 3.6 million sqm, almost six times higher than the current level.

Behind the growth

One of the main reasons for the anticipated expansion of the aparthotel format is that domestic tourism gained popularity after 2022 due to the reduced accessibility of many international resorts (because of the suspension of air travel, the weak ruble, visa issues, and other internal or external restrictions). Rise in domestic tourism created stable high demand for accommodation in virtually all key resorts in Russia.

Another reason is that developers specialized in multi-unit residential construction began to start many projects in aparthotel and resort real estate construction amid the decline in the residential real estate market following the cancellation of the mass preferential mortgage program.

Also, there are significant incentives and state support for developing tourism infrastructure and the domestic tourism industry, including the construction of hotel complexes and aparthotels.

Furthermore, in 2024 the status of aparthotels was legalized; they were included in the official hotel classification system, creating uniform standards for the segment and transparent conditions for market participants.

Besides, the departure of many large foreign hotel operators from the market in 2022 led to the expansion of Russian hotel chains (Azimut Hotels, Cosmos Hotel Group, Alean Collection, ZONT Hotel Group, VALO Hotel Services, Mantera Group, among others), which began collaborating with aparthotels, increasing the latter’s attractiveness and guaranteeing a high level of service and trust management services.

Moreover, many investors appeared in the market who found the trust management model used in aparthotels and the opportunity of generating passive income attractive. The operating return on investments in aparthotels in developed resorts managed by well-known hotel brands can reach 7%-10% and higher. And given the rise in the market value of apartments, long-term returns can reach 13%-17% per annum, exceeding the return on long-term bank deposits (currently 8%-10% per year for a three-year deposit).

All this suggests that aparthotels will be a major segment of non-residential construction in the coming years.

Coastal regions: top locations for aparthotels

The aparthotel format is developing most actively on the Black Sea coast, currently accounting for over half of the total supply in this segment. Urban aparthotels are primarily in Moscow and St. Petersburg with just over one-fifth of the total supply.

In the coming years, it is also the Black Sea coast that will likely register the biggest expansion in supply, but new aparthotels are also set to be actively emerging on the Caspian Sea coast, in Dagestan.

In coastal regions (Krasnodar Krai, Crimea, Dagestan), aparthotels under construction already amount to more than a quarter of all multi-unit residential real estate under construction and this figure is expected to grow further.

There is also an increase in the construction of similar projects in other resorts across the country, for example, on the Baltic coast or at mountain and spa resorts in the North Caucasus, the Altai Mountains and the Urals, among others.

With the latest governmental decision, the number of projects in designated rust belt action areas reached 68 in Hungary. Estimated 40 thousand dwellings1 are being built or will be built on these sites. The sole purpose of this post is to follow these projects and to see how they will or will not help the recovery of the new residential construction sub-market in Hungary.

Status on 1 October 2025. The upswing has continued, but less intensively. — Completed: 3 102 dwellings Under construction: 9 770 dwellings Before construction: 19 490 dwellings

Brief background

Rust belt action areas (let me shorten them to rusty) are practically brownfield areas with special benefits. The owner of the site or the developer should initiate the process (with specific development plans) and there is a Committee to examine if the proposed site is entitled for the rusty status. Based on the opinion of the Committee, the final decision is made by the government. The decisions (about the exact sites) are announced in a decree and the special benefits coming with it are:

priority investment status, meaning e.g. faster permitting procedures2,

newly built homes can be sold at 5% VAT without limitation in time3,

By the current regulations, it means a min. 5% and a max. 27% price advantage over competitors developing on non-rusty area until 2030 (depending on when the permit was obtained) and a 27% price advantage from 2031 on.

Our focus

What we do is to turn the mentioned decree into information we need for forecasting. With the help of Eltinga Building Permit Monitor database and the iBuild project information database, actual projects are identified from the lot numbers specified in the decree. Among all the general project specifics, the number of dwellings (where it is known), are attached to these projects.

The map shows the stages of the housing projects that were given rusty status. Bluish dots are those before construction, neon yellow dots are those under construction and the dot disappears once the project is completed.

OK, it is very convenient to see projects on a map, but our focus is more on the chart under the map where the yellow is the number of homes under construction.

What we are curious about is if and when the right end of the yellow curve shows a strong upturn.

In other words, we are curious whether the regulation ignites a recovery or not. As of now, it is more common that the yellow line has increased because projects having started in the past were given the rusty status. (So they were just re-qualified, it did not mean new project starts.) In parallel, it is less common that projects start after they were given the status. Just two extreme examples for these: Unipark Buda has been under construction since 2019 and it got the rusty status at the end of 2023, while Láng quarter was given the rusty status in 2021 and it is still before construction.

The charts will be updated quarterly, so check back if you are also curious.

Another way we like to look at it is a list. Here we do not separate the projects to phases (like on the map) and it gives a quick understanding on how each rusty project moves ahead from 1 February 2024 on.

Data sources

The data mostly come from Eltinga Building Permit Monitor (in Hungarian: Építési Engedély Figyelő). This is a very detailed database on before construction multi-unit housing projects in Budapest. It is aiming primarily at developers who would like to understand the competition. For further information on this, please turn to Mr Zoltán Sápi, Eltinga, sapiz@eltinga.hu. Besides, we used the iBuild project information database.

This is an estimation based on the median size of those rusty projects where the number of homes were announced ↩︎

Written by Dejan Krajinović, Beobuild Core d.o.o., EECFA Serbia

Overall construction output in Serbia is expected to decline this year, primarily due to the slowdown in civil engineering as several major road and railway projects were completed last year. By contrast, non-residential construction has entered a new growth cycle driven by investments connected to the hosting of EXPO 2027 in Belgrade. The event will be held in a purpose-built exhibition complex in the outskirts of the city, covering around 80 hectares. Alongside the construction of this complex, numerous public and private investments are indirectly tied to the event, including new hotels, accommodation, leisure, and commercial projects, as well as the reconstruction of museums, cultural heritage sites, and public spaces.

Aerial photo of the construction site of the EXPO 2027 complex – Photo: beobuild.rs

The EXPO 2027 complex itself is a vast construction site, comprising approximately 230,000 sqm of exhibition pavilions, multifunctional venues, congress and conference halls, as well as office and retail space. In addition, a residential complex with around 1,500 units is being built to house participating delegations. The exhibition will run for 93 days, from 15 May to 15 August 2027, featuring around 130 countries and hundreds of events spanning sports, science, culture, and innovation. Total investment could exceed EUR 2.5 billion, with EUR 1.5 billion allocated for the EXPO complex and a further EUR 1 billion for accompanying facilities and infrastructure. This project has been the key driver of growth in non-residential construction and is expected to sustain activity in the sector in the coming years.

The broader development zone around the EXPO 2027 complex extends far beyond the exhibition center itself. While the core site covers 80 hectares, total development area exceeds 200 hectares. It will include the new National Stadium complex, a center for aquatic sports, a theme park, recreation facilities, and hotels. The National Stadium alone is a EUR 600 million project, designed with 52,000 permanent seats and the capacity to expand by an additional 8,000. Construction began in early 2024 and, despite delays, it is expected to be completed in time for 2027. Other sporting and leisure facilities are also planned for delivery ahead of the event, though it remains uncertain whether all projects will meet the deadline.

Several other public and private developments across Belgrade are linked to the exhibition, including the reconstruction and expansion of museum facilities: a new Natural History Museum building, the relocation of the Nikola Tesla Museum, the renovation of the Aeronautical Museum, and the modernization of the City of Belgrade Museum, among others. The private sector is likewise preparing for the anticipated rise in visitors, with investments in accommodation accelerating. Notable projects under construction include new hotels under the Intercontinental and Ritz-Carlton brands, alongside numerous smaller ventures.

However, the high level of spending on the EXPO 2027 has placed considerable strain on the state budget. To maintain fiscal deficits at around 3% of GDP, funds have been reallocated from other public projects. This has been most evident in infrastructure development and civil engineering, where shifting priorities have led to significant delays on major planned projects. As a result, civil engineering output is contracting faster than expected in 2025, with negative implications for growth in 2026 as well. On the other hand, long-term economic benefits of hosting EXPO 2027 remain uncertain.

After the event concludes, the EXPO 2027 complex will be repurposed as the new Belgrade Fair Complex. The current fairgrounds in central Belgrade, built in the 1950s, are planned for redevelopment once operations move to the new site. This ensures that the EXPO facilities will continue to be used in the years ahead, supporting the economic rationale for the project. Moreover, new transport infrastructure, including a railway link to the city center, river dock facilities, and expanded commercial developments, should further enhance the attractiveness of the location for private investment.

Forecast up to 2027 for the Serbian non-residential market and for the rest of construction subsegments is available in the 2025 Summer EECFA Forecast Report Serbia. To order it or to request a sample report, please contact us.

On a quarterly level, the value of started construction projects in the second quarter of this year has been the second lowest since 2020 and the Activity-Start of EBI Construction Activity Report Hungary at current price did not reach HUF 470 billion. In the first half of the year, projects entering construction phase were worth around HUF 1,200 billion, far below the previous years and close to H1 2020 when the pandemic hit.

EBI Construction Activity Report Hungary analyses the construction industry on a quarterly basis, including the volume of newly started construction works and the value of projects completed in each quarter in aggregate and by segment as well. It is prepared by Eltinga, Buildecon (creation of indicators and development of algorithms for aggregation) and iBuild (project research and project database). Inquiry and price offer for the report.

Building construction performed poorly in Q2 2025

In Q2 2025 the value of building construction starts fell below HUF 400 billion, barely reaching half of the Activity-Start of Q1. After 2020 it was only in Q3 2024 when the value of construction starts was at a similarly low level. The decline in building construction was even more pronounced at constant price: Activity-Start of EBI Construction Activity Report at constant price was last lower in Q1 2015 than in Q2 this year.

Such a poor performance in building construction occurred despite the extremely successful quarter in multi-unit housing construction. The Activity-Start for non-residential construction fell to a critically low level not seen since Q1 2015, below HUF 120 billion. At constant price, the decline is even more drastic, the value in Q2 2025 was less than half of the previous negative record.

The largest building construction projects during Q2 2025 were mostly multi-unit housing ones. Only one non-residential project made it to the list of the biggest projects, Phase 1 of Halms automotive parts manufacturing plant in Miskolc.

Better Civil Engineering Activity-Start, but still at a low level

Q2 2025 saw an improvement over Q1 in Civil Engineering Activity-Start of EBI Construction Activity Report, but projects started only at a value of around HUF 100 billion. In the road and railway construction segment, there was an increase in Q2 2025 against Q1 with projects entering construction phase on HUF 50 billion, a level not considered high.

The biggest civil engineering projects launched in Q2 2025 include the railway infrastructure of the Ivancsa industrial-innovation development area, the XIV/A water shaft in Tatabánya, and the development of the drinking water networks in Ács, Bábolna and Koppánymonostor.

The capital city has the highest share in total Activity-Start

Looking at construction projects launched in the past four quarters, Budapest had the highest value with a share of 34% in total Activity-Start. It still exceeds the 20%-30% typical of the period between 2021 and 2023.

In the previously leading Northern Great Plain, 16% of projects started. The share of Southern Transdanubia was 15%, and that of the Southern Great Plain was 11%. The lowest values were registered in Northern Hungary and Western Transdanubia during the period, with a share of 4% each. In Central Transdanubia and the Pest region, a respective 8% of projects were launched.

Favourable trend continuing in multi-unit housing construction

Q2 2025 far exceeded the average of recent years in terms of the value of construction starts: multi-unit housing constructions started at HUF 250 billion at current price. This is an absolute record, the second highest value after Q1 2025 registered since 2014. Activity-Start of EBI Construction Activity Report in the segment exceeded HUF 200 billion for the third consecutive quarter, way more than the previous highest HUF 144 billion until H1 2024. The expansion was also significant compared to previous years, even when calculated at constant price.

The momentum fuelled so far by maturing government bonds and interest payments may continue this autumn with the launch of the Home Start Program (providing first-time home buyers with a fixed-rate loan of up to HUF 50 million at a 3% interest rate). Also, this autumn, projects financed by the Housing Capital Program this year (a government initiative to help the supply side) may also appear among sold homes. As a result of these, a pick-up in both demand and supply is expected for the rest of the year. In Budapest, the projects of the Housing Capital Program may be the source of a further high level of Activity-Start. In the countryside, more multi-unit housing projects may start due to the livelier demand thanks to the launch of the Home Start Program. In the capital city, the number of available new homes is already at one of the highest levels in recent years because of the previous significant construction starts. This, in addition to the new supply, may make developers more cautious with project launches as the end of the year approaches.

The value of completed multi-unit homes in Q2 2025 was around HUF 90 billion, a slight increase compared to Q1. Overall, Activity-Completion of multi-unit housing constructions slightly dropped in the first half of the year compared to the previous year, remaining roughly at the 2023 level.

Looking at the past four quarters, Budapest has had a massive share in multi-unit housing constructions entering construction phase (75%), while none of the other regions reached 10%. In Central Hungary 77% of such projects started and in Western Hungary 14%, while only 9% of the Activity-Start was registered in Eastern Hungary.

Hotels in focus: the year started off sluggishly for projects, but growth is visible

Hotel construction works boomed in 2019-2020 most, but projects also commenced in 2021 and 2023 at relatively high values. 2024 saw a slight decline, and this year also started rather sluggishly. The second quarter brought some expansion, though; between April and June 2025, the total value of construction starts in the segment was over HUF 20 billion, a major improvement compared to the previous, very weak quarter, and roughly the same as the median for the period between 2023 and 2025. At constant price, we also see that Activity-Start of EBI Construction Activity Report in Q2 2025 does not differ much from previous quarters but is far behind the high values between the end of 2019 and the beginning of 2021. The largest started hotel projects in H1 2025 included Phase 1 of Staybridge Suites Hotel in Budapest and the MCC Talent Development Center project in Miskolc.

Several hotel projects that were launched in previous years have now reached completion. In Q2 2025, Activity-Completion in the segment set a record, approaching HUF 90 billion at current price and exceeding HUF 160 billion at constant price. For example, the 4-star hotel next to the Balaton Park Circuit racetrack and Le Primore Hotel in Hévíz have been completed.

Also, many hotel projects are currently underway which are due for delivery next year, such as the renovation of the Grandhotel Galya in the countryside, and a number of hotels under construction or under renovation in Budapest: Sofitel Budapest Chain Bridge, hotel in Kígyó street, VP36 Boutique Hotel, Paulay Opera Hotel, Hotel Paulay (Puro), Moxy Budapest Downtown by Marriott, and Hilton Garden Inn. Hotel Gellért in the capital city is also undergoing renovation and may be completed in 2027. Klotild Palace St. Regis Hotel and K36 Hotel and Student Hostel are also nearing completion and could open this year.

Original article: Tünde Tancsics (ELTINGA); English version: Eszter Falucskai (Buildecon)